Well, maybe not literally. But figuratively-speaking, one can make the case.

And two very bright, young investment advisors have done just that.

The National Association of Active Investment Managers (NAAIM) announced last week that Charlie Bilello and Michael A. Gayed, both with Pension Partners, LLC, are the 2015 first-place winners of the NAAIM Wagner Award for Advances in Active Investment Management for their paper “Lumber: Worth Its Weight in Gold – Offense and Defense in Active Portfolio Management.”

In its seventh year, the NAAIM Wagner Award is designed to expand awareness of active investment management techniques and the results of active strategies. The award is named for Jerry Wagner, founder and president of Flexible Plan Investments, Ltd., a judge of the annual competition, and one of the driving forces behind the creation of NAAIM.

Of the winning paper, Greg Morris, the chairman of the award committee, writes “Charlie Bilello and Michael Gayed truly provide out-of-the-box thinking with this year’s winning paper. Focusing on non-traditional market signals using two well-known commodities, Bilello and Gayed demonstrate that risk-based active investment management has a big impact on performance.”

In the paper, Bilello and Gayed uncover a market anomaly in the relative movement of lumber to gold. They find that the relationship between these two commodities provides important information on economic growth and inflation expectations, which gradually diffuses with a lag to stock and bond markets. Lumber’s sensitivity to housing, a key source of domestic economic growth in the US, makes it a unique commodity as it pertains to macro fundamentals and risk-seeking behavior. On the opposite end of the spectrum is gold, which is distinctive in that it historically exhibits safe-haven properties during periods of heightened volatility and stock market stress.

The authors use lumber and gold as a signal to help answer the most critical question for active asset managers: when to take more risk (“play offense”) and when to take less risk (“play defense”) in an investment portfolio. They show that strategies using the signaling power of lumber and gold result in stronger absolute and risk-adjusted returns than a passive buy-and-hold index. Importantly, Bilello and Gayed argue that being defensive and protecting capital during periods of higher volatility in equities was a critical factor in generating outperformance.

USA Today’s business section picked up the story of the winning paper, and did a nice job of putting its conclusions in simple terms:

“In a nutshell: When lumber outperforms gold over the previous 13 weeks, you should be more aggressive in the stock market, and when gold outperforms, you should be more defensive.

Why lumber? Lumber prices are a good indicator of the housing market—which, in turn, is a good indicator of the economy as a whole. And unlike most housing indicators, lumber isn't lagged by weeks or months—lumber futures prices are available throughout the trading day. And while home construction is just one part of overall economic growth, it has an enormous ripple effect.

Gold, on the other hand, is a good measure of fear. People buy gold when they think bad things will happen. ‘In multiple cycles, when lumber outperforms gold, the stock market tends to be less volatile,’ Bilello says. ‘The economy is improving and in an expansionary phase. And it's the opposite when lumber is underperforming.’”

What is lumber telling us now? "From the end of last year, lumber has been underperforming gold," Bilello and Gayed say. "It doesn't mean that stocks have to go down—it simply means that there is a higher probability of volatility rising."

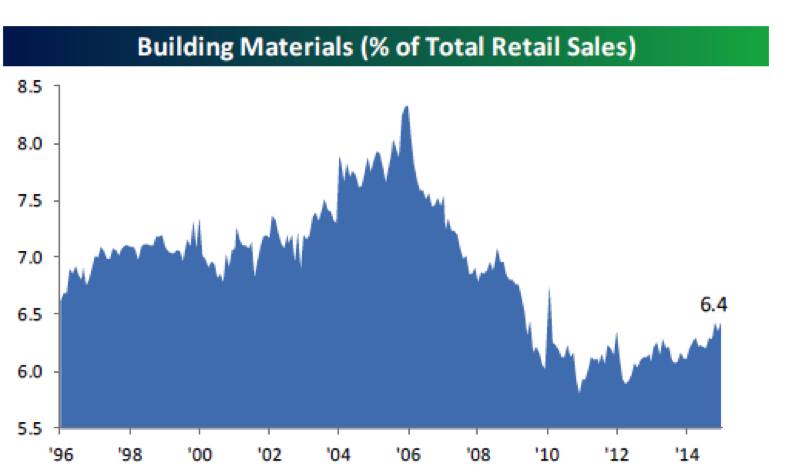

Speaking of the ripple effect of the housing market, it does not seem coincidental that US GDP has been stuck in a low-growth phase (predicted by Congressional Budget Office projections and others to remain so for several years). Building material sales remain well below pre-recession levels as a percentage of total retail sales:

Source: Bespoke Investment Group

Last week, the Federal Reserve issued its “Beige Book,” which reports anecdotal and empirical evidence from the 12 Fed regional banks on how the economy is performing in their specific areas from mid-February through March. Not surprisingly, “weather conditions” were cited some 71 times, as many of the regions were still coping with the aftermath of a brutal winter.

The overall regional assessments of economic progress ranged from “modest to moderate to steady,” as “the economy continued to expand across most regions.” Demand for manufactured products was “mixed … with weakening activity attributed in part to the strong dollar, falling oil prices, and abnormal seasonal weather effects.” Business service firms saw rising activity, especially for high-tech services. Residential real estate activity showed signs of improvement, although there was “slowing in housing starts due to the harsh weather.”

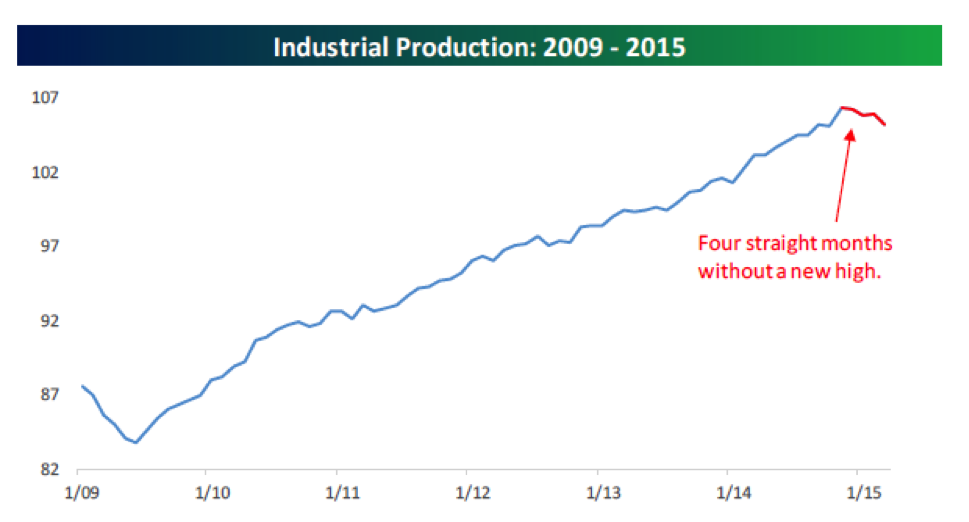

The jury is still out on whether the 1st quarter relative weakness in many economic reports will quickly be forgotten, as was the case last year. If you recall, Q1 2014 GDP actually put in a negative number, only to be followed by relatively strong figures for the rest of the year. However, many analysts are watching the current performance of the economy with some caution, despite the continued strength in equity markets. Industrial production numbers are one area of concern, with three declines in the last four months and the largest one-month decline since 2009.

If Mr. Dilello and Mr. Gayed are correct, and markets may face a period of heightened volatility, it is comforting to know that the quantitative tools of active management are at the helm, and not human emotion. The end of last week, according to many of the headlines, saw predictions for the bottom dropping out of global markets. But on Monday, at least as of the time of this writing, it was yet another quick and impressive recovery for equities. It would seem prudent to let the algorithms, indicators, and models deal with that type of whipsaw up-and-down action, which has been in force for most of this year’s tight S&P 500 trading range.