I was talking with a friend the other day about troubles in his family. At one point he remarked, “A mother is only as happy as her saddest child.” It’s a saying that has been attributed to Jackie Kennedy (and that is certainly understandable), but I think it goes much further back in time. My wife said her mother used to say it when she was growing up.

I can’t say that I have ever heard it before, but I know from experience exactly what is meant by it. My younger brother had all kinds of difficulties during his short life. Yet when he died (at 49), each of his siblings eulogized about how Tom was Mom’s favorite. It’s just natural for a mom to want to nurture the child that is struggling.

I don’t think this tendency to support the underdog is restricted to moms, though. In the US, it is almost the national norm to back the underdog. Who do you root for at the movies?

There was a famous research experiment conducted in 1991 at Bowling Green State University by Frazier and Snyder, where students were asked to choose between two unidentified teams in a seven-game series, with one termed an over-whelming favorite. 81% chose the underdog. When they were then told after the first four games that the underdog was ahead, half of the students who had picked the underdog switched to the favorite. Then they were told the series was tied at three apiece. 84% chose the underdog.

Such is the persuasive power of underdog status in America. I think it goes back to the American sense of equality, of evening things out, and a respect for hard work and persistence, traits that have always been identified with

Americans.

Yet in investing, most of the time a different choice is made. Most of the strategies I have developed over the years are trend following by nature. As such, I may favor, as a rule, the favorites. And I think investors as a whole are inclined to abandon investment underdogs and favor the top performers. That’s a result of the “herding” instinct that we often speak of in behavioral finance.

However, in investing we have a concept like the underdog effect. It’s called “mean reversion,” and while that name is off-putting, it really just means that when something goes to one extreme it tends to return to its usual level of performance. Like a rubber band that’s stretched, when you let it go, it returns to its original shape (why don’t sweaters do that?).

This “mean reversion” effect is especially prominent in the behavior of strategies. The best performers in one period often turn out to be the worst performers in another. And when a strategy truly seems down and out, it often seems to spring back with outstanding performance.

This is the reason why we urge investors and their advisors to create portfolios that are diversified. And, it is why we say that you can’t achieve diversification by just picking the latest winning strategies. You need to mix in some of today’s losers to have some of tomorrow’s winners.

Those of you who closely follow the results of your portfolios and specific strategies within them may be confused as to why I would be talking about the losers. As you probably know, most of our strategies here at FPI have outperformed the S&P 500 since the market tops in May and July through last Thursday. In fact, my latest count shows that better than 90% have achieved this distinction.

Of course, beating the S&P 500 Index is not our – nor should it be your – standard of investment success. The true test is whether you are on track to achieve the goals established when you became an FPI client. This is documented in your OnTarget report. If your quarterly statement shows that you are outside of the red and in the yellow, green, or blue, you are OnTarget. I’d wager most of our clients will once again be so rated in the third-quarter reports currently being prepared.

But I wasn’t talking about the winners. I was talking about the losers—the less-than 10% of our strategies that may be underperforming the S&P. Once, perhaps, the favorites, they are now the underdogs.

I’m talking about strategies like STF, Managed Income Aggressive, and Wolfpack Aggressive. These did not fare as well in the latest downdraft. Should you abandon these underdogs and switch to the favorites?

I’d argue that this is probably the worst time to quit them. Each of these has a very good long-term track record. Each can deal with both further declines and a rebirth of a new bull market. If their decline in itself indicates any investor action, it would probably be to either hold on or buy more.

It’s the same with the stock market as a whole. We’ve been very bearish for some time now. The market has fallen substantially. The first correction (greater-than 10% fall) in years has occurred. But it is out of these types of ashes that new bull markets rise.

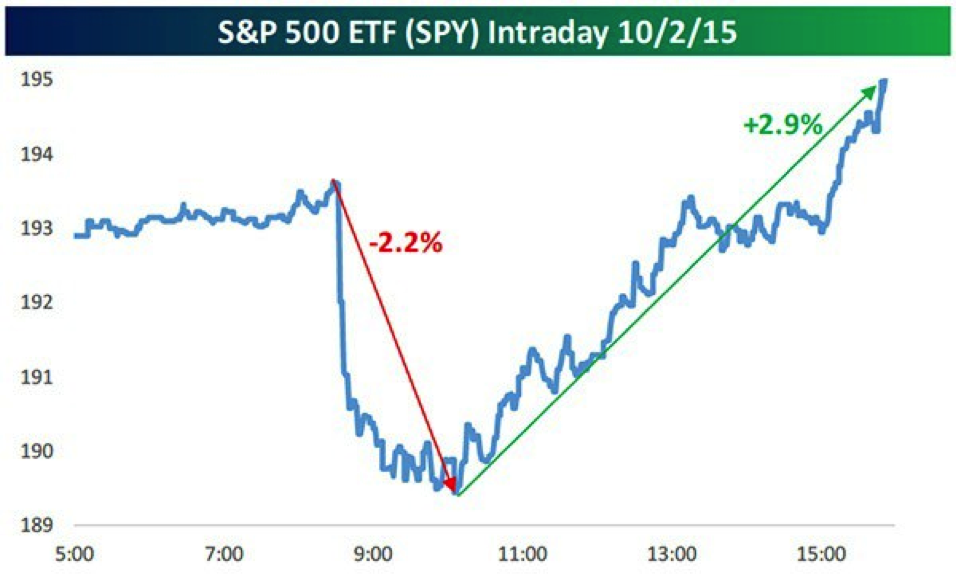

Friday’s intraday price reversal was indicative that support does exist for such a turnaround.

Source: Bespoke Investment Group

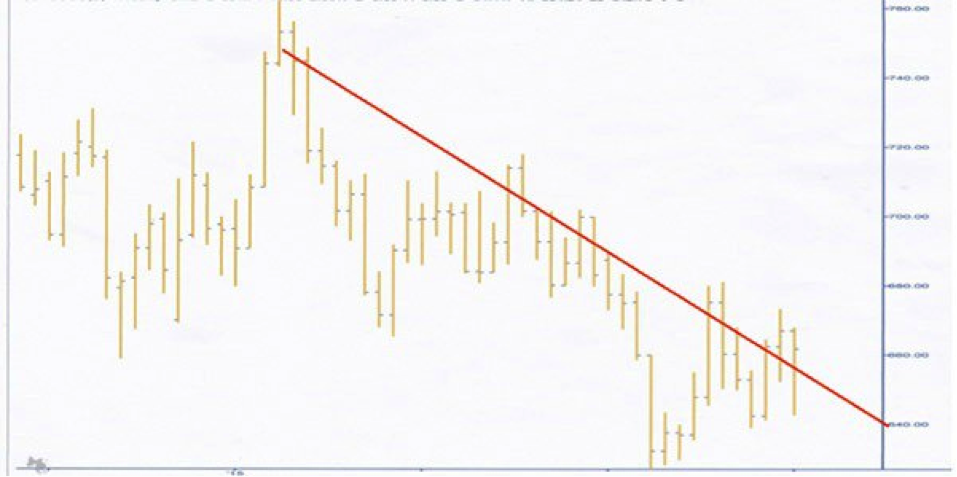

In addition, last Monday we tested the August lows that were the result of the dizzying decline that stocks experienced on August 24. The test was a successful one.

Source: Bespoke Investment Group

In addition, the Classic market timing sell signal that we wrote about weeks ago has now reversed and a buy on that strategy is now in place. Similarly, we are in a short-term positive seasonality period.

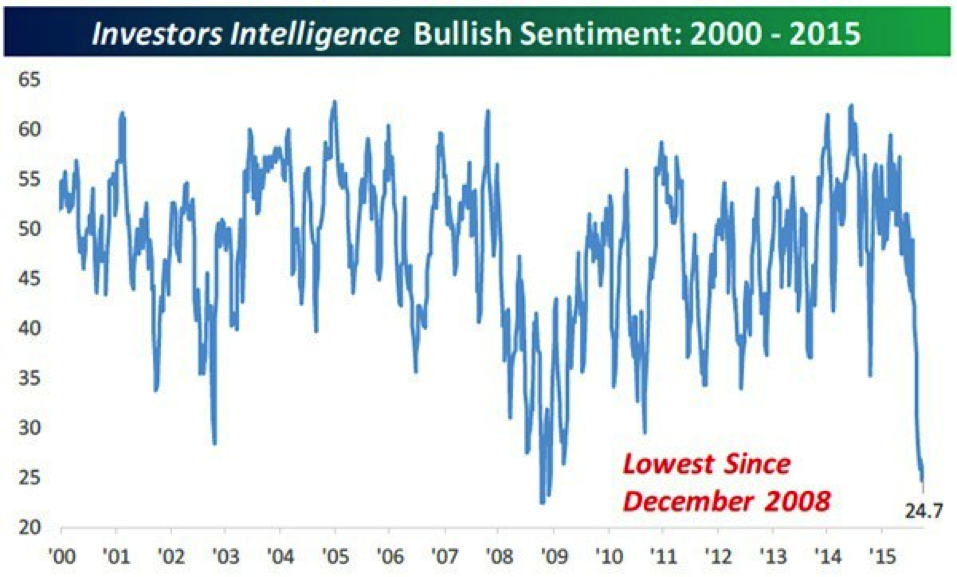

And when we talk about mean reversion, it is very evident in two of our favorite indicators. Both have gone to extremes not seen in years. In the past such readings have led to higher prices in the immediate future.

Source: Bespoke Investment Group

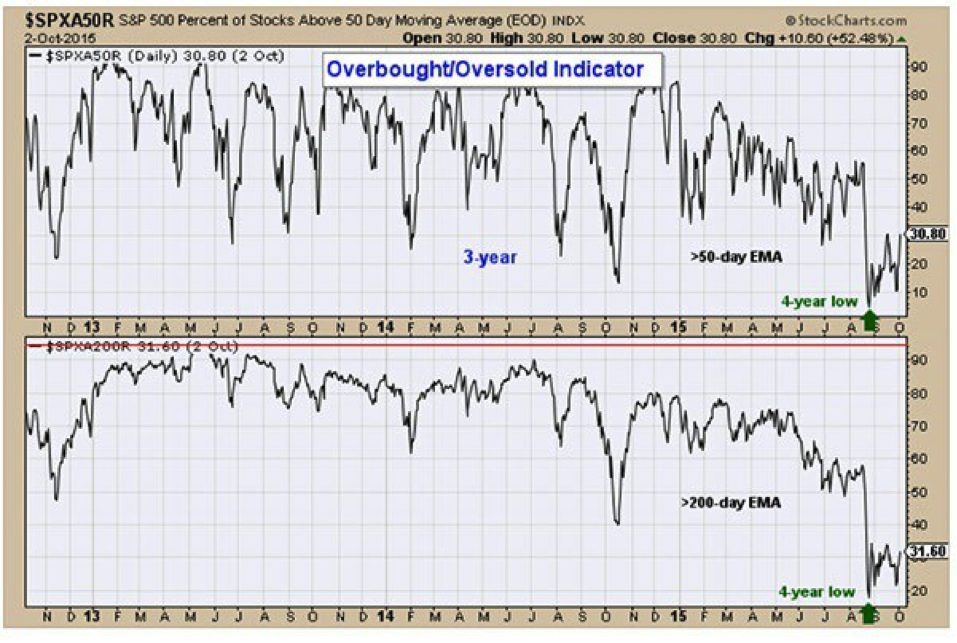

Percentage of Stocks above 50- and 200-day MA

Source: stockcharts.com

While these good omens seem to be showing up daily, it does not mean that the correction, or even the worst of the correction, is over. Most of our strategies remain defensively positioned.

Last week’s four up days combined with today’s rally leave stocks a bit overextended. Third-quarter earnings season (starting today), while I expect it to reinvigorate stocks when all is said and done, does leave open the likelihood of some further short-term volatility in the event of a high profile miss.

Economic indicators are sure showing little of a positive nature. Last week, of 25 economic reports, only seven surpassed expectations. And most are worse off than they were a year ago.

Still, interest rates are actually falling and commodity prices seem to be stabilizing (have you been watching oil and gold’s ascent?). My contrarian projection when the year began that the Fed will not raise interest rates this year is becoming ever more accepted by the investment community. And, finally, there remains little support for a recession that could cause the next bear market.

In this environment, I, like your mother before me, look to the unhappy ones to provide added support, but I also realize that the rest of the children have to be listened to as well.

All the best,

Jerry