The Crimean Conflict Has Affected Commodities Markets, Just Not Where You’d Expect

Since the end of February, when the Crimean crisis started to escalate, grain prices have responded to nearly every up and down of the crisis. Wheat is up 21%, and corn is up 10%.

We believe investors looking to take a view on the future price of wheat or corn should do so through the options market. In this case, we think being long puts on wheat is an attractive way to implement our short wheat view.

This article originally appeared on institutionalinvestor.com on 19 May 2014.

Since the end of February, trading in the commodities markets appears to be largely unaffected by the Crimean crisis – at least at first glance. Oil prices are 1% lower, based on brent crude oil futures, despite Russia being the largest oil producer in the world. Even in European natural gas, where roughly 30% of supplies come from Russia, prices have actually moved substantially lower despite some initial spikes in early March as warm weather sapped demand. We see several potential reasons for this, but the bigger picture is that commodities traders haven’t been very concerned about supply disruptions from Russia. However, the same is not true for traders in commodities that depend on Ukraine for a large share of supply. Those commodities are wheat and corn.Â

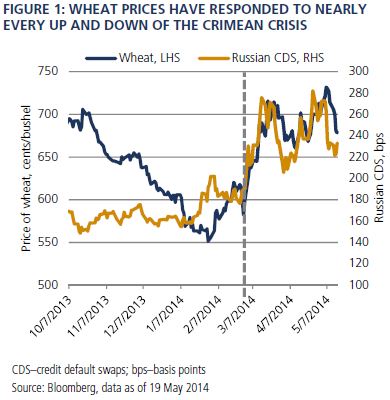

The link between Russian credit risk and wheat pricesÂ

If you want an outside gauge of whether the market is more or less concerned about events in Russia and Ukraine, you can look at wheat prices. Ukraine is a major supplier of grains, particularly wheat and corn: The country represents roughly 7% of global wheat exports and 17% of global corn exports, on average. Since the end of February, when the Crimean crisis started to escalate, grain prices have responded to nearly every up and down of the crisis (Figure 1). Wheat is up 21%, and corn is up 10%.

Â

What this means for future pricesÂ

Absent the events in Crimea, we see the wheat and corn markets as well supplied globally, and we see little evidence that this will change over the coming several months. High grain prices over the past year have led to large crops and a rebuilding of global inventories. There is no doubt that this year’s winter wheat crop in the U.S. suffered some damage as it came out of winter dormancy into an excessively hot and dry spring across the Southern Plains. However, crop conditions in Europe are much more normal. In corn, the current pace of planting is relatively slow, but we expect a large crop and limited downside to yields given the developing El Niño weather pattern. (Typically El Niño years are associated with cooler, wetter summers, and this reduces the tail risk of a materially smaller corn crop like last year’s.)Â

The combined impact of current conditions in the U.S. and uncertainty in the Black Sea region has resulted in a large premium being placed on U.S. grain prices. For example, compare the current FOB market (free-on-board, that is, the cash offer at port for global wheat). Australian offers for high-grade wheat are approximately US$60 per metric ton, or 20% cheaper than the same grade of U.S. wheat. This shows how uncompetitive the U.S. offer has become to global buyers. We expect that over the coming months the risk premium embedded in U.S., as well as global, grain prices is likely to recede as the size of the U.S. wheat and corn crops becomes more certain.Â

Investment implicationsÂ

Our forecast for falling grain prices over the next few months assumes that the Russia-Ukraine situation doesn’t escalate further. How do we reflect this fundamental view in our portfolios? Implied volatility from the wheat and corn options market is below 30%, which is well below the average of the past five or 10 years. Since the end of February, volatility has risen by roughly 3 percentage points, far less than the impact on the outright price of the commodity.Â

Therefore, we believe that investors looking to take a view on the future price of wheat or corn should do so through the options market. In this case, we think that being long puts on wheat is an attractive way to implement our short wheat view.Â

© PIMCO