The Risk Tolerance Paradox

…And What You Can Do About It

Overview

The risk tolerance level many investors expect to achieve over the long-term rarely equals the same tolerance investors actually experience over shorter periods. This paper provides a brief introduction to this paradox, explores the main reason we think it exists, and introduces a risk management strategy that seeks to solve the problem.

As more “low volatility” and portfolio risk management strategies hit the marketplace, it will be imperative that advisors and investors explore each strategy to uncover how risk is actually being addressed. Identifying those techniques that address both diversifiable and systematic risk is likely to provide better overall results for investors.

Identifying Your True Risk Tolerance

In an attempt to simplify the complexities of managing portfolio risk, the discovery of an investor’s risk tolerance level has likely been a straightforward process. It may have begun with a series of questions about his/her time horizon, investment prowess, financial goals, and overall level of concern about the stock market; and it likely ended with a check mark placed in a box labeled “conservative,” “moderate,” or “aggressive,” branding the investor as such. Assets would have then been allocated among various asset classes that have collectively exhibited a historical level of risk (e.g., standard deviation, beta) that matched the investor’s pre-determined profile.

There’s a Name for That

While the motive behind the risk profile check box is good—to assist investors in identifying a comfortable level of portfolio risk—the paradox many investors face is this: the risk tolerance level investors expect to achieve over the long-term rarely equals the risk level investors actually experience over the short-term. In other words, a conservative portfolio may act as such over the course of 20 or 30 years; however, during shorter time periods, that same conservative portfolio may exhibit volatility levels more in line with an aggressive (or more conservative) portfolio. This paradox is rooted in the statistical term “heteroscedasticity,” which simply means the level of volatility cannot be predicted over any period of time.

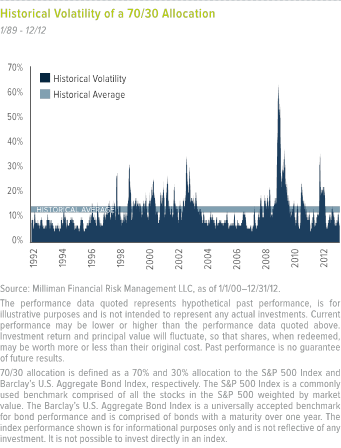

To illustrate this concept, let’s take a look at the portfolio of a typical moderate investor, consisting of 70% stocks (represented by the S&P 500 Index) and 30% bonds (represented by the Barclay’s U.S. Aggregate Bond Index). The average historical volatility of stocks is around 18%, and the average historical volatility of bonds is around 4%. Therefore, a moderate investor should expect to realize a volatility level of 13% over time.

During shorter periods, however, it is rare that a moderate investor actually experiences 13% volatility. In fact, from 1989 to 2012, on a 21-day basis, a typical moderate investor spent over 90% of his/her time at least one percent outside the historical average (more than 14% or less than 12%). In other words, collectively, a typical moderate investor realized either too much or too little risk relative to his/her predetermined risk tolerance a total of 21 of the past 23 years (see chart below).

Two Types of Risk

The reason for this discrepancy lies in asset allocation’s ability to successfully manage portfolio risk.

There are multiple risks that can negatively affect portfolio value. When categorized, they generally fall into one of two buckets; 1) diversifiable risk, and 2) systematic risk.

Understanding this typecast is a cornerstone to truly reducing portfolio uncertainty.

Diversifiable Risk

Diversifiable risk is inherent within a specific company or industry. An employee strike at a coal mine, a detrimental headline, or an investment rating downgrade are a few examples of diversifiable risks. This type can generally be diversified away through appropriate asset allocation.

Systematic Risk

Systematic risk, on the other hand, is inherent to the entire market or market segment. Examples of systematic risk include global economic crisis, large interest rate movements, recessions, and wars, to name a few. Systematic risk events have a low probability of occurrence, but they can have a significant negative impact on portfolio value if they occur. This is because systematic risk events affect the whole “system.”

Systematic risk is considered to be un-diversifiable, and is responsible for some of the largest upswings in portfolio volatility on record (e.g., ’73–’74, ’00–’02, ’08–’09). For example, during the recent financial crisis, nearly every major asset class declined in lockstep (save U.S. corporate bonds). Many people saw their retirement nest eggs lose significant value in a short period of time. This is simply because these types of risk events cannot be diversified away.

The realization of this has caused many investors and advisors to evaluate conventional wisdom, sparking a sea change in the way they manage portfolio risk and save for retirement.

Conclusion

Historically, the common answer to overcoming portfolio volatility and large portfolio losses has been to, “Stay invested in the market; continue saving and investing in your portfolio across all market conditions; when the market goes down, ride out the storm—eventually growth will return and the damage to your portfolio will be repaired.”

We believe this maxim was completely accurate for individuals in their twenties and thirties. However, as millions of “accumulating” investors approach retirement, and become “decumulating” investors, this approach simply may not work. When an individual must use a portfolio to meet current income needs, it is not always possible to “ride out the storm.”

As the investment landscape increasingly focuses on risk management, it is imperative that financial advisors and their clients perform due diligence on each method. It is possible that risk management strategies that rely solely on asset allocation may still be exposed to periods of systematic risk, at which point asset allocation may be rendered ineffective.

We believe identifying those strategies that address both diversifiable and systematic risk is likely to provide better overall results for investors.

About Milliman Financial Risk Management LLC

Milliman Financial Risk Management LLC is a global leader in financial risk management to the retirement savings industry. Established in 1998, the practice includes over 100 professionals operating from three trading platforms around the world (Chicago, London, and Sydney), and advises over $80 billion in assets (as of September 30, 2013).

Mutual Funds involve risks including the possible loss of principal. The Fund is not intended to be a complete investment program. Many factors affect the Fund’s net asset value and performance.

Investment in derivatives (which include options, futures and other transactions) may give rise to leverage risk (which can increase volatility and magnify the Fund’s potential for loss), and can have a significant impact on the Fund’s performance. Derivatives are also subject to credit risk (the counterparty may default) and liquidity risk (the Fund may not be able to sell the security or otherwise exit the contract in a timely manner).

Futures contract positions may not provide an effective hedge because changes in futures contract prices may not track those of the securities they are intended to hedge. Futures create leverage, which can magnify the Fund’s potential for gain or loss and, therefore, amplify the effects of market volatility on the Fund’s share price. If an investment is linked to the performance of an index, it will be subject to the risks associated with changes in that index.

Investments in currencies are subject to the risks that those currencies will decline in value relative to the U.S. dollar, or, in the case of hedging positions, that the U.S. dollar will decline in value relative to the currency being hedged. Foreign investing involves risks not typically associated with U.S. investments, including adverse fluctuations in currency values, political, social and economic developments, liquidity, volatility, less developed and inefficient markets, political instability and differing auditing standards.

Emerging market countries may have relatively unstable governments, weaker economies, and less developed legal systems. Emerging markets may be based on only a few industries and security issuers which may be susceptible to economic weakness, default and liquidity issues.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Even Keel Mutual Funds. This and other important information about the Fund is contained in the prospectus, which can be obtained by calling 855-645-5462. The prospectus should be read carefully before investing. The Even Keel Mutual Funds are distributed by Northern Lights Distributors, LLC, member FINRA. Northern Lights Distributors, LLC is not affiliated with Milliman Financial Risk Management LLC or Milliman, Inc.

© Milliman Financial Risk Management

evenkeelinvestments.com