I spent the last two weeks on a Caribbean island (as I always say: Timing is everything!). We rented a house and had lots of visitors from “Up North” (my wife will be there a month and during that time we will have had seventeen people staying in the house!).

With the enormous amount of snow experienced in the Northeast and the abnormally low temperatures that stretched from there throughout the Midwest, all of our visitors were talking about the winter weather during the last two years in our neck of the woods.

No surprise there, right? But, what I was surprised by was the fact that almost every waking hour saw The Weather Channel exclusively displayed on the TV screen in the family room of the vacation rental.

I know some older family members and acquaintances that have turned TWC into a 24/7 permanent image in their TV viewing rooms. But at our vacation spot, I observed this latest TWC fixation across all age ranges. And this was with outside temperatures in the mid-80s, an infinity pool just outside the doorway, and azure blue surf beckoning just 30 feet away across a pristine white sand beach!

Of course, I could not help but compare this TWC fascination of our visitors to the CNBC obsession many investors and their financial advisors have demonstrated over the years. During market hours, I have often observed this phenomenon on home and office visits. When I ask, “What actionable ideas do you get from the station?”, I usually get a response about wanting to keep up on what’s happening.

Now, of course, there is nothing wrong with that answer. I love to steal a look at the screen to get a quick update on the direction of the markets each day. I do, however, worry about those viewers who actually listen in for a while—be it for a short or long period of time.

I can understand the “train wreck” phenomenon, the tendency to be a gawker when passing by a car accident, for example. Like watching the abnormal weather of late, the tendency of people to stop and look is hard to avoid—whether it’s an auto or a market crash.

But there is so much that is wrong about most people exposing themselves to a steady diet of financial news shows. It tends to make them much more short-term oriented, and a constant air of crisis is continually instilled. Both lead to investment behavior that preys upon our predisposition as humans to emotionally overreact.

Worst still, there is a tendency to focus on the behavior of the usual gang of pre-packaged, general market indexes—you know, the Dow, S&P, NASDAQ and Russell, etc. While these can definitely tell you something about the equity market environment, on the financial news shows they tend, instead, to be offered as THE standard against which to measure investment performance.

While I have often commented on the inappropriateness of this, I must say I have often felt like I was the lone voice in the financial wilderness. It seems so obvious to me. How can one judge investment success of a portfolio meant to reflect the suitability of each individual client by comparing it to the performance of a mass-marketed index, like the S&P 500, that has twice experienced 50% losses in the short lifetime of the current century? Yet the financial media does this every day, week, month, and, especially, quarter, with no disclaimer of inappropriateness.

Thus, it was with great pleasure that I noticed this recent headline in the periodical for Registered Investment Advisors, the Investment News

When underperforming the S&P 500 is a good thing

Matching the index last year would have involved too much risk

Read full article at Investment News

The article written in Jeff Benjamin’s Investment View column acknowledged that “Blame the ever-expanding financial media or the increased awareness among investors, but there is no getting around the reality that clients have become programmed to dwell on the performance of a few high-profile benchmarks.”

The problem with this, he explained, was that last year’s 13%-plus S&P 500 performance caused many clients to question why their accounts had lagged the index. Yet, the “(f)act is, a truly diversified investment portfolio should have returned less than 5% in 2014. It was that kind of year. Any adviser who generated returns close to the S&P was taking on way too much risk, and should probably be fired.”

Jeff pointed out that while the S&P 500 had an above-average year, foreign stocks and commodities posted negative returns, and broader-based domestic stock indexes that are also required in a diversified portfolio experienced sub-par years. As Ed Butowsky, managing partner at Chapwood Capital Investment Management was quoted in the article: “Sure, the S&P 500 had a good 2014, and if you had all or most of your money invested in [that index], you did, too. But what were you doing with most of your money in a single index?”

Diversified portfolios, whether created from asset classes or actively managed strategies, or both, as in our Fusion service, rarely outperform the best performing index, whether it’s the S&P 500 or some other top performer in another given year. Diversification by definition can only achieve average returns. Diversification’s advantage, easily ignored in a bull market, is that it delivers below-average risk or volatility.

So, how do you measure performance? We do it by comparing our performance to the estimate of each client’s likely performance. We make these estimates in advance, before they invest. Our clients’ quarterly OnTarget Monitors demonstrate whether or not their customized portfolios are “OnTarget” or within the expected glide path to their investment goal.

As Jeff said, one of the big reasons diversified portfolios underperformed the domestic-based S&P 500 was the losing performance posted by international funds—both the developed and emerging market versions . At the beginning of this year, a lot of commentators were expecting the US stock market indexes, buoyed by a rising dollar, to again outperform their international brethren this year.

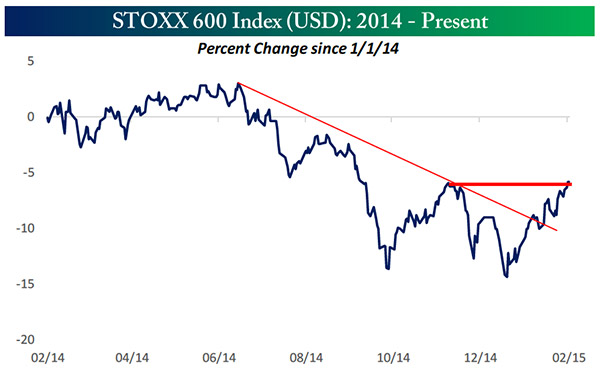

Yet a quick look at the financial markets demonstrates why only holding domestic stock-based investments can be as damaging to a portfolio as investing solely in the foreign variety would have been last year. Although the domestic stock market has managed to eke out new highs, it has done so without much fervor and has been flat to down most of this year. In contrast, as the chart demonstrates, foreign stocks have soared:

Source: Bespoke Investment Group

Just as market “experts” expected the reverse price action, they also said that the companies in the S&P 500 that would likely earn the most in the quarter and thus lead the charge forward were those that derived their revenue from right here in the US. Yet, in the 4th quarter earnings reporting season just completed last week, the S&P 500 companies with a majority of foreign revenue were the ones that, on average, best beat estimates.

Speaking of earnings season, it was encouraging to the bullish case that we have been making for over two years now that we saw so many companies beat the pre-reporting earnings estimates of the analysts. In fact, this quarter’s results placed it in the top five quarters out of the last fifteen. More than 60% of firms reporting beat analyst estimates.

As I mentioned right before earnings season commenced, the very fact that most companies’ earnings estimates had been downgraded by analysts before the reports began virtually assured that we were going to have more earnings surprises to the upside than to the downside. Revenue reports similarly did better than expected.

Most of the market indexes are in mildly overbought territory (indicating they may have gone up too far too fast in the last three weeks, during which the S&P 500 registered gains and the last nine trading days when the NASDAQ did the same). As a result, it would not be surprising to see a pause here, be it a decline or sideways action in the short term.

However, the major trend remains firmly in an uptrend and all of our intermediate- and long-term tactical indicators (read market timing measures) remain positive. Until the trend conclusively reverses, use any weakness in stocks to make greater use of our equity-based, actively managed strategies. Actively managed strategies allow you to participate in bull markets while having a pre-established defensive game plan should the bull market end.

At the same time, take the weather forecasts of TWC and the voices on CNBC, as well as the opinions of this commentator, with a grain of salt, which I found on my return to be on our roadways in abundance. And a tip of the hat (and newly donned scarf and gloves) to Mr. Benjamin at the Investment News. Finally, at least one financial media person gets it …

All the best,

Jerry