In honor of Father’s Day this past Sunday, I wanted to reminisce on an activity I enjoyed with my father.

My father liked all sports, and was a pretty fair college tennis player, but his real passion was the great outdoors: camping, fishing, lake swimming, and canoeing. Our family enjoyed our camping trips all over the US, if not the cramped and very long rides in the old station wagon.

My father also enjoyed hiking, occasionally having us tackle a somewhat challenging mountain trail. On several of those hikes, we experienced a phenomenon known to serious mountaineers and amateurs alike, known as encountering a “false summit.” From the mighty Himalayas to the modest peaks of Pennsylvania’s Poconos, false summits can be found all over the world. The experience has been described as you think it might be—approaching for a lengthy amount of time what appears to the hiker or climber to be the summit of the mountain, only to find the mountain continues upward. Some mountains, particularly in the Northwest US, are notorious for multiple false summits.

This feels a little bit like the climb US equity markets have been on the past few years. The financial media and many market “pros” have declared a market top has been in sight multiple times, yet indices keep scaling to new heights. It remains a hot topic of discussion just about every week, as some new concern hits the markets and a potential market top is declared. But markets keep on scrambling up the “wall of worry” and it proves to be yet another false summit.

The lack of significant market pullbacks has been rather remarkable over this bull run, especially since new all-time highs were set in the S&P 500.

According to analysis by Raymond James’ strategist Jeffrey Saut, this move higher has been accompanied by some choppy action, but hardly a full-blown correction. The S&P broke out to new highs in May 2013, but that breakout was followed by a 6.7% pullback into late June. New highs in August of 2013 were also followed by a 4.8% pullback, and that sequence of new highs and a 4.8% retreat repeated again in September and October 2013. The pattern emerged once more in January of 2014, with more new highs and a subsequent 6.2% decline into the first week of February.

Saut wonders if we will finally see in the next few months “the kind of trading top that will lead to the 10%-12% pullback history calls for some time this year.”

Last week’s market action did not calm the talk of a potential market top, with the major indices putting in their poorest performance in several weeks. With the minor rebound on Friday (June 13), the weekly results in fact were rather tepid: the S&P was down 0.7%, the Dow was off 0.9%, and the NASDAQ Composite shed 0.2%.

Ostensibly the worsening of the situation in Iraq and a cut in global growth estimates by the World Bank were the impetus for the selling pressure early in the week, but consolidation was not unexpected after overbought readings on the market toward the end of the preceding week.

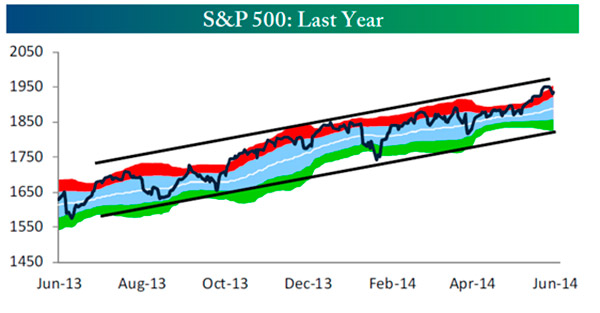

Bespoke Investment Group developed a chart that indicates both the tight range of the market’s uptrend over the past year and the fairly consistent, though minor, pullbacks from “overbought” red conditions. Bespoke notes, “whenever things get as overheated and extended as they had been, we typically see at least a short-term pause. This doesn’t mean we’re due for a big sell-off or longer-term correction, but rather a pullback within the long-term uptrend channel that the market has been in for more than a year.”

Source: Bespoke Investment Group

What has been surprising to many market observers is the lack of volatility during a seasonal period—both as measured by the calendar and by the presidential cycle—when volatility should be ramping up. Despite Bespoke’s relatively upbeat outlook, the calls for that 10% correction cited by Mr. Saut are not uncommon among analysts for 2014.

While we think speculation on the market’s next move can be interesting and, at times, instructive, it hardly qualifies as a strategy. This is why active management, as practiced by Flexible Plan Investments, is all about eliminating emotion, market bias, and the confusing din of expert predictions. Active management’s reliance on model-based decision making facilitates that process.

Those models can cover a wide range of inputs and might include analysis of econometric data, market price trends and technicals, seasonality factors, sentiment, cycle composites, volume indicators, and a whole host of other algorithm-based analytics. Utilizing unemotional strategies based on such factors over the full duration of market cycles certainly makes more sense to us than blindly reacting to the latest headlines.

However, falling into that “interesting to note” camp is the fact that the S&P 500 recently reached 1955.6 on an intraday level, just below Bloomberg’s tally of the average prediction for full-year 2014 by twenty major Street analysts—which was at the 1968.5 level (with a range from 1850 to 2185).

Even if that average prediction were correct (an iffy proposition usually), does that mean a period of further gains followed by a major correction this fall, stalling and stagnating at current levels through the end of the year, or a pullback over the summer followed by the now-traditional year-end rally?

Logic dictates that an intermediate market top has to be reached at some point, but the question is when? While there is no shortage of those calling for the end of the bull market, are they just falling prey again to the phenomena of “false summits”? Only time will tell—and the only real certainty is the need to have strategies that are risk managed and well prepared for any market eventuality.

Have a great week.

David