While I was training early this morning, I was forced to endure two hours of CNBC’s seemingly permanent headline across the bottom of the screen that screamed that the markets were heading for a “massive sell off.” At the time, the Dow Jones Industrial Average futures were down about 500 points. When the markets opened at 9:30, the Dow did open down about 500 points (thereafter it actually was down about 1,000 points) before bouncing back to its opening levels.

I shouldn’t have been surprised by the hyperbole as the weekend was spent reading other media headlines using words like “huge” and “worst” to describe aspects of last week’s stock market action. I know such embellishment sells newspapers and garners ratings, but it really has gotten out of hand, and worse, it scares people when they have no reason to be scared.

Back in 1987 we had a down 500-point-plus open, but that was deservedly scary. Why the difference? In 1987, the Dow had closed at 2,246.76 the Friday night before the October 19th plunge. Yup, that’s right – that 500-point-plus drop made for a frightening 25% nose-dive.

Today’s 500 points follows Friday’s close of 16,459.75. So that works out to a 3.03% stumble. Even the 1,000 points in its brief life only translates to 6.07%. That’s just one-quarter of the 1987 crash and is hardly “massive.”

These gap-down openings are not all bad in any case. Today the S&P 500 was down 4.72% on the open. Panicky selling is rarely good. Instead, it usually offers a good time to buy.

The S&P 500 ETF (SPY) has been around since 1993. That means it has seen its share of corrections and true bear markets. Before today there have only been three instances when the market gapped open down 4% or more. One day later in each case the ETF was up over 3% from the previous day’s open. And one month later the SPY was up 1.15% to 16.4%.

If we narrow the gap to 3% to increase the number of occasions, the picture is little changed. Buying the gap in these circumstances led to gains over 77% of the time with an average return of almost 5% by month’s end.

The same goes for poor weekly returns. Yes, the S&P 500 tumbled 5.63% last week. Yet, on average, whenever the Index has fallen 5% or more since 1980, the average and median returns have been up over the next 1-, 4-, and 12- week periods with gains registered 60 to 70% of the time! Thanks to the Bespoke Investment Group for these statistics.

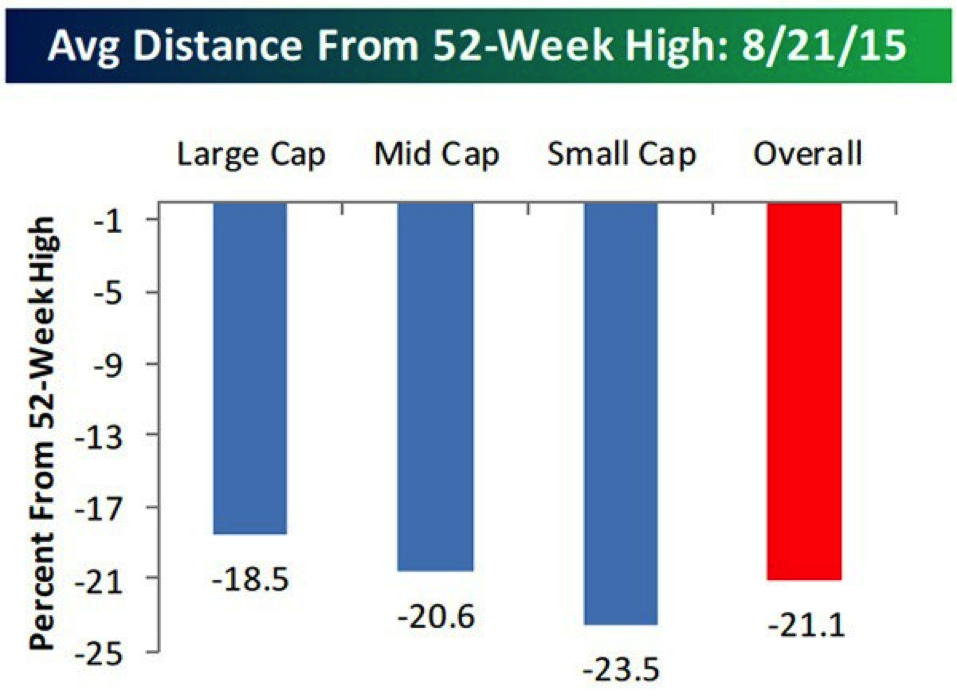

At Friday’s close, the S&P 500 was down 7.5% from its all-time high set just three months ago (May 21). But as we pointed out over the last two weeks, the average stock has fallen considerably more from its highs. The average stock has already declined more than the 20% cutoff that is the demarcation for a bear market designation. This is one of the reasons we generally don’t trade stocks. Individually they tend to be more volatile than stock indexes and mutual funds.

Source: Bespoke Investment Group

At today’s worst point, the indexes, in contrast, were “only” in market correction territory (greater than 10%). The occurrence of a correction should not be a surprise to any of my readers. I have been saying we were long overdue for such an occurrence. I began this mantra in January and have repeated it at least monthly ever since.

But at the same time I have also been saying that when such occurs, it is not the time for long-term investors to sell, because there was as yet no evidence that such a happening was the prelude to a bear market like we saw in 2000 and 2007. I stand by that analysis.

Seventy percent of the S&P 500 companies beat analysts’ earnings expectations in the last reporting period that ended just a week or so ago. These same analysts are just starting to buy into what I have been telling you all year: the Federal Reserve is not likely to raise interest rates in September and that next year was more likely. Low rates tend to be good for stocks, as we have seen for six years now. And our economy, which has not been growing like gangbusters but has, at least, been growing, continues to surpass most of the rest of the world.

While a lot of international investors may have been abandoning dollar-denominated assets last week to offset losses at home, I wager they will return to our better returns and growth prospects in the future. I do think this is a big reason for the panic selling. It has been much worse overseas by a factor of about 50%. In addition, we had a massive imbalance of put and call options expiring in our options market on Friday. This technical factor exacerbated the Friday decline.

It is no wonder that investment sentiment is so low. Bulls are hard to find and bears are more plentiful. Similarly, the S&P 500 has rarely been so oversold – over four standard deviations in the technical parlance. I agree that there could be more decline to come, at least back to last October’s lows, but in the short term both of these factors generally lead to stock advances in the near future.

Even seasonality, which normally turns stocks sour in the fall, has a brief window of probable advancement until early September. (Did you notice our Political Seasonality strategy moved to cash in advance of last week, then moved back into stocks at Friday’s close?)

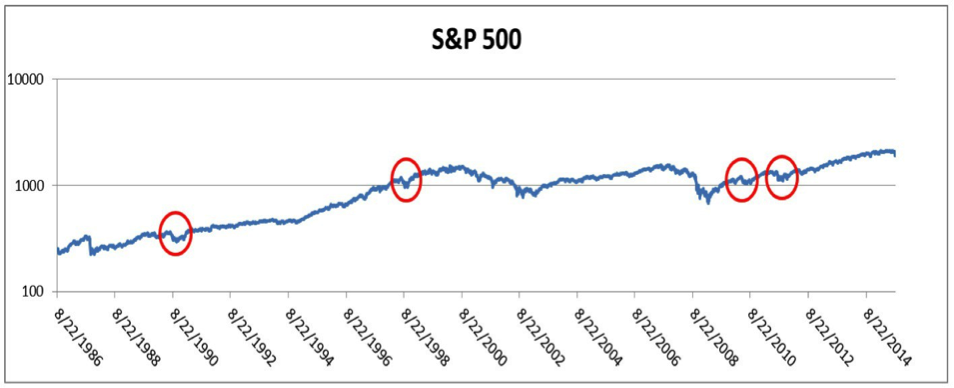

Finally, can we have a little perspective please? Here’s a chart of the last 30 years of the S&P through today’s close (in log scale to equalize the size of comparable percentage moves). I’ve circled the S&P 500’s drop in 1987 and then a few corrections along the way to the May 21st all-time high watermark. I was also going to circle the recent drop but it is so small in comparison that my drawing tool can’t quite do it.

Source: Flexible Plan Investments Research

Hopefully you get the point. At the moment, as Allianz’ Chief Economic Advisor, Mohamed El-Erian said about the recent decline, stocks are just “building value.” And actively managed strategies let you take advantage of those values where others might fear to tread.

Look before you leap

Look before you leap! How many times have we all heard that admonishment? This is especially true in the summer when we spend so much time around a pool or lakeshore. We’ve all heard of the terrible downside that can occur by not checking things out in advance before we act.

Every time we have a few down days like we’ve had of late, I see the same play acted out. It begins with a first act where everything is rosy, the two characters in love. Then tragedy strikes and love is lost. Sometimes the second act brings reconciliation and other times the tragic loss just plays out.

Investors fall in love. They fall in love with stocks and asset classes and they fall in love with strategies. When a rapid downturn occurs, however, they can quickly fall out of love.

The usual reason for the parting that often happens thereafter is twofold. First, they forget why they bought what they did. It is one thing to be a buy-and-hold investor with a static portfolio who decides to give up on it. It is another to do that with an actively managed strategy that is constantly changing. You bought that strategy because it included a methodology that made all of the buy, sell, and hold decisions for you; presumably because you were not happy with the decisions you or someone else had made for you in the past. There should be a very good reason for a change.

A second reason is closely aligned with today’s first article – a failure to put the strategy performance in perspective. Was the strategy already suitability based so that it respected what you had expressed were your feelings about market declines? If so, unless your suitability profile has changed (just check with your advisor to do a quick update), the amount of loss sustained in a decline like the one we are experiencing is probably less than you expected and less than the indexes.

Only a handful of our suitability-based strategies fell more than the S&P 500 last week, and the ones that did tended to be more aggressive choices that utilized leverage. In fact, of the 127 strategies we track each week in putting together our weekly hotline, 113 outperformed the S&P 500 after fees.

When I say in this context to “look before you leap,” I mean that you need to consider a number of factors before leaping out of a strategy or even into a money market fund.

You need to consider the fact that you are probably already in strategies that are suitability based and reflect your temperament toward risk and have adjusted for it. Just as these don’t go up as fast as the riskier indexes, they don’t tend to go down as much either.

In another vein, if you have chosen an aggressive strategy, you need to look back at what the expected maximum los of the strategy was in its hypothetical research report. If the loss experienced was nowhere near that level, learn to give the strategy the room to work. Only by doing so can you expect to reach the outsized gains that are research demonstrated for the methodology.

Finally, in addition to checking out how YOU actually did with your strategy last week, instead of listening to what the media said the indexes did, check with your advisor and find out what the strategy was holding last week. With actively managed strategies, it changes all of the time.

For example, last week if you had checked on any of our FUSION balanced, moderate, or conservative accounts you would probably have not been surprised to find a lot of cash or bonds that would cushion any stock market volatility. But I bet you would have been surprised with some selective holdings of inverse equity index funds that seek to make money from the decline in stocks. Yet that was often the case.

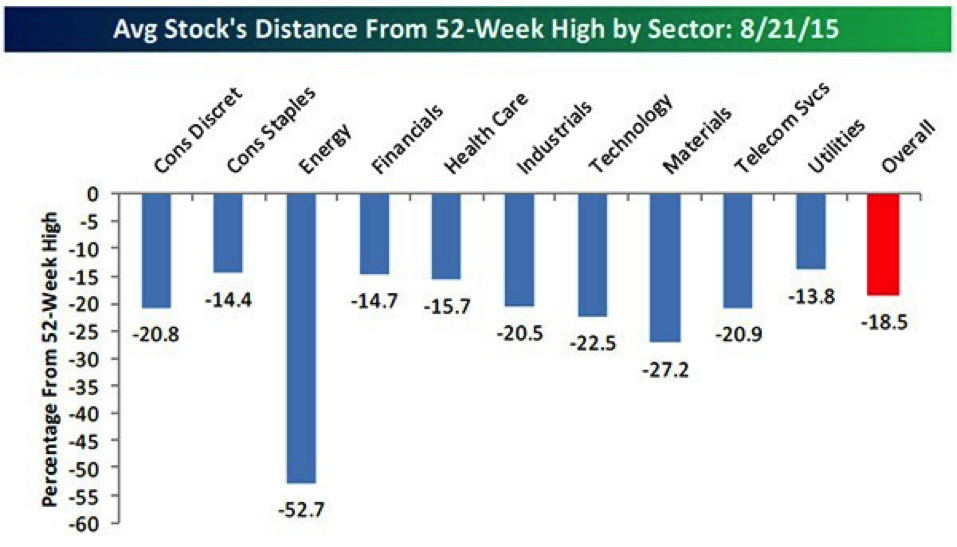

Similarly, with all ten of the S&P sectors falling almost 9% last week, you probably would have been pleasantly surprised to see all of our sector strategies with better weekly returns than the S&P 500.

Source: Bespoke Investment Group

And with gold being one of the top performers last week – up over 4% – it would probably be encouraging to see over 6% of each Fusion portfolio holding investments in the shiny metal.

A number of strategies were completely in cash for all or part of last week. Many had significant allocations to bonds and money market funds.

In other words, if you looked before you leaped, you’d find that your work had been done for you. And that’s what dynamically risk managed accounts are designed to do.

The advantage of a one-stop shop

I know from over 40 years in this business that despite the information I have given about how to put last week into perspective and how necessary it is to check on how your strategy actually fared during that volatile period, some of you are still going to want to change strategies.

When I created our Strategic Solutions platform at Trust Company of America in 1998, and then later added Jefferson National Monument Advisor, my goal was to make it easy for clients and advisors to seek out new strategies or to move to greener fields if they saw fit to do so.

Prior to those efforts, it was commonly the case that it was necessary for advisors to first research alternatives from many different sources. You had to find them and then do due diligence on the providers. If you were fortunate enough to find an alternative that you were comfortable with, the advisor and their client had to prepare and execute all of the new paperwork for both the new money manager and custodian. Then came the asset transfer process, and the time that took. It was all very frustrating and time consuming.

With Flexible Plan’s Strategic Solutions, and later our managed accounts with Schwab, Fidelity, and now Folio Institutional, you can easily change strategies with just an emailed instruction from your advisor. With more than 100 strategies from Managed Money Market to STF, not to mention seven suitability-based core strategies, there is something for everyone. We have trend-following strategies for most every type of asset class, as well as plenty of pattern recognition, mean reversion strategies. And at times like these, who can forget the alternative strategies, all of which can access gold.

Like retailers learned long ago, there is something special about one-stop shopping!

I hope you enjoyed this special, extended edition of In My Opinion this week. I think the recent events warranted it.

All the best,

Jerry

http://www.flexibleplan.com/market-hotline/disclosures