The first thing you notice when you are landing at Detroit Metro Airport in the winter after two weeks in the Caribbean is whether or not there is snow on the ground. I am pleased to report that other than a few clumps left by the snow plows or swept by the wind into the empty furrows and fenced-in corners of a farmer’s field, the six inches that covered everything when I left have largely disappeared.

Happily, I seem to have returned in the middle of an early spring thaw. Yesterday, the sun was shining and temperatures soared into the mid-sixties. Although the lake behind my home remains stubbornly frozen, as I pulled into the driveway I could see a pair of swans circling overhead, looking… hoping… for a patch of water to land upon. But hey, last year they came early, waited a couple of days, and then saw open waters until November. Here’s to hoping!

It seems that all the cold, dreary days of recession are thawing as well. While this is and will remain for perhaps all-time the longest recovery period for a recession in more than a century, it does appear to be thawing.

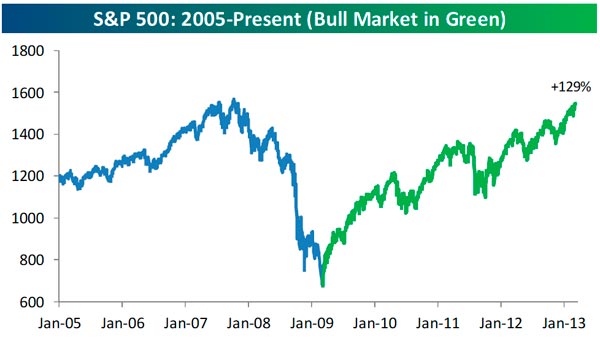

The sheet of ice overhead that has capped the long underwater voyage of the major stock market indexes is breaking up. Last week the ice finally cracked for the Dow as it topped its all-time high water mark from 2007. The S&P is just 1% below a similar break out.

Source: Bespoke Investment Group

As we have been reporting lately, a major propellant for the swift ascension in the stock market indexes has been improving economic indicators. Last week, there were fourteen economic reports released. Like most weeks this year, the number of reports outpacing the expert predictions outnumbered the disappointing ones.

Unlike the past, this time the majority was overwhelming, as better-than-expected results were registered by twelve of the fourteen reports – everything from non-manufacturing sales, to factory orders to employment – they all outperformed expectations! (The only laggard was Non-farm productivity and there was a tie for Average Hourly Earnings.) No wonder stocks have moved higher each of the last six trading days.

Normally, our spring thaw turns cold and snowy at least one more time. Is that what will happen to the thaw in our recession? It is a bit disconcerting to observe that although economic reports have beaten expectations of late, many still have failed to dig fully out of the hole they dug for themselves last year.

The research folks at the Bespoke Investment Group report that of the 40 economic indicators that they follow monthly, less than half (40%) are running ahead of their level a year ago. Sixty percent are still at levels below where they were last March!

Last year at this time, 65% of the indicators were running ahead of their year-to-year performance. So we are going to have to watch the indicators carefully to discern if, like the stock market indexes, the economy is breaking out of its doldrums as well. With sixteen more indicators scheduled to report this week, the wait may not be a long one.

While the economic reports have been propelling the stock indexes higher, the contribution of improving earnings reports has disappeared – but only because we have moved out of earnings reporting season. However, interest rates have resumed their climb. The 10-year bond yield hit a recent new high last week and upward pressure on rates could slow down a stock market advance.

We continue to take the Federal Reserve at its word and believe that Fed accommodation that saw $20 billion in bond purchases last week, with another $22 billion scheduled for this week, will continue throughout 2014. As a result, these purchases provide a strong tailwind to push the stock markets higher.

Yet their purpose is to hold rates down, and the fact that bonds keep rising even with the wind at their back makes me worry about those trillions of dollars of bond market investments that risk catastrophic losses if rates move substantially higher. I’m not going to join the chorus of advisors who for years have recommended moving out of bonds, only to see rates move still lower. But I do advise you to move from buy and hold positions in long-term CDs, bonds, and especially bond funds, to an actively managed bond portfolio.

An actively managed bond portfolio can take advantage of many defensive tools when, not if, interest rates move substantially higher. An actively managed portfolio can shorten the maturities of the bond investments held. Shorter maturities mean less exposure to rising interest rate-induced losses. Actively managed bond portfolios can move to the stable safety of money market funds or even turn to inverse funds that profit from rising rates. And, of course, if you utilize a high yield bond strategy you can also benefit from rising stock prices.

If you haven’t made this adjustment yet, now’s the time to do some spring cleaning. While you’re at it it’s not a bad time to make sure you are in an actively managed portfolio on the stock side of your portfolio as well.

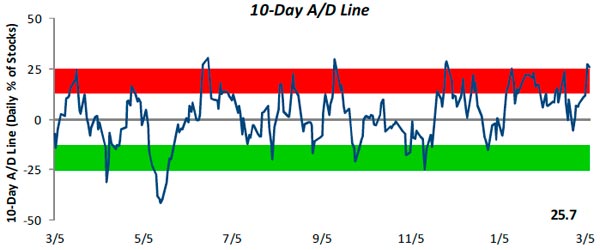

These new highs are great, but we have moved higher every week but one this year and stocks have gone up now seven days in a row. As the indicator below shows, the broader measures of the stock market are getting overheated, and sooner or later a correction will ensue.

Source: Bespoke Investment Group

An actively managed equity strategy can stick with the market if the S&P, for example, at last moves above its 2007 highpoint. But that’s less than 1% higher! What an active stock market strategy can also do is move you to less volatile investments if the rally starts to unravel.

Of course, as I always say, whatever strategies you turn to make sure you diversify strategically. Unlike the swan circling the frozen lake, it’s nice to have options if the climate suddenly changes for the worse and an early spring thaw turns into a late winter storm.

All the best,

Jerry

© Flexible Plan Investments