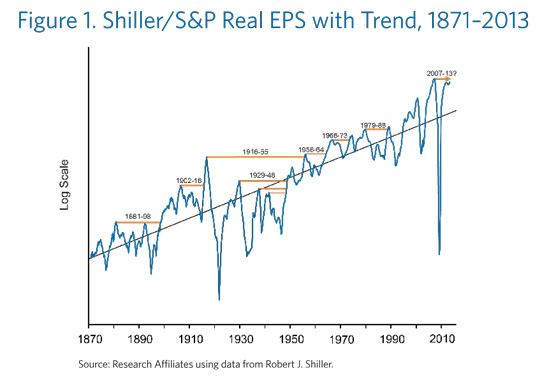

Profits are dangerously elevated by all reasonable measures. S&P 500 Index real earnings per share are far above their long-term historical trend. Industry profit margins are at or near all-time highs. Corporate profits, both as a percentage of GDP and relative to labor income, are at or near record levels. The dramatic rise in income inequality is a direct consequence of this spectacular reallocation of income to capital and away from labor.

For nearly a quarter century, we have experienced profits growing at a faster clip than GDP. Extrapolating this trend into the future is speculative at best. Equilibrium real growth in earnings per share cannot exceed real growth in per capita GDP, real growth in wages, and real productivity growth, on a long-term basis, without violating our sense of social fairness: More rapid growth in profits than GDP means a rising share of income to capital. Capital’s share cannot rise in perpetuity; social and political forces, if not economic developments, will cause it—sooner or later— to revert to a more usual level.

Many of today’s investors uncritically assume that the conditions they have known over the course of their professional careers must be normal. The idea that we may soon experience a multi-decade period of zero or negative growth in real earnings per share, taking the level of profits down to a lower share of national income, seems preposterous. Yet economic history has seen many examples of such a turn, including the 1880–1890s, the World Wars, the 1930s, and the 1970–1980s. In fact, almost every decade except the 1990s and 2000s saw a protracted profits slump. Some declines in profitability lasted most of a decade; others, longer!

The profits bubble of 2007, likely to be just barely exceeded in 2013 in real EPS terms, is above trend by a wider margin than all previous profits booms except the one that ended in 1916 (see Figure1). While it would be foolish to draw too much attention to the 39-year span before that peak was exceeded in 1955, or the two World Wars and the Great Depression that intervened, it would be equally unwise to lightly brush aside the aftermath of the 1916 crest.

The macroeconomic cause of today’s profits bubble can be understood as a quarter century of politically facilitated globalization. During the 50 years following WWII, we lived in an open global developed economy containing less than one billion people in Europe, North America, Australia, Japan, Korea, Taiwan, and a handful of others. Some countries were growing faster, some slower, but the technological level and population growth rates were not very different across the predominant countries within this relatively open global economy. The shares of income to labor and capital varied cyclically but tended to revert toward long-term averages.

Beginning in the 1990s, we experienced a seismic shift in our global political economy. Approximately three billion people began to join this open global economy: about one billion each in China and India and another billion or so in Russia, Eastern Europe, South America, and Southeast Asia. Average wages, level of technology, and amount of accumulated capital in the countries of the aspiring three billion lagged far behind those enjoyed by the one billion in the developed world. Imitation and appropriation is far easier than innovation and invention, so catching up has been rapid for those nations willing to make even modest concessions to the aspirations of their citizenry. For the past quarter century, the capital and technology accumulated by the old equilibrium advanced global economy has been suddenly shared across a labor force and populace that quadrupled.

This tectonic shift in our global political economy produced some winners and some losers. Incomes of many of the three billion newly joined rose quickly. Global poverty rates have plummeted. Meanwhile, wages in the old advanced economy countries stalled at least partly in response to competition from the lower wages welcomed by workers in developing countries.

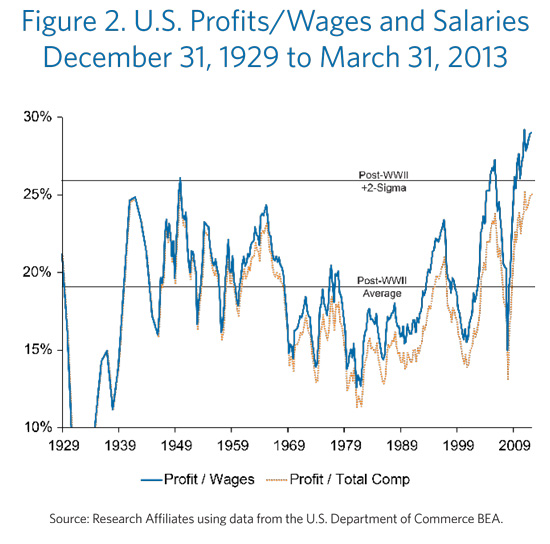

Profits grew to a much larger share of output and an unprecedented percentage of wages and salaries (seeFigure 2). To be sure, if we adjust wages to include the value of benefit programs and entitlements, we aren’t quite at all-time highs in profits-to-total compensation ratios. But, even here, we’re darned close to unprecedented records. In both cases, the five- and ten-year averages are at new highs. These longer-term trends are fueling popular unrest.

This period of globalization and the inflation of our profits bubble has been facilitated in part by a corporate capture of government policy, inhibiting competition, depressing investment, and promoting rent seeking. Rent seeking may be more extreme within our very own financial industry than in any other. TARP and QE are just the most recent and largest examples of government intervention to benefit corporate interests. For several decades, under governments led bybothparties, the close nexus between Wall Street and Washington has facilitated an economic policy that favors politically savvy corporations and too-big-to-fail megabanks. Our policymakers have too often mistaken what is in the best interest of their elite peer group (and, surely by sheer coincidence, some of their largest campaign contributors) as in the best interest of the broader society. The result has been decades of stagnation in wages, high taxes on labor income, subsidies for debt and consumption, underinvestment, and soaring corporate profits.

Now, we applaud business success and the resulting profits, particularly when profits flow from inventing new processes, products, and services and providing value to customers. We eschew government meddling in the economy especially when the results favor the politically connected and thwart fair competition. Because globalization and corporatist economic policies seem to have unfairly tilted the scales against lower skilled workers in developed countries, we sympathize with the growing political pressure to subsidize the creation of low skill jobs, to improve the skills and wages of the less proficient, and provide a living wage to the working poor.

We cannot predict the quarter or year when profits will peak. We can predict the catalyst. The share of corporate profits is a political choice. The present share of income going to capital seems increasingly intolerable. Populism is rising throughout the developed world and will likely lead to political change. Today we have libertarians joining progressives in rhetorically attacking big banks and advocating redistribution through raising minimum wages and subsidizing low wage jobs. Expect corporations’ labor, interest, and tax expenses to rise faster than sales over the next couple of decades and profits to grow much more slowly, or even decline, in real terms.

KEY POINTS

1.Corporate profits are at or near an all-time high relative to both GDP and wages and salaries.

2.Globalization facilitated by a corporatist economic policy is the cause of the upward surge in profits. The resulting degree of income inequality seems socially intolerable.

3.Rising populism will likely lead to changes in government policy. Expect real earnings per share to grow much more slowly, or even decline, over the next couple of decades.

© Research Affiliates

www.researchaffiliates.com

© Research Affiliates

Read more commentaries by Research Affiliates