Last week we focused on investors’ waiting game with the Federal Reserve. Would their policy statement following last Wednesday’s meeting, like last month’s Groundhog Day sighting, suggest more weeks of winter in the form of rising interest rates?

The result of the wait was, contrary to many market “experts,” very dovish. While the word “patient” was removed—in fact the entire sentence was removed—the statement made it clear that a rate hike was not imminent—April was out and, while June was still in play, a change that soon seems doubtful. Why?

-

Let’s look at what the Fed said: Inflation must look like it is moving higher toward the Fed’s 2% target rate before a rate increase is likely. But the rate of inflation is moving down not up. Two weeks ago the Producer Price Index actually registered a decline in wholesale prices. Before that, the Consumer Price Index also fell. Last week, in both the Philly and New York Fed Manufacturing Report, the few companies reporting an increase in the Prices Paid component declined in number yet again.

-

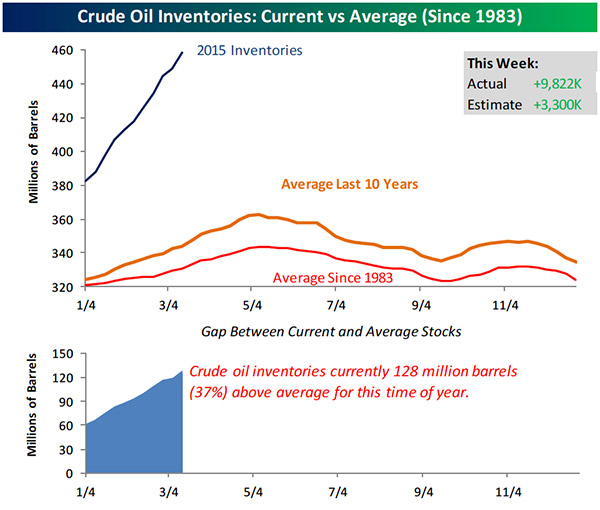

Certainly one reason why prices fell was the sharp decline we have been experiencing in oil prices. Energy costs are an important part of the inflation calculation and the prices continue to fall. Last week, the latest market low point of a few weeks ago was broken to the downside yet again. Oil inventories continue to build to historic levels. Here’s market researcher Bespoke Investment Group’s recent report:

For only the sixth time since 1983, US crude oil inventories have risen for ten straight weeks. For those keeping track, there has only been one prior period where stockpiles increased for 11 straight weeks (September – December 2004). In this week’s report from the Department of Energy, crude oil stockpiles for the latest week increased by 9.822 million barrels, which was nearly three times the expectation of 3.3 million barrels. Over the last ten weeks that crude oil inventories have risen, the total increase in stockpiles has been 76.3 million barrels, which is a record for any 10-week period, and 75% more than the prior record 10-week build of 43.9 million from 2001.

Of course, a picture is worth a thousand words and this one bears repeating:

Source: Bespoke Investment Group

One would think that this would mean that producers would slow down or stop producing. Well, no signs of that as yet. In fact, a Saudi Arabia spokesman announced today that there would be no change in their production levels, despite the unprecedented overhead in inventory. Oil prices are likely to stay low for longer than most expect ... and inflation rates with them

-

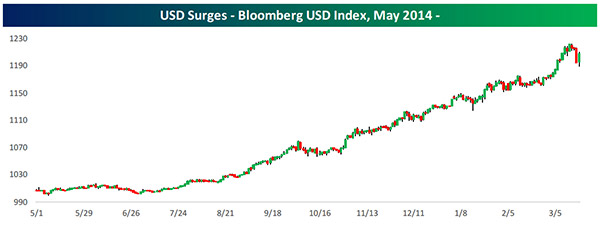

Of course, a reason many have suggested for oil’s plunge is the rising Dollar. Its performance has been practically off the chart now for more than six months. The effect of this is to make imports cheaper (putting further downward pressure on inflation rates) and our exports more expensive (resulting in lower economic and, perhaps, earnings performance for US-based international companies). The result of both of these outcomes is contrary to the Fed’s twin mandate of moderate inflation and growing employment.

Ironically, the cure for a rising Dollar is lower interest rates, not higher. When interest rates in a nation are higher than those of its competitors, it attracts investments in that nation’s currency. If money supply growth is flat or moderate, the supply of the currency is less that the demand and the currency value is driven higher. That is precisely what is happening here with our Dollar.

Source: Bespoke Investment Group

-

The Fed, though, is caught between a rock and a hard price. Currently our rates, as low as they are, are higher than our competitors. And that is not likely to change for quite some time. Both Japan and the European Union have adopted the Fed’s Quantitative Easing approach precisely to drive rates in their countries lower AND, importantly, to make their currency cheaper than ours and their other competitors. If the Fed raises rates, it will exacerbate the situation, and the outcomes the Fed seeks to avoid re its mandates become even more likely.

-

Finally, it is very difficult for the Fed to raise rates at the same time that economic reports are suggesting a weaker economy. As we pointed out last week, the Fed has never raised interest rates in the past when retail sales fell for three months in a row.

Among the economic reports last week, only two out of ten exceeded expectations while eight failed. This disproportionate result has been the case for most of this year. Many say this is because of weather, but the economists setting the expectations on the diverse economic reports that have underachieved were all aware of the brutal weather in much of the country BEFORE they set the level of expectations.

It seems that we should look forward to a longer-than-expected period of lower-than-targeted inflation rates and oil prices, together with a rising Dollar and weak economic reports. What’s this all mean for investors?

With comparative rates of returns favoring stocks versus bonds, equities are likely to continue to shine. Bonds are likely not to be negatively impacted by a stable interest rate environment contrasted with a rising rate atmosphere. Importantly, there is still time to lock in low mortgage rates and seek out those 0% credit card deals.

Unfortunately for both the stock and bond markets, however, volatility is likely to increase. There will be times when headlines will run counter to the storyline advanced above. Since both stocks and bonds are more extended to the upside than the downside, the reaction is going to be violent on those days. We’ve already seen the increase in volatility this year. In the past seven trading days, for example, the S&P has flip-flopped its direction each day!

Of course, this hotline is a part of our “In My Opinion” series. It represents just my opinion and is subject to change. Rather than relying on it or those of the talking heads on TV, why not do what I do with my own investments—utilize disciplined, computerized trading strategies that have been tested over years in a wide range of economic environments. These dynamic, actively managed methodologies can follow a given direction for quite some time (like our now multi-year stock market bullishness) but then change direction sharply if conditions warrant it.

One final thought on the Fed. The Federal Reserve has many tools in its tool bag. Raising and lowering interest rates are two of them, and no one knew that QE was also lurking in their bag of tricks before they pulled it out not once, but three times. They have many options, some that can be anticipated, some that cannot.

One that has not been mentioned much but which may be already in play is the Fed’s ability to talk rates up or down with its pronouncements. Without them raising or lowering the Fed funds rate a single basis point, they can cause the interest rates to rise or fall simply by what they say. It’s my guess that that is all they will be doing until fall at the earliest, but as I said last week … we will just have to wait and see.

All the best,

Jerry