The chart that matters the most today?

Source: Bloomberg

“Foreign-exchange reserves are assets held by a central bank or other monetary authority, usually in various reserve currencies, mostly the United States dollar, and to a lesser extent the euro, the pound sterling, and the Japanese yen, and used to back its liabilities” Definition of forex reserves by Wikipedia.

The past 15 years have been marked by unprecedented accumulation of foreign-exchange reserves. Emerging economy central banks, led by China and the oil-producers, built up a rich chest of forex reserves to build a buffer against external shocks after having learnt their lessons in the Asian financial crisis, adding more than $10tn in the last 15 years. This accumulation came to a brief halt during the height of the financial crisis in 2008 but recovered sharply thereafter. So, except for a brief while during the financial crisis, the EM world hasn’t seen erosion in their foreign reserves up until recently. Corporates and governments in many of the EM economies have substantial foreign currency debt (helped by easily available cheap dollar credit) without adequate backing of forex reserves. Led by China, emerging markets, notably Russia and Saudi Arabia, have also called on their rainy-day stashes. In a world where petro dollars is dying, Saudi Arabia, the world’s largest exporter of crude oil had to dip into its forex reserves for support. A large European bank estimates that developing countries, which hold about two-thirds of global reserves, spent a substantial chunk of their forex reserves in 2015 up until now, the most since the global financial crisis in 2008. The trend is likely to continue as oil prices stay low and growth in emerging markets remains weak, reducing the dollar inflows that central banks used to build reserves and conduct monetary policy.

So one may ask, what is the big deal? In simple terms, reserve accumulation adds money supply to the financial system - each dollar purchase creates a corresponding amount of new local currency and helps stimulate the economy through investments in physical/financial assets. Most economies used forex inflow to buy US treasury and other productive assets through sovereign wealth funds. When there is a drawdown on reserves, these assets (investments in productive assets) need to be liquidated to pay back the dollar. This creates a dictum on asset prices globally which come under pressure on desperate selling.

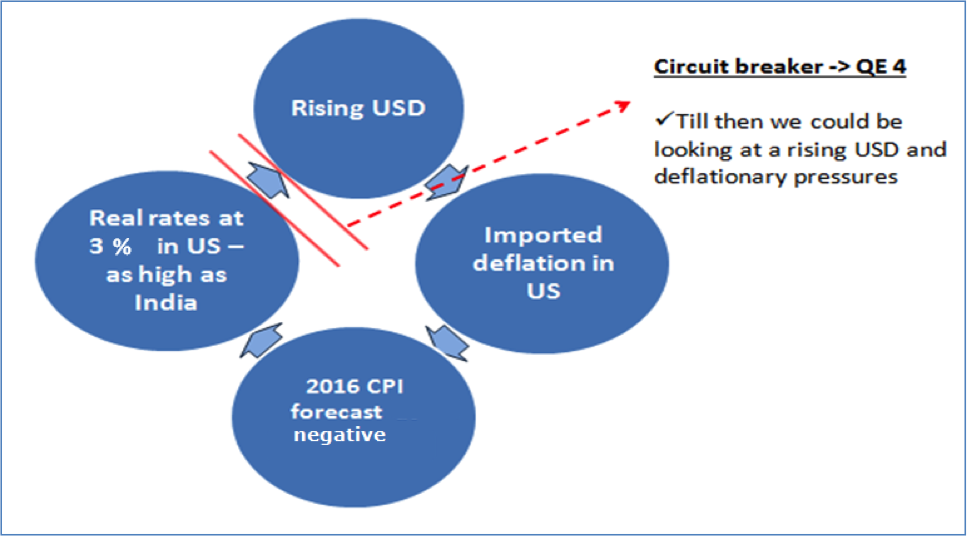

The drawdown on forex reserves is an additional source of uncertainty in a world already plagued by volatility. The weak commodity cycle has forced commodity exporters dipping into their reserves to make up for lower incremental dollars from export of commodity/energy and this, in my opinion will be the strongest trigger for the next leg of the dollar rally. A bye effect of a firming dollar is the deflationary effect it has on commodity price, thereby leading to pronounced imported deflation in the US. As per estimates by Gavekal research, if the dollar rally goes unchecked, we could be looking at US CPI inflation dropping into negative territory by early 2016 implying US real rates near 3%, as high as India which will in turn, provide a boost to the dollar rally. In short, conditions are ripe for a sharp dollar rally and the resulting interplay of bond yields and CPI will further push up the dollar. Not to forget that US is the only economy looking to raise interest rates in a developed world obsessed with lowering and negative interest rates. This will only increase the allure of the dollar further. The only circuit breaker is a QE 4 but we know it will not be easily forthcoming so a dollar rally looks quite probable and so are the deflationary pressures.

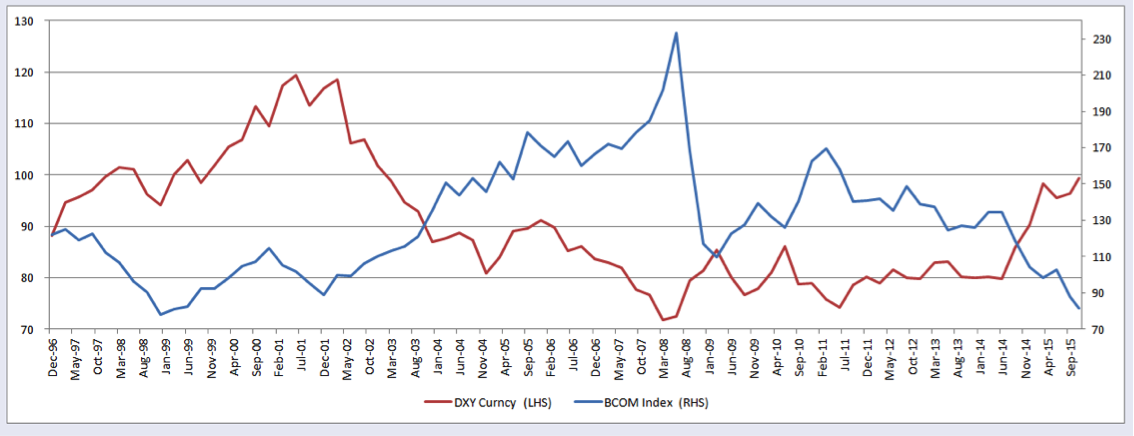

Commodity prices and dollar index have move in opposite direction

Source: Bloomberg

BCOM - Bloomberg Commodity Index

DXY – Dollar Index

A QE4 looks like the lone circuit breaker for a deflationary pressures and rising real rates in US

Petro dollars a critical determinant of global liquidity or rather illiquidity?

Source: Barclays Research

Ben Bernanke expressed the relationship between reserves and bond yields memorably in 2005 in his ‘global savings glut’ hypothesis. Large current-account surpluses among emerging markets were a reflection of excess national saving. The surplus capital had to go somewhere. Much of it was channeled by central banks into developed market bonds held in their burgeoning reserves. The growing stockpiles of bonds compressed interest rates in the developed markets.

In a dwindling forex reserve scenario, emerging market economies could find it tougher to boost their money supply and shore up faltering economic growth. While central banks have other ways of pumping cash into the banking system, such moves without the backing of increased foreign reserves could end up weakening their currencies further - an outcome they may want to avoid. The swing in global foreign exchange reserves is one key measure of the global liquidity tap being turned on and off. When a regime of loose money suddenly ends, emerging-market asset prices are usually one of the first casualties. India however stands out in a weakened EM basket having boosted its forex reserves when most economies (especially commodity export dependent economies) had to draw down on their reserves, thereby creating a safety buffer in an increasingly volatile world. Regulatory curbs on foreign ownership have ensured that our bond market has been rather resilient during the recent turmoil compared to the volatility seen in most EM bond markets which have higher foreign ownership.

Disclaimer: The views expressed in this article are personal in nature. It does not construe to be any investment, legal or taxation advice. Any action taken by the reader or recipient on the basis of the information contained herein is reader’s/recipient’s responsibility alone and Tata Asset Management Limited will not be liable in any manner for the consequences of such action taken by reader/recipient.