The fears that had cast a pall over January weighed on the markets in early February as well, but sentiment improved sharply as the month progressed. The Bank of Japan’s (BOJ) move into negative policy rates led to concerns of policy exhaustion, which further muddled the macro backdrop. However, comments from central bankers, solid U.S. economic fundamentals and a turn higher in oil prices underpinned a dramatic shift in sentiment.

Encouraging U.S. economic data contributed to an improvement in global risk appetite. Consumption patterns and even manufacturing trends were better than anticipated. In addition, various measures indicated a trend toward higher inflation.

Investors marveled at yet another V-shaped trajectory in the markets in February, but concerns still lingered. After another sharp sell-off to start the month, most risk assets retraced much of their losses by month-end. Still, the dramatic improvement was not enough to counter the declines in risk assets for the year so far, suggesting investors remained anxious about the challenges facing the global economy.

In the world

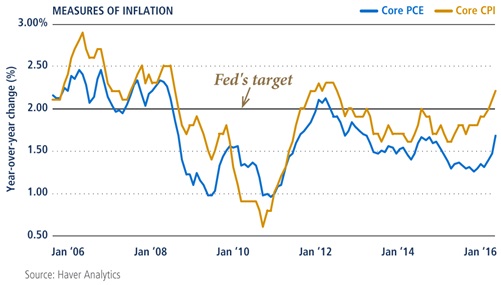

INFLATION TRENDS TAKE A TURN FOR THE BETTER

Core inflation data (excluding food and energy) as measured by both CPI and PCE are now clearly on an upward trend. January’s data releases helped confirm this trend in two ways: The monthly increases beat consensus expectations and the prior-month’s gains were revised up. While the Federal Reserve's (Fed) preferred measure (core PCE) remains below its 2% target, the trend is encouraging for the Fed given its long-fought battle to dispel fears of deflation. Looking ahead, as the economy reaches full employment, job growth may slow but should be accompanied by an increase in wages – which is a key, but thus far largely absent, part of the inflation pipeline.

Although January’s fears seeped into February, market sentiment improved sharply as the month progressed. Global growth and deflation fears gained momentum at the start of the month as the BOJ introduced negative interest rate policy. While the move was intended to calm markets, it appeared to do the opposite: Investors began to focus on the potentially adverse consequences of negative rates and the possibility that central bank policies were reaching the limits of their effectiveness. With oil prices declining, concerns over Chinese policy lingering and U.S. recession worries gaining steam, strongly negative sentiment gripped markets and another bout of volatility ensued. Just as dramatic as the sell-off in risk assets was the shift in sentiment in the second half of the month. While there was no single catalyst, a number of factors supported the change. First, Federal Reserve Bank of New York President William Dudley dismissed concerns about the likelihood of negative interest rate policy in the U.S. and highlighted domestic growth momentum. Second, People’s Bank of China (PBOC) Governor Zhou gave a rare interview and provided some clarity around China’s currency policies, stating that he saw no basis for further currency depreciation. Third, speculation that oil producers were holding discussions on potential output adjustments sparked a rally in oil markets.

Global risk appetite during the second half of the month was further bolstered by indications that the U.S. economy remained healthy. While markets have frequently questioned the resiliency of the U.S. economy during the seven-year (and counting) economic expansion, data in February largely depicted a healthy economy. In fact, some of the data released during the month actually exceeded expectations. Concerns over a possible recession in the U.S. manufacturing sector abated somewhat as both factory and survey data showed improvement, suggesting that recent weakness may not be indicative of a prolonged retrenchment. Retail sales data revealed that cheaper gas and a strong labor market – with the unemployment rate below 5% and wages rising faster than expected – continued to encourage consumer spending. Perhaps the most encouraging sign, though, was the trend higher in inflation. Core CPI posted its third straight year-over-year improvement with a 2.2% pace, while core PCE (the Fed’s preferred measure) moved up to 1.7% year-over-year, its strongest pace in three years.

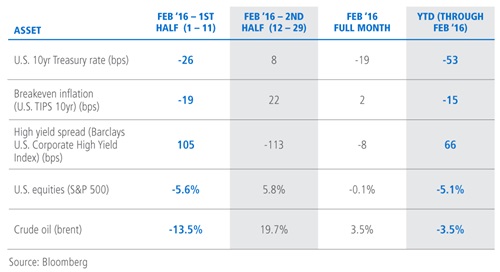

Despite the shift in sentiment and dramatic rally, investor anxiety was still evident. The impressive rally later in the month was all the more noteworthy considering how much recession fears dominated financial markets in the first half of the month. In the first 11 days of February, the U.S. 10-year Treasury rate was driven to a one-year low of 1.66% – a full 60 basis points (bps) below year-end levels – while inflation expectations (derived from inflation-linked securities) fell to post-crisis lows, global equities1 dropped more than 5% and high yield spreads2 widened more than 100 bps. Yet the subsequent rally was equally striking: Equities erased much of the month’s losses, high yield spreads actually ended the month tighter and inflation expectations were higher. Still, most asset markets remained worse off for the year, which signaled lingering market unease. Perhaps most telling, bond market yields remained lower on the month despite the shift in risk appetite, suggesting that the fears dominating the early part of the month hadn’t dissipated so much as moved to the background.

In the markets

‘V’ FOR VOLATILITY

Most risk assets experienced a V-shaped trajectory in February as the global pessimism that gripped markets in the early weeks of the month faded steadily through month-end and risk appetite returned. While investors had become increasingly concerned about global growth and the potential for a near-term recession, reassuring rhetoric from central bankers and a turn higher in oil prices contributed to a shift in sentiment, as did a better tone in economic data. Ultimately though, the rally in risk assets served only to offset the initial sell-off in early February, and did little to retrace the damage done in January. Only time will tell if global economic trends will sustain investor sentiment and bring about a full reversal of the sluggish start to 2016.

DEVELOPED MARKET DEBT

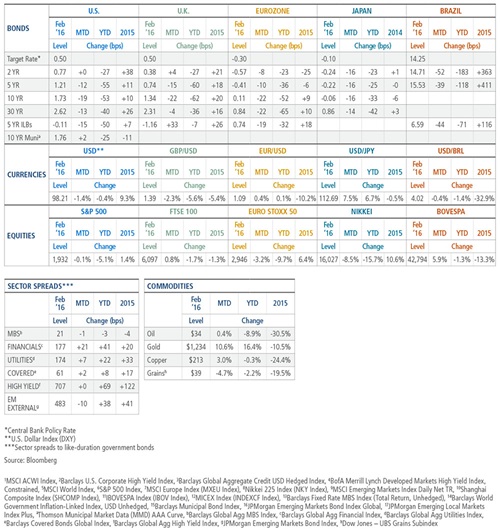

Global recessionary fears and negative central bank policy rates created weak sentiment and drove developed market yields broadly lower during February. Although sentiment recovered during the month’s second half, yields remained low. Ten-year yields in the U.S., eurozone, UK, Japan and Australia were lower by 15 bps and 25 bps over the month. Eurozone peripheral yields, which were flat to somewhat higher, proved the only exception. While U.S. economic data continued to reveal domestic strength, market expectations for a March interest rate hike from the Fed were negligible given the weaker external environment. Elsewhere, markets continued to expect additional accommodation from the European Central Bank (ECB) at its March meeting, while fears that Britain may leave the EU (Brexit) drove demand for UK gilts. Finally, Japanese yields dropped on fallout from January’s surprise easing from the BOJ and expectations for additional action in March.

CREDIT

Global investment grade credit spreads3 widened 4 bps in February but finished the month on a strong note, retracing much of the widening in the first half of February thanks to an oil-fueled rally and a rebounding equity market. Global investment grade credit returned 0.7%, given falling global government bond yields, and fundamentals outside of commodity-related sectors remained supportive of valuations looking forward.

February was a tale of two halves for global high yield,4 with the first half down alongside higher equity volatility and lower oil prices and the second half up on a sharp improvement in commodities, signs of stability in global banks and improving U.S. economic data. Spreads ended the month flat, but returns were positive for the first time in four months.

DEVELOPED MARKET EQUITIES

After a volatile month, developed market equities5 ended down 0.7%. They began the month in steep decline and then rallied into month-end on positive economic data out of the U.S. and speculation of additional monetary easing in Asia and Europe. U.S. equities6 followed the path down and up, amid improving consumer data, but returned -0.1% for the month as a whole. In Europe, equities7 declined 2.1% as inflation remained weak across the region, raising speculation that the ECB would review and possibly reconsider its current monetary policy. Japanese equities8 declined significantly, returning -8.4% as the stronger yen and questions around the effectiveness of BOJ policies fueled risk-off sentiment.

EMERGING MARKET EQUITIES

In emerging markets, equities9 ended slightly down, returning -0.2% amid mixed returns at the country level. Chinese stocks10 returned -1.8% as additional easing measures and rare comments made by the PBOC in defense of the yuan relieved some worry around the Chinese economy. In Brazil, stocks11 rallied 5.9% during the month despite an additional credit rating downgrade by Moody’s. A nascent reduction in concern around China’s growth outlook eased demand concerns for Brazil’s export-driven economy. Russian equities12 advanced 3.1% as rising oil prices lifted the value of assets in the world’s biggest energy exporter.

MORTGAGE-BACKED SECURITIES

Agency mortgage-backed securities (MBS)13 underperformed like-duration Treasuries by 14 bps. Underperformance was particularly noticeable for securities with coupons in the middle of the range because they are the most vulnerable to prepayments. Ginnie Mae MBS underperformed conventional MBS due to supply pressure, and 15-year MBS marginally outperformed 30-year MBS. Prepayment speeds announced at the beginning of the month declined, but the average refinancing index level during February jumped more than 50% as mortgage rates fell. Non-agency MBS prices declined amid the broader market volatility, with year-to-date performance largely in line with broader credit markets. However, market technicals remain favorable, collateral performance has been stable and housing fundamentals should be well insulated from global macroeconomic concerns.

INFLATION-LINKED DEBT

Global inflation-linked bonds (ILBs)14 almost universally lagged nominal sovereign bonds as inflation expectations slid lower in February, despite the rebound in oil prices and other risk assets over the latter half of the month. U.S. Treasury Inflation-Protected Securities (TIPS) were the exception, ending roughly in line with nominal Treasuries after inflation expectations rebounded mid-month from their lowest levels since the global financial crisis. U.S. breakeven inflation (BEI) was supported by stronger-than-anticipated data on wages and the CPI, as well as the modest improvement in oil prices. In contrast, eurozone breakeven rates were plagued by supply pressures throughout February and plunged lower into month-end as the initial February HICP data slipped back into deflationary territory. UK breakevens were similarly pressured by supply as well as disappointing inflation readings.

MUNICIPAL BONDS

Municipals15 posted gains but gave back some of their recent outperformance relative to Treasuries and corporate bonds over the past few months. Yields dipped near all-time lows early in the month as a flight to quality prevailed in the market, but intermediate and long-term muni rates ended higher after sentiment shifted mid-month. Technicals remained supportive: Muni funds took in $4.2 billion, continuing a trend of strong demand and supply picked up after January’s muted levels, but year-to-date issuance remained roughly 10% below that of 2015.

In credit news, discussions picked up in Washington around a solution for Puerto Rico’s debt crisis. The U.S. Treasury weighed in with a plan for a federally appointed oversight council and a “Super Chapter 9” bankruptcy process. The proposal was met with mixed opinions by market participants, as it explicitly prioritizes pensioners over bondholders.

EMERGING MARKET DEBT

Emerging market assets gained, as tighter index spreads and lower U.S. Treasury yields aided external debt,16 while generally lower yields and stronger currencies propelled local currency debt.17 Across external debt, high-yielding Latin American and African bonds led the way as commodity prices firmed during the month’s second half. The gains in external debt for commodity exporters, however, did not translate into local currency strength – exporter currencies remained weaker at month-end, whereas the currencies of European commodity importers held gains from earlier in the month. Elsewhere, the Mexican central bank surprised markets with a 50-bp hike designed to support the currency. Finally, S&P and Moody’s both downgraded Brazil, citing a weaker fiscal anchor and high debt servicing costs as factors. Oil exporters Saudi Arabia and Kazakhstan were also downgraded.

COMMODITIES

Commodities posted marginal losses in February as declines in energy and agriculture overwhelmed gains in precious and industrial metals. Natural gas underperformed within the energy sector on warm weather and strong production numbers. Brent crude oil ended the month relatively flat, albeit with quite a bit of intra-month volatility, while WTI sold off on heavy imports into the U.S. With the exception of sugar, which gained nearly 10%, the majority of the agriculture complex faced headwinds in part from an impending South American harvest. Gold was the top performer for the month, supported by continued safe-haven demand amid market uncertainty and macro weakness. Industrial metals were volatile throughout the month but ended on a positive note in part because of favorable PBOC actions.

CURRENCIES

The U.S. dollar ended February slightly weaker against most major currencies despite a strong rally in the second half of the month. Technical headwinds and weak U.S. manufacturing data pushed the dollar down before positive economic data pulled it back up mid-month. The Japanese yen surged as risk-off sentiment early in the month outweighed surprise accommodation by the BOJ in late January. In Europe, the euro gained modestly despite expectations of additional ECB easing in March, while the pound sterling slipped on Brexit fears. The rebound in commodity prices in the second half of the month helped select developed market currencies (Canada, Australia), although emerging market commodity importers (Poland, Israel) tended to outgain exporters (Russia, Mexico). In Asia, the Chinese yuan was steady, but the Indian rupee dropped due to foreign outflows and the Korean won weakened on geopolitical tensions.

Outlook

PIMCO expects the world’s major economies to continue converging in 2016 while central bank policies diverge. The U.S. recovery will remain on a fairly stable trajectory. Growth in Europe and Japan is projected to increase only modestly, while BRIM (Brazil, Russia, India, Mexico) economies should see gradual improvement. The Fed will maintain its bias toward raising rates, but most other central banks will likely ease policy through rate cuts or quantitative easing (QE), or at least keep rates on hold.

In the U.S., our baseline expectation is for slightly above-trend economic growth of 2.0%–2.5% over the year with underlying inflation of 1.5%–2.0%. With job growth expected to slow as the economy reaches full employment, personal spending will be tied more closely to real wages, which should improve modestly. Given soft global demand and a strong U.S. dollar, we anticipate little boost from international trade. On the positive side, government spending will provide a modest fiscal boost. We believe the market remains too sanguine about the potential for rate hikes in 2016, though the Fed will continue to be data-dependent and mindful of international developments.

For the eurozone, we anticipate above-trend GDP growth of about 1.5%. The ECBʹs ongoing QE measures will keep bank lending rates low across both core and peripheral countries, boosting loan growth. Similarly, modestly improving sentiment and employment should support domestic demand. Headline inflation will depend on the path of oil prices and the euro, but core inflation is likely to remain below the ECB’s definition of price stability. Persistently below-target inflation should open the door to expansion of the existing easing program.

Japanese GDP growth should increase modestly to about 1% in 2016. The slowdown in China and other trading partners will remain a headwind to net exports, and domestic policies have not provided the boost many hoped for. That said, Japan’s shift in fiscal policy goals – an important new development – could be supportive of stronger growth. Headline inflation could advance toward 1%, but will likely remain below the BOJ,s target of 2%. Amid concern that the quantitative and qualitative easing (QQE) program could run up against technical limits, the BOJ introduced negative interest rates in late January, but the implications for inflation and growth remain unclear.

Our outlook for China is little changed with expectations for growth around 6% and headline inflation about 2%. We still believe China possesses the “will and the wallet” to deal with the challenges of slower growth and pivot toward a service economy; however, the task is difficult and policy mistakes are still possible. We anticipate additional easing via cuts to the deposit rate and required reserve ratio. We also see a likely rise in the budget deficit due to quasi-fiscal financing of local public works as China uses leverage to support its economy in the near term.

We expect BRIM growth to increase modestly to 1.25%–2.25%. An important driver of our lower-than-consensus forecast is the extended contraction in Brazil, given the sharp drop in confidence and elevated political uncertainty. Russia is also expected to contract in 2016, albeit at a slower pace than previously. Meanwhile, both India and Mexico should grow in line with consensus. We forecast 2016 headline CPI inflation in BRIM at 6% (consensus at 5.9%), but Brazil remains the outlier with higher-than-consensus inflation.

Of Note

U.S. RECESSION? THE NUMBERS DON’T ADD UP

Risk of a U.S. recession in 2016 has been on the rise in recent months – or at least that is what the press would have you believe. The data does show a deceleration: U.S. GDP growth slowed from 2.5% in 2014 to 1.9% over the four quarters of 2015, with Q4 growth at just 1%. And markets appeared to question the Fed’s December rate hike: Treasury rates rallied, equities sold off and credit spreads widened.

Aside from the gloomy sentiment, what does the data tell us? Both of PIMCO’s models that examine the likelihood of recession suggest the probability is higher than it has been in a while. But a closer look confirms that the risk of recession remains low and is still significantly lower than at the onset of previous recessions. In addition, the economy has so far shown none of the typical warning signs that preceded past recessions: no overconsumption, no overinvestment and no overheating. Nor are there any signs of overkill by the Fed, which has contributed to past downturns. In our view, fears of a recession in 2016 are overdone.

Appendix

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results.

A word about risk: All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk and liquidity risk. The value of most bonds and bond strategies is impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Equities may decline in value due to both real and perceived general market, economic and industry conditions.Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. It is not possible to invest directly in an unmanaged index.

This material contains the current opinions of the manager and such opinions are subject to change without notice. This material is distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Statements concerning financial market trends are based on current market conditions, which will fluctuate. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

PIMCO provides services only to qualified institutions and investors. This is not an offer to any person in any jurisdiction where unlawful or unauthorized. | Pacific Investment Management Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660 is regulated by the United States Securities and Exchange Commission. PIMCO Investments LLC, U.S. distributor, 1633 Broadway, New York, NY 10019 is a company of PIMCO. | PIMCO Europe Ltd (Company No. 2604517), PIMCO Europe, Ltd Amsterdam Branch (Company No. 24319743), and PIMCO Europe Ltd - Italy (Company No. 07533910969) are authorized and regulated by the Financial Conduct Authority (25 The North Colonnade, Canary Wharf, London E14 5HS) in the UK. The Amsterdam and Italy branches are additionally regulated by the AFM and CONSOB in accordance with Article 27 of the Italian Consolidated Financial Act, respectively. PIMCO Europe Ltd services and products are available only to professional clients as defined in the Financial Conduct Authority’s Handbook and are not available to individual investors, who should not rely on this communication. | PIMCO Deutschland GmbH (Company No. 192083, Seidlstr. 24-24a, 80335 Munich, Germany) is authorized and regulated by the German Federal Financial Supervisory Authority (BaFin) (Marie-Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with Section 32 of the German Banking Act (KWG). The services and products provided by PIMCO Deutschland GmbH are available only to professional clients as defined in Section 31a para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication. | PIMCO (Schweiz) GmbH (registered in Switzerland, Company No. CH-020.4.038.582-2), Brandschenkestrasse 41, 8002 Zurich, Switzerland, Tel: + 41 44 512 49 10. The services and products provided by PIMCO Switzerland GmbH are not available to individual investors, who should not rely on this communication but contact their financial adviser. | PIMCO Asia Pte Ltd (501 Orchard Road #09-03, Wheelock Place, Singapore 238880, Registration No. 199804652K) is regulated by the Monetary Authority of Singapore as a holder of a capital markets services licence and an exempt financial adviser. The asset management services and investment products are not available to persons where provision of such services and products is unauthorized. | PIMCO Asia Limited (Suite 2201, 22nd Floor, Two International Finance Centre, No. 8 Finance Street, Central, Hong Kong) is licensed by the Securities and Futures Commission for Types 1, 4 and 9 regulated activities under the Securities and Futures Ordinance. The asset management services and investment products are not available to persons where provision of such services and products is unauthorized. | PIMCO Australia Pty Ltd ABN 54 084 280 508, AFSL 246862 (PIMCO Australia) offers products and services to both wholesale and retail clients as defined in the Corporations Act 2001 (limited to general financial product advice in the case of retail clients). This communication is provided for general information only without taking into account the objectives, financial situation or needs of any particular investors. | PIMCO Japan Ltd (Toranomon Towers Office 18F, 4-1-28, Toranomon, Minato-ku, Tokyo, Japan 105-0001) Financial Instruments Business Registration Number is Director of Kanto Local Finance Bureau (Financial Instruments Firm) No. 382. PIMCO Japan Ltd is a member of Japan Investment Advisers Association and The Investment Trusts Association, Japan. Investment management products and services offered by PIMCO Japan Ltd are offered only to persons within its respective jurisdiction, and are not available to persons where provision of such products or services is unauthorized. Valuations of assets will fluctuate based upon prices of securities and values of derivative transactions in the portfolio, market conditions, interest rates and credit risk, among others. Investments in foreign currency-denominated assets will be affected by foreign exchange rates. There is no guarantee that the principal amount of the investment will be preserved, or that a certain return will be realized; the investment could suffer a loss. All profits and losses incur to the investor. The amounts, maximum amounts and calculation methodologies of each type of fee and expense and their total amounts will vary depending on the investment strategy, the status of investment performance, period of management and outstanding balance of assets and thus such fees and expenses cannot be set forth herein. | PIMCO Canada Corp. (199 Bay Street, Suite 2050, Commerce Court Station, P.O. Box 363, Toronto, ON, M5L 1G2) services and products may only be available in certain provinces or territories of Canada and only through dealers authorized for that purpose. | PIMCO Latin America Edifício Internacional Rio Praia do Flamengo, 154 1o andar, Rio de Janeiro – RJ Brasil 22210-906. | No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. PIMCO Investments LLC, distributor, 1633 Broadway, New York, NY 10019, is a company of PIMCO.

© 2016 PIMCO

© PIMCO