Wall Street strategists expect the Federal Reserve to take a slow and careful approach to winding down a program meant to help ease pressure in funding markets.

The Fed abruptly stopped shrinking its balance sheet — a process known as quantitative tightening — at the end of 2025 and pivoted to adding reserves back into the financial system by buying short-term Treasuries due in less than a year.

In December, the central bank began buying about $40 billion of bills each month in a bid to ease the pressures that were building in short-term rates. At that time, Chair Jerome Powell said the Fed was “front-loading” its purchases to ensure there were enough reserves through the April tax season.

Roberto Perli, the New York Fed official who manages the central bank’s multi-trillion dollar securities portfolio, said in a blog post last month with colleagues that the monthly pace of purchases is likely to be “significantly reduced.” Between mid-April to mid-May, they said the decrease could be “somewhat gradual” to account for uncertainty and other factors.

The Fed’s schedule is expected to be out Monday at 3 p.m. New York time.

“I think Monday’s release will set the pace for how quickly the Fed wants to get to an end state,” said Gennadiy Goldberg, head of US interest rate strategy at TD Securities. “That’s what the minutes and remarks from Perli basically imply — they will be moving cautiously to ensure there are no missteps.”

Bill purchases since December — about $217 billion, including the reinvestment purchases — have ensured funding markets continued to function smoothly in 2026, especially as flows from this week’s US income tax payments are expected to cause gyrations in reserve balances, causing volatility in overnight markets. That’s why market participants are expecting the Fed to move cautiously as it reduces the size of its purchases.

Perli noted income-tax payments were expected to cause wide swings in the Treasury General Account and reserves, with balances troughing in late April, March 18-19 FOMC meeting minutes showed. Perli said in the blog that he expected the level to be about equal to what was seen at the end of 2025 and around $3 trillion after the end of April through September.

Yet, others like Wrightson ICAP senior economist Lou Crandall believe the Fed could safely cut its monthly purchases by a larger amount, noting Powell’s December remarks regarding the tax season, which is a pressure point for reserves.

“The Fed is likely to come out of the tax season comfortably in the upper part of the ‘ample’ range, and we don’t see any pressing need to continue to increase the size of its reserves cushion as the second quarter progresses,” Crandall wrote in a note to clients Monday, adding that the central bank could also change its mind in the next few months.

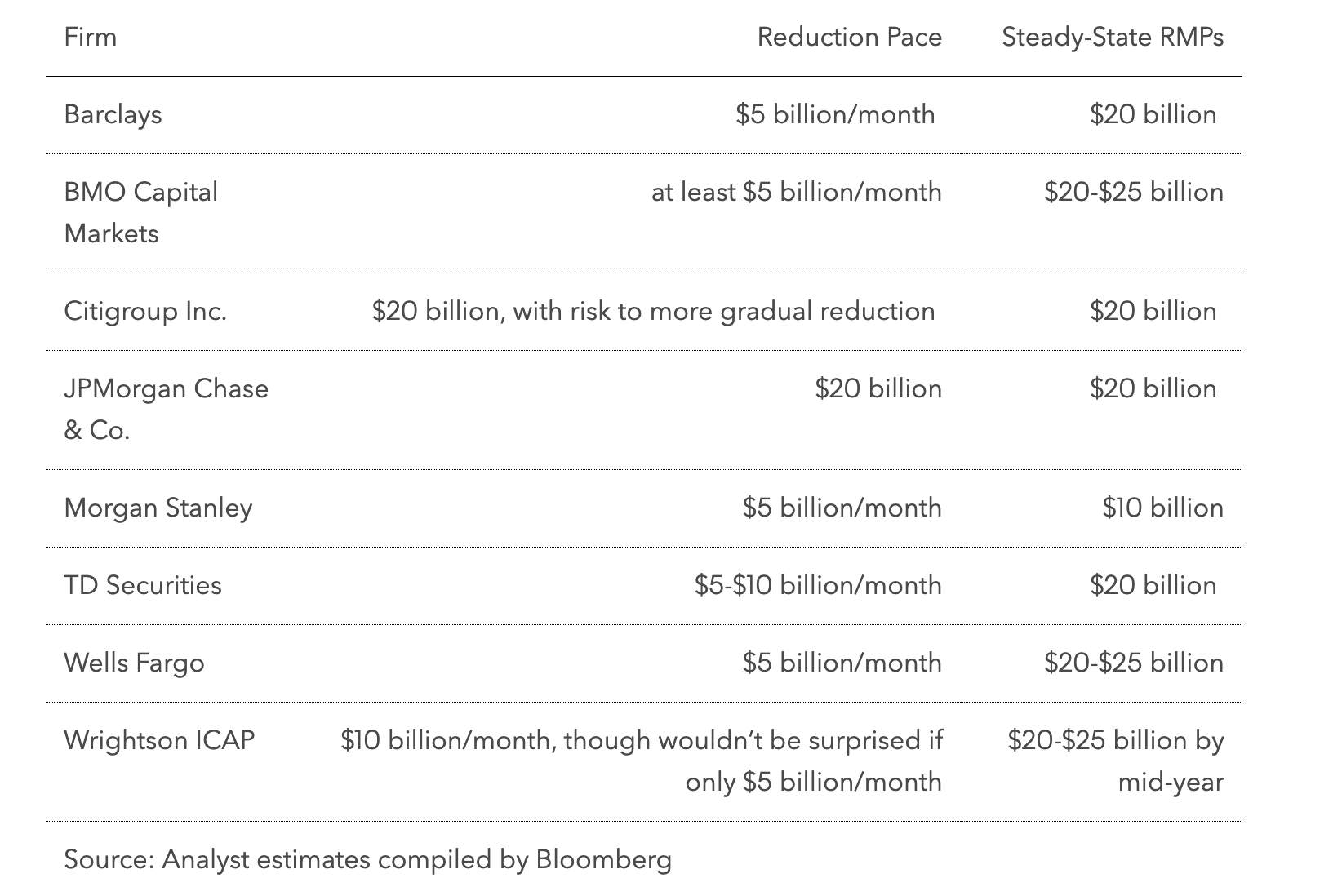

Here’s how strategists are thinking about the Fed’s RMPs:

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Alexandra Harris