Meme mania swept through Wall Street in 2021. Retail investors gathered on social media and coordinated trading strategies to short squeeze high-profile hedge funds. Their success was more than financial; it was hailed as a David versus Goliath battle, a victory for the underdogs that toppled the almighty.

That was just a skirmish. The conflict between retail and professional investors today has extended well beyond “degen” traders active on Reddit and a few hard-charging hedge funds. We now have middle-class households frantically managing their wealth to beat AI job threats, pitting them against asset managers de-risking and rebalancing portfolios according to the industry’s conventional wisdom.

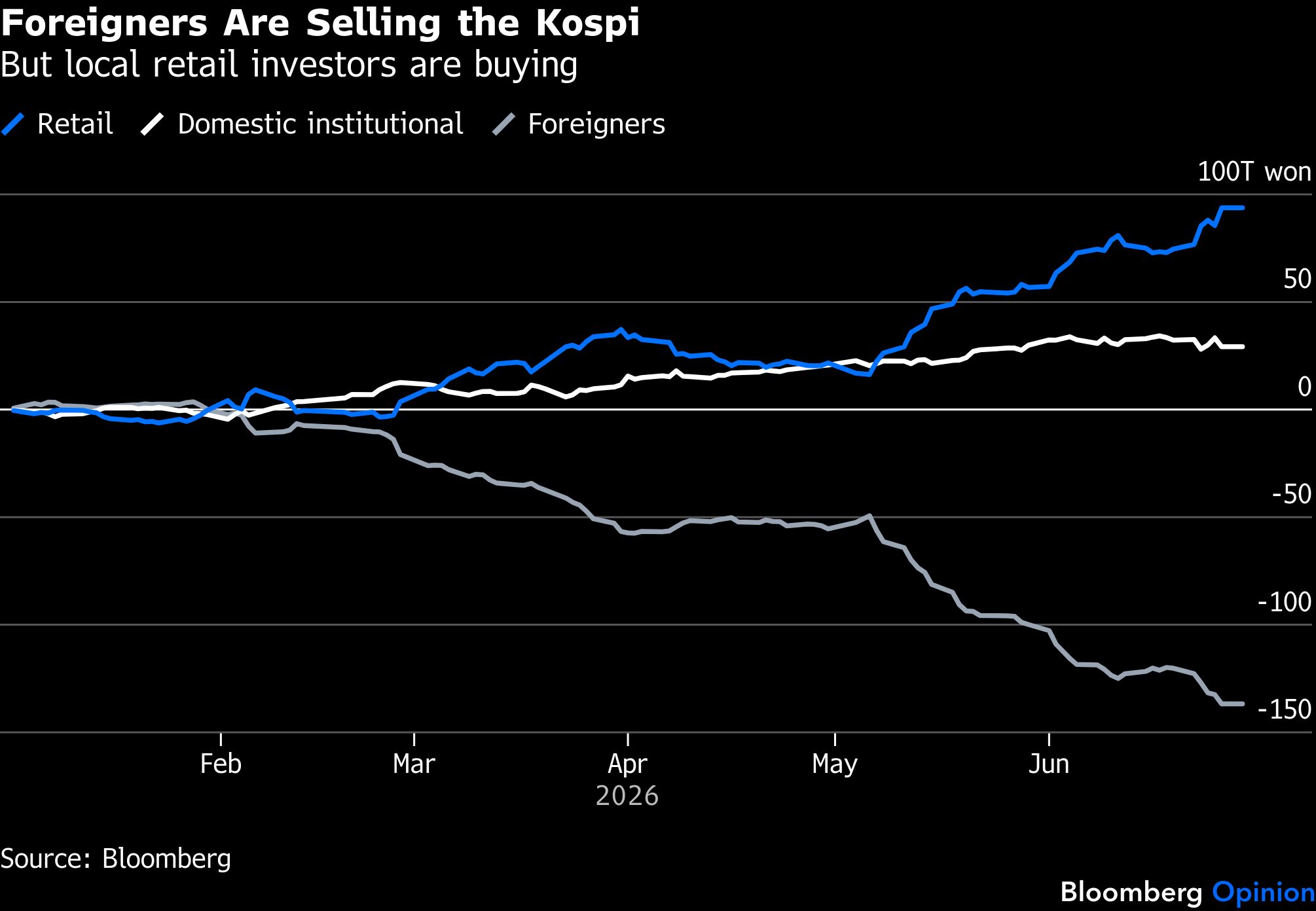

This tension is most pronounced and easiest to track in South Korea and Taiwan, home to the world’s best-performing stock markets this year. Foreign institutional investors have sold more than $110 billion of their holdings, while local retail traders have filled the void.

Professionals are selling because of concentration risk brought on by the parabolic rally in AI infrastructure stocks. The MSCI Emerging Markets Index, in particular, has gone through a structural change. Three stocks — Taiwan Semiconductor Manufacturing Corp. and South Korea’s Samsung Electronics Co. and SK Hynix Inc. — now account for over 30% of the entire index, versus 18% at the beginning of the year. Ironically, by that weighting, China — the world’s second-largest economy — is now only the third-largest emerging market.

Everyday traders, on the other hand, are not worried about a handful of stocks dominating their holdings. Many chase them, purchasing single-stock leveraged exchange-traded funds to amplify their returns. In addition, it’s clear that simply buying a broad-based index fund — championed by the modern portfolio theory — is no longer sufficient to protect one’s wealth. This is because market leadership has changed: US hyperscalers’ capital spending is turning them from cash cows into the Maleficent 7, while semiconductor suppliers are benefiting from the trillion-dollar AI investment boom.

This shifting dynamic has raised an existential question: Does diversification, the cornerstone of portfolio management, still make sense when the world is undergoing seismic changes?

Traditional managers are probably underperforming this year. Just look at what those who pared back their Korean holdings early have missed: Samsung and Hynix are up 168% and 303%, respectively.

Further, it might be wrong to say concentrated portfolios are destined to fail. Billionaire Chris Hohn’s Children’s Investment Fund is, by some measures, the most profitable hedge fund of all time, according to data compiled by the Financial Times. Hohn manages about $77 billion in only 15 positions globally. As such, diversification is starting to look like an excuse for those who haven’t done their homework and thus have no conviction.

Even in the slow-moving world of pension funds, there are early signs that David is winning again. In late May, South Korea’s National Pension Service lifted its domestic equity target for the year in an attempt to hold onto its better-performing positions. The $1 trillion fund is the undisputed Kospi whale, owning 7.9% of Samsung and 8.1% of Hynix.

Meanwhile, the $600 billion California Public Employees’ Retirement System, the largest pension fund in the US, went a step further. It’s adopting a so-called total portfolio approach, ditching rigid allocations to stocks, bonds or private equity in pursuit of the best possible returns. The strategy goes live in July.

In other words, facing defeat, the modern-day Goliath is starting to re-examine what constitutes an optimal portfolio, and whether the benchmarks being used to evaluate performance still make sense.

To be sure, as retail investors take the reins, stock markets will likely become more volatile. In South Korea, for instance, derivatives activity associated with leveraged ETFs are creating sharp daily price swings.

Nonetheless, small investors’ direct participation in the stock market is a welcome wake-up call for the professionals. Their day-trading dip-buying reflex at the onset of the Iran war gave them the upper hand, and active stock selection in the AI pick-and-shovel universe has further amplified their wins. So who’s the real smart money here?