Markets bounce back after initial Brexit turmoil, but long-term uncertainty remains

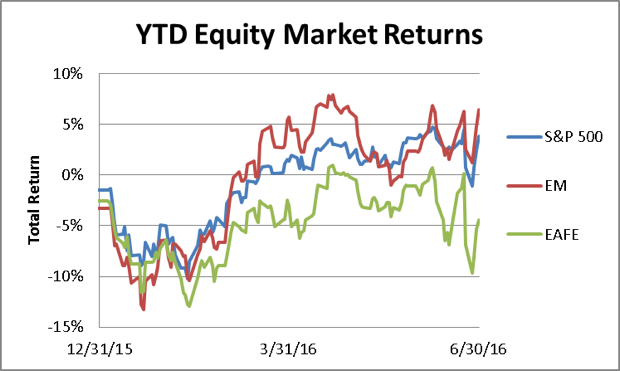

Global equities faced a fickle market backdrop during the second quarter. While improving economic fundamentals strengthened market sentiment through most of the quarter, investor anxiety re-emerged following Britain’s June 23rd decision to exit the European Union (EU). A sharp two-day selloff in global equities followed the “Brexit” referendum, but risk assets rallied during the final three days of the quarter and largely offset those losses. As a result, the S&P 500 Index still managed to return 2.5% in the quarter (3.8% YTD), and the emerging market index (MSCI EM) posted a positive quarterly return of 0.7% (6.4% YTD). The international developed market index (MSCI EAFE), on the other hand, declined 1.5% during the quarter and extended its year-to-date loss to 4.4%.

Source: Bloomberg

Although the markets largely recouped the Brexit’s immediate negative effects by quarter-end, it has injected new political and economic uncertainties into the financial markets that could take some time to digest fully. The direct impact of Brexit looks to be rather limited over the near term, since negotiations over the U.K.’s exit from the EU are poised to take place over two years. That said, concerns surrounding the ultimate impact of Britain’s departure could stifle business investment and economic activity in the region during the interim—significantly elevating the potential for a recession in the U.K. (and possibly other parts of the EU).

In the U.S., the risk of recession over the next 12 months is slightly higher than it was before the Brexit vote. The U.S. economy is primarily driven by domestic consumption and investment, however, which should insulate it from the worst of the Brexit fallout. While deteriorating economic growth overseas and a strengthening dollar could negatively impact international demand for U.S. goods, exports account for less than 15% of U.S. gross domestic product (GDP)—and the U.K. comprises just a small fraction of that. Even the much larger EU, which is likely to experience some economic weakness following a divorce from the U.K., comprises just 17% of U.S. exports.

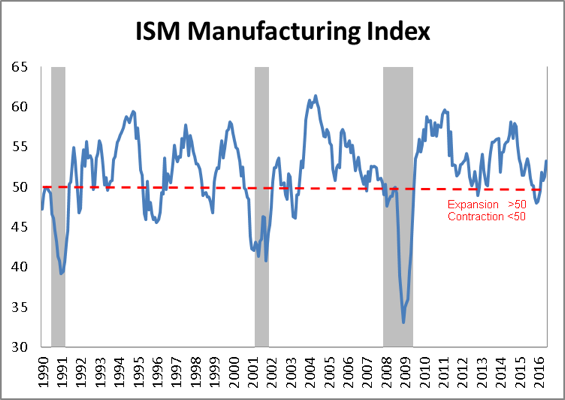

On a standalone basis, the U.S. economy appears to have rather stable footing. Even the long-suffering U.S. manufacturing sector is showing signs of recovery. The ISM Manufacturing Index expanded for the fourth consecutive month in June, climbing to its highest level in 16 months. In addition, the threat of a U.S. Federal Reserve-induced recession from potentially ill-timed interest rate hikes now appears much more remote than it did earlier this year. The global economic uncertainty created by Brexit will force the Fed to take a slower approach to policy normalization than it had previously anticipated. Against this accommodative monetary backdrop, we believe domestic GDP will continue to expand at a consistent (albeit tepid) 2% rate of annualized growth over the coming quarters.

Source: Bloomberg

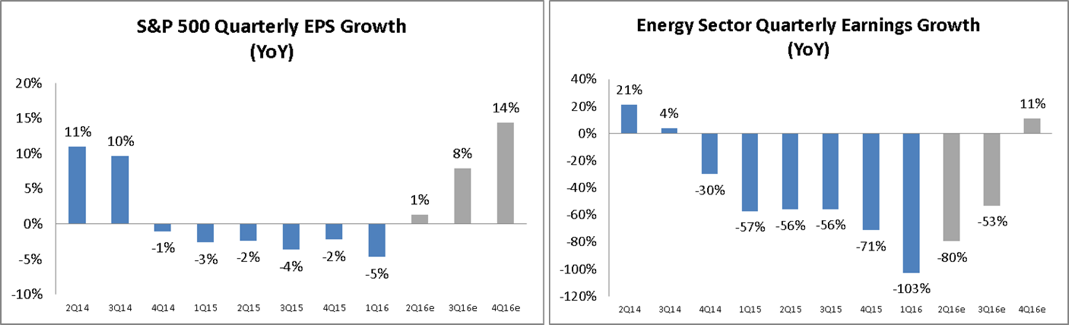

While the domestic economic growth outlook is far from robust, U.S. equities could continue to move modestly higher in this low-growth environment. Earnings have been the biggest driver of the stock market’s recovery over the last seven years and will continue to determine the trajectory of equity returns, since price-to-earnings multiple expansion from current levels is unlikely. While substantial declines in energy sector earnings have dampened corporate profit growth over the last 18 months, we expect that headwind to reverse. With oil prices back up near $50 per barrel, year-over-year corporate earnings growth should reaccelerate during the third quarter of 2016 for the first time since oil prices started to collapse in mid-2014. This rebound in earnings growth should extend into 2017, potentially driving sustained advances in domestic equity prices over the coming quarters.

Source: Bloomberg Source: Bloomberg

Nonetheless, investors should anticipate more measured equity returns over the next several years. Furthermore, with Brexit concerns now adding to the laundry list of risks threatening to derail this protracted bull market run, we expect increased market volatility for the foreseeable future. Consequently, we plan to maintain our slightly more conservative stance in the near term until we have more clarity on the Brexit’s geopolitical and economic implications. We believe stocks will continue to offer better risk-adjusted returns to investors over the longer term against bonds, gold, cash and other competing asset classes, however. Accordingly, we are not making material changes to our long-term strategic equity allocations and will capitalize on periods of elevated volatility to rebalance tactically around that norm.

Core Portfolio

During the quarter, we initiated positions in Bunge, Allergan, the S&P Oil & Gas Exploration & Production ETF and the ProShares Short S&P 500 ETF.

Bunge is an agribusiness company involved in various phases of the food production value chain. The company purchases, transports, and distributes grains and oilseeds; crushes oilseeds to make meal and oil for the livestock and food processing industries; and produces edible oils and related products for food service customers and consumers. We view Bunge’s global asset base as an effective means to capitalize on secular growth trends in agriculture, which are being driven by global population growth and the escalating shift toward protein-rich diets in developing countries.

Allergan is one of the world’s largest specialty pharmaceutical manufacturers. Its key products include Botox, which is approved for cosmetic and therapeutic indications; Restasis, a treatment for chronic dry eye; and Namenda, an Alzheimer's disease treatment. Shares of Allergan came under significant pressure early in the quarter because of Pfizer’s failed takeover bid of the company. The shares were pressured further by unwarranted concerns associated with Allergan’s business model following the widely publicized troubles of industry peer Valeant Pharmaceuticals. Given Allergan’s solid product portfolio and its ability to delever its balance sheet significantly with its pending generics business sale, we viewed the steep selloff of the shares as an opportune time to build a position in the company.

The S&P Oil & Gas Exploration & Production ETF is composed of about 50 U.S.-based energy producers. We used this investment vehicle to add diversified exposure to the E&P sector, as shares of these companies remain dramatically undervalued. If oil prices recover to a more normalized level of $60 per barrel over the next two years (as we expect), energy-related names should offer significant upside from today’s depressed levels.

The ProShares Short S&P 500 ETF provides inverse (opposite) exposure to the S&P 500 Index. As such, if market conditions deteriorate and the S&P 500 declines, this investment will gain value. While we remain constructive about the outlook for domestic equity prices over the long term, this investment gives us the ability to reduce our downside exposure during potential bouts of volatility as the market confronts a number of unusual political and economic challenges over the next six months.

We sold our positions in BlackRock and the Consumer Staples Sector ETF, as both securities reached our risk-adjusted price targets.

BlackRock is the largest asset manager in the world, with more than $3.6 trillion under management. Although we continue to like the firm’s assets and scale advantages, the current environment of elevated volatility and low interest rates presents challenges for future earnings growth. As for the Consumer Staples Sector ETF, while we like the defensive properties consumer staple companies provide, we believe valuations for this sector as a whole have become too expensive to justify continued investment.

We also sold our positions in Hertz and Gilead.

Hertz provides car rental services in on-airport and off-airport locations across the United States. The company has been underperforming against its earnings potential, in our view. Sustained pricing improvement across the industry has remained elusive, however, and further rental fleet rationalization may be required. Although a turnaround still appears possible, Hertz’s recovery is likely to take more time and its earnings power appears less significant than initially anticipated. Accordingly, we decided to exit our position to fund other opportunities.

We completed the sale of our position in Gilead during the second quarter. We initially purchased Gilead in 2011 as the biotechnology company began expanding its product pipeline in the Hepatitis C market. Through acquisitions and product development, Gilead experienced tremendous sales and profit growth from 2013 to 2015, boosting its stock price by 400%. Over the past two years, we have reduced our position in the company because of the stock’s price appreciation. Gilead’s failure to map out its future growth plans prompted our decision to exit the holding completely and reallocate the capital into more compelling investments.

Equity Income

MLPs rebound as negative sentiment dissipates

Income-producing equity investments, such as Mortgage Real Estate Investment Trusts (mREITs) and Master Limited Partnerships (MLPs), reported solid gains during the quarter. The FTSE NAREIT Mortgage REITs Index posted a second-quarter total return of 9.7% (14.3% YTD), while the Alerian MLP

Index increased 19.7% during the quarter (14.7% YTD).

As we noted last quarter, the MLP sector was extremely oversold earlier in the year because of the collapse in oil prices and trepidation over the sustainability of MLP dividends. Those concerns proved exaggerated, and we believe the negative investor sentiment that continues to hover over the sector will dissipate as MLPs’ midstream energy assets demonstrate their worth in this commodity environment. We believe this asset class is in the initial phase of a long-term recovery that will generate substantial returns for MLP investors over the next two to three years.

Fixed Income

Yields plummet as Brexit prompts investors to seek safety

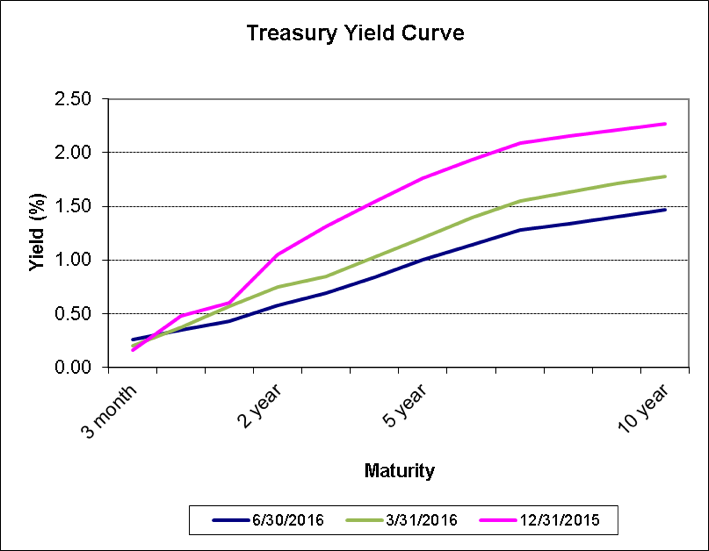

Interest rates in the U.S. declined to historically low levels in the second quarter, as the uncertainty created by Britain’s vote to exit the European Union sent investors to seek safety. Yields on the 10-year U.S. Treasury bond declined to about 1.4%, more than three-quarters of a point lower than where it began the year. As a result of the economic uncertainty, the Fed is unlikely to raise short-term interest rates in the near future.

A lack of new supply continues to make municipal bonds relatively attractive compared with taxable bonds. Corporate bonds are the most attractive taxable bond sector, as declines over credit quality concerns have led to attractive risk-adjusted yields.

Source: Bloomberg

Alternatives

Private Equity investment remains slow as valuation levels continue to rise

Most Hedge Funds continued to post relatively flat results during the second quarter. Macro-oriented managers who positioned their portfolios correctly in commodities and global bonds posted the best returns. U.S. credit managers also performed well, since credit spreads narrowed as fears of an economic recession declined. With investors chasing stocks with strong yields and selling companies that benefit from higher interest rates, long/short equity managers have struggled this year with holding too few consumer staples and utilities and too many financials. Finally, there is an interesting shift in hedge fund assets from directional strategies to market-neutral strategies with more short exposure. As valuations rise, the opportunity to make money on long and short positions increases.

Low interest rates continue to support nearly every sector of the Real Estate market. As investors search for yield, well-located properties with high occupancy and strong cash flow distributions have attracted significant demand. While apartments and multifamily housing remain the favored sector, other niche sectors to watch include senior living, student housing, self-storage and medical office buildings, which are all benefiting from supportive demographics. With interest rates expected to stay low because of subpar global growth, owning real estate remains attractive.

The Private Equity market has been strong in 2016, but not without its challenges. Concerns over rising valuation levels and the effect they may have on future returns is clearly at the forefront of both fund managers’ and investors’ minds. The amount of capital waiting to be invested in private equity continues to grow. According to a recent Prequin survey, private equity funding available for investment is triple the amount of capital called in the previous year. Hence, investors need to be patient in selecting opportunities for fear that even if the private equity manager identifies an attractive growth opportunity, industry-wide valuation declines could result in subpar returns. To overcome this potential hurdle, managers are focusing on self-liquidating private debt investments, which should be less reliant on friendly capital markets to achieve results.