Investors love an oligopoly. Imagine an industry dominated by a few large, long-standing players. They can earn outsized profits in boom times and avoid crashes thanks to rational capital spending. The existential questions, though, are whether these firms might turn on each other, and is the industry’s entry barrier high enough.

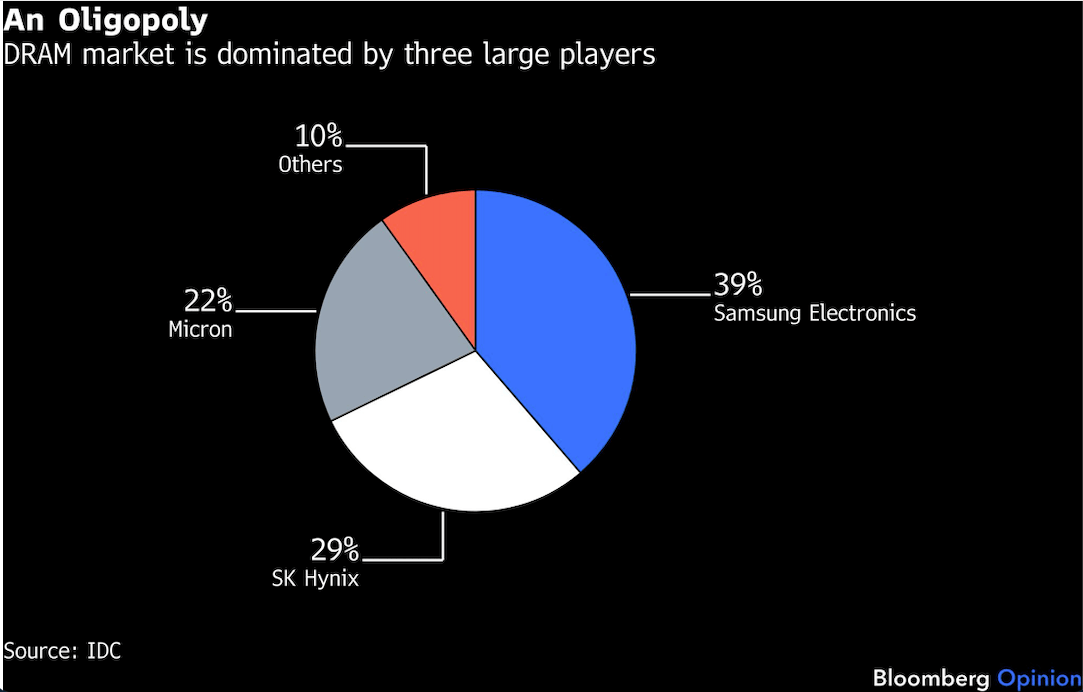

Samsung Electronics Co., SK Hynix Inc. and Micron Technology Inc. are thriving in part because of this competitive structure. They own about 90% of the global dynamic random-access memory, or DRAM, market, and are the only suppliers of the high-bandwidth, or HBM, chips that pair with Nvidia Corp.’s graphics processing units. With booming AI demand, the trio is enjoying record profits.

China is starting to look like the upstart that can disrupt the joyride. ChangXin Memory Technologies Inc., or CXMT, is seeking to raise $9.8 billion in an initial public offering in Shanghai, right on the heels of SK Hynix’s blockbuster $26.5 billion US listing last week. Investors will begin subscribing for shares on Thursday.

CXMT has the momentum. It’s the country’s only viable contender to challenge the oligopoly. Its market share has roughly doubled to 8% from a year ago. Benefiting from worldwide memory shortages — China is hungry, too — the company is getting a boost as the big three divert their capacity to make HBM. In the first half, it is expected to generate up to 120 billion yuan ($17.7 billion) in revenue and 75 billion yuan in net income, a sharp turnaround for a firm that was in the red as recently as mid-2025.

Clearly wary of China’s industrial prowess, analysts have conducted studies on whether CXMT can disrupt the current market makeup. The company is secretive with its ambition, but according to Bloomberg Intelligence, its progress with HBM has reached the engineering stage. But the chipmaker is not able to make these advanced semiconductors at commercial scale yet.

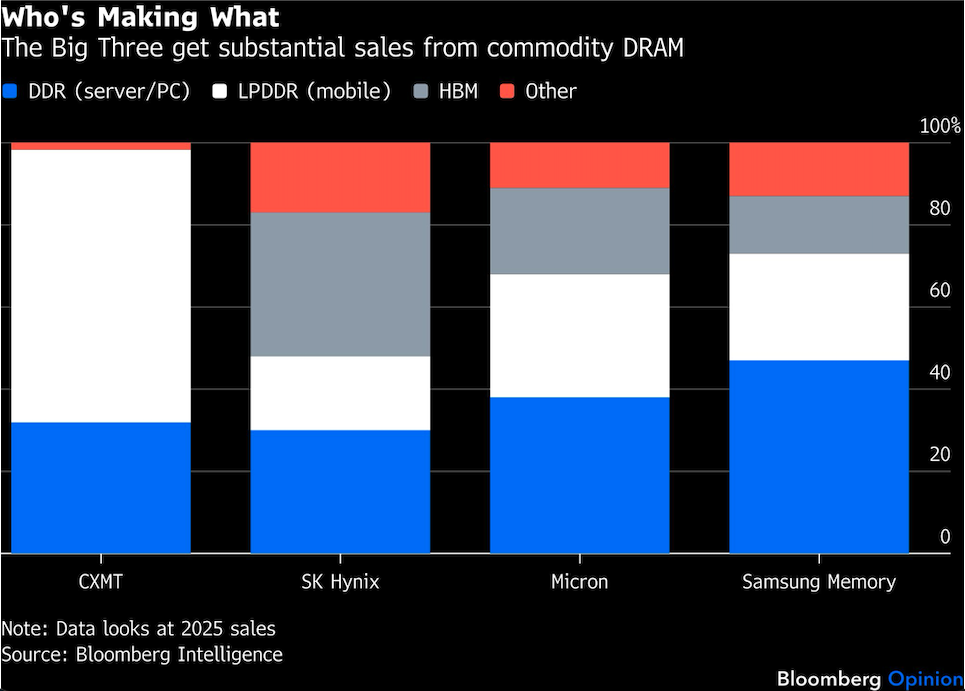

As for conventional DRAM, CXMT is already capable of mass producing the next-generation Double Data Rate 5, or DDR5. But its profitability is lower compared to peers, because it runs on older and larger nodes.

Nonetheless, when have slim margins stopped China from trying? Once listed, CXMT will have the dry powder to upgrade its production. The company reportedly plans to boost capacity by two-thirds by 2028. For reference, SK Hynix has said it will double capacity in five years.

Even if China can’t crack the HBM stranglehold, its more immediate presence in conventional memory can hit the earnings of Samsung, SK Hynix and Micron. This is because a sizable chunk of their sales still stem from commodity DRAM. And more importantly, it’s this segment — not HBM — that underpins record profits. While HBMs are often sold under annual contracts, which means their unit prices are relatively stable, prevailing costs of conventional chips have skyrocketed this year.

Moreover, CXMT’s IPO is a direct challenge to memory bulls’ supercycle argument. Its aggressive capacity expansion will exacerbate an industry downturn after the cycle peaks. In addition, the big three can nudge their customers to sign favorable long-term agreements only if they have bargaining power. But will they lose it when a newcomer is knocking at the door? Apple Inc., for one, isn’t taking the bite. It’s reportedly in negotiations to purchase chips from the Pentagon-blacklisted CXMT.

After SK Hynix’s US debut, there’s been a lot of discussion on what it plans to do with the money and how capacity expansion could affect supply-demand dynamics. This conversation will only get more heated when CXMT gets its $10 billion.

Whenever there’s a big party, you can bet China will be there.