Our New Neutral outlook is generally supportive of equities: Low discount rates, recovering but muted inflation and a drawn-out business cycle argue for positive equity performance. However, full valuations and uneven growth suggest returns may be significantly lower than long-term averages. This means that capturing equity alpha will be critical for investors to meet their return objectives. Today, higher valuations are especially seen in small caps, which in our view are an important long-term strategic allocation for many investors. Fortunately, there are attractive ways to seek alpha through structural inefficiencies in markets, particularly by adding exposure to small cap stocks through the Russell 2000 futures index.

Recently, achieving alpha in equities has generally been difficult, and active managers on average have lagged market indexes. Many argue that the best alpha opportunities are in typically less efficient market segments such as small cap stocks. And yes, we agree that small cap appears to be an area that is ripe for capturing alpha.

However, there are many challenges to investing with a good small cap manager. Small cap is a capacity-constrained market segment, so the top performing managers can become victims of their own success. Some small cap strategies may grow in size and then close to new investors – this is good for the strategy, but disappointing for investors who want to allocate to the manager. Other small cap managers may continue to accept new assets and then compromise their investment mandate by either moving up the market cap spectrum or becoming more diversified to accommodate the larger asset base. In both instances, the manager may no longer be providing investors with the small cap exposure they expected.

Indexing is one viable solution to obtaining small cap exposure. But in an environment of lower expected returns, we believe investors should look beyond traditional approaches. The PIMCO StocksPLUS Small Strategy is an alternative that aims to preserve excess return potential without being limited by capacity constraints.

How it works

The market price of equity index futures contracts should be close to the fair value price, the theoretical price at which the futures contract should be trading to reflect the cash required to buy and hold every stock in the index. If the futures contract price is different from the fair value price, it may be an opportunity for what is known as index arbitrage, a strategy designed to profit from discrepancies between the prices of the stocks in an index and the price of a futures contract on that index. By buying either the stocks or the futures contract and selling the other, an investor can attempt to exploit market inefficiency for a profit. However, we believe the less liquid nature of small cap stocks makes investing in Russell 2000 index futures contracts particularly compelling.

Let’s say an investor wants to obtain short exposure to small cap stocks. This is theoretically straightforward, but in practice it is operationally difficult to obtain short positions, especially in small cap stocks. Why? Think about the mechanics of a short sale: The investor needs to find an available block of shares to borrow, sell and then buy back at (hopefully) a lower price. Finding the shares to borrow can be more difficult and costly in the less liquid small cap market, so many investors prefer the convenience of hedging using index futures. In other words, a common practice among investors looking to express short exposure – mostly long/short and macro hedge funds and institutional investors – is to short-sell Russell 2000 Index futures.

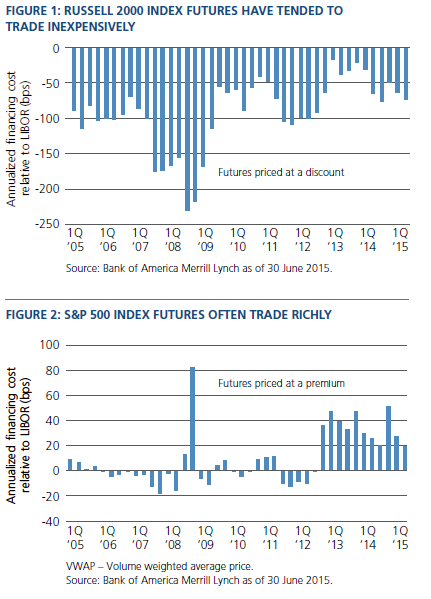

For the investor who wants long exposure to small caps, this may work out to be a structural advantage. Since often there is more demand to short-sell the Russell 2000 Index futures contract, it drives down the price, frequently resulting in a discount to fair value. Arbitrage investors would be unable to take advantage of this mispricing as it would require going long the futures and simultaneously shorting the 2,000 stocks in the index, typically not a feasible strategy. As a result, the Russell 2000 index futures have historically tended to trade “cheap” and thus can offer a potential return advantage to investors who maintain long positions. The “cheapness” in the Russell 2000 Index futures has tended to be persistent, and this type of discount is not typical for other futures contracts, such as those on the S&P 500, because pricing differentials can be more easily arbitraged away (see Figures 1 and 2).

Consider a portable alpha approach

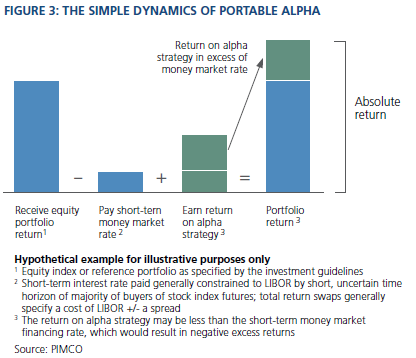

Equity investors can seek to capitalize on the structural inefficiencies of Russell 2000 index futures contracts through a portable alpha approach. Portable alpha strategies obtain equity exposure synthetically, typically via futures and/or swaps. Unlike a common stock portfolio, this method of gaining equity exposure requires a small up-front payment and money-market financing, allowing the manager to run an independent, complementary strategy designed to generate alpha in addition to receiving the returns of the equity exposure. In essence, if the returns of the alpha strategy exceed the money-market cost of the equity exposure plus management fees, then the strategy overall will outperform (Figure 3).

PIMCO has been managing portable alpha strategies for over 25 years, providing access to a variety of equity market segments while also seeking to deliver consistent outperformance over three- to five-year time horizons.

For investors seeking an allocation to small cap, we believe a portable alpha strategy is a compelling solution. The PIMCO StocksPLUS Small Strategy invests in Russell 2000 Index futures and backs those investments with an absolute-return-oriented bond portfolio, thereby offering investors the potential to capture alpha in their small cap allocations. The Russell 2000 futures market is large and liquid, as are the fixed income markets we typically invest in. So, we do not anticipate capacity constraints. In addition, since the Russell 2000 Index futures contract has historically traded lower than fair value, we are able to tap into an additional potential source of structural alpha.

The growing need for alpha

Our outlook for equities is constructive, but we expect future returns to be significantly lower than long-term averages. Given the challenges of capturing equity alpha – even in small caps – we believe investors may need to consider alternative approaches. PIMCO, as a broad-based solution provider, has developed a range of portable alpha and smart-beta-based strategies designed to help investors achieve excess returns in their core equity allocations.

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Mortgage and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and their value may fluctuate in response to the market’s perception of issuer creditworthiness; while generally supported by some form of government or private guarantee there is no assurance that private guarantors will meet their obligations. High-yield, lower-rated, securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Investing in securities of smaller companies tends to be more volatile and less liquid than securities of larger companies.Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the managers but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark or registered trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Pacific Investment Management Company LLC in the United States and throughout the world.

©2015, PIMCO.

© PIMCO