Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

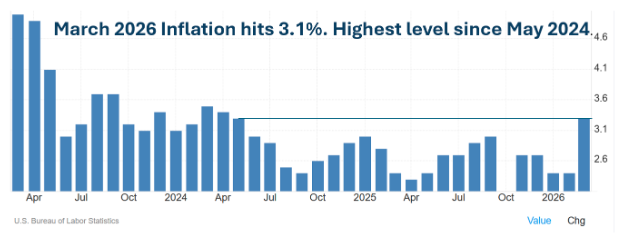

- Inflation in March 2026 was 3.1%, a level last seen in May 2024.

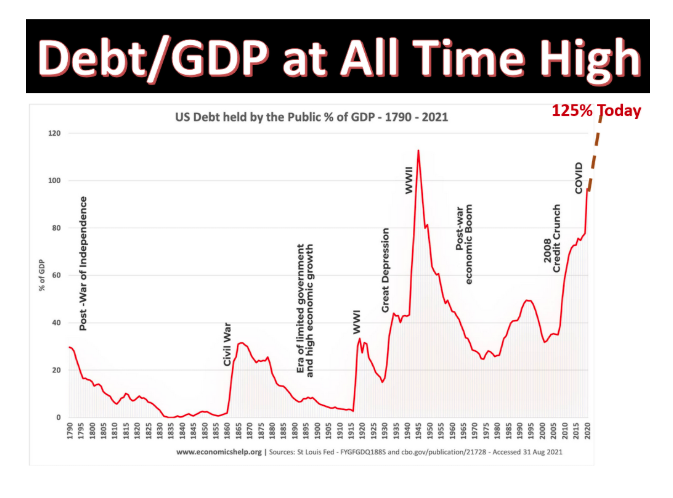

- At 125% of GDP, U.S. national debt is at its highest level ever. “Highest ever” is probably too high.

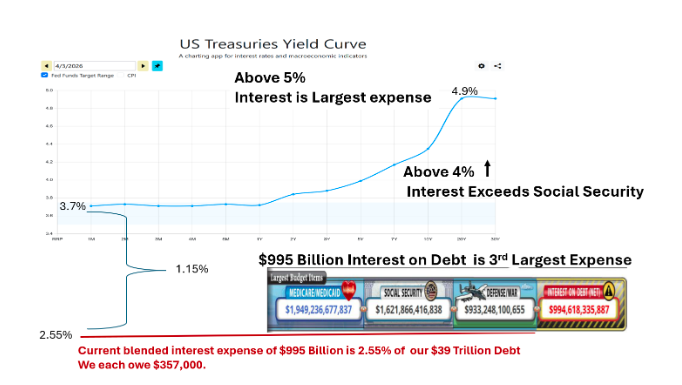

- The blended interest rate on debt is currently 2.5%. This rate is going up and so is the amount of debt — a double whammy.

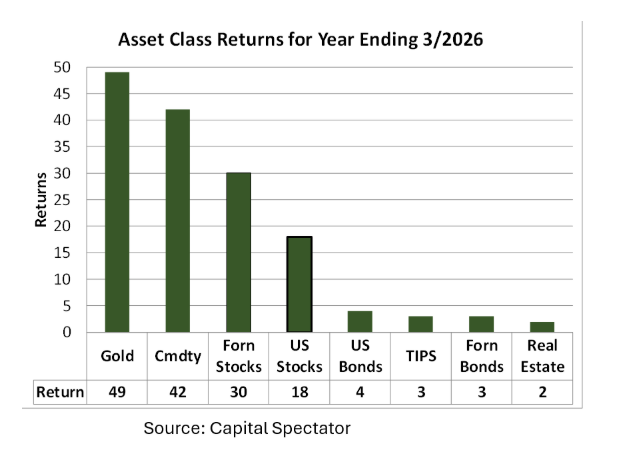

- Precious metals and commodities provide inflation protection, as do Treasury Inflation Protected Securities (TIPS). Stocks are not a good inflation hedge.

Driven by rising energy prices, inflation rose to 3.1% last month. This is likely the beginning of more to come.

Current interest of $995 billion is 2.5% of the $39 trillion national debt. This blended 2.5% interest rate is heading higher as old issues mature and new bonds are issued. The $39 trillion debt is 125% of the country’s $31 trillion GDP, its highest level ever and headed even higher. This double whammy driving increases in interest expense can’t be stopped. Debt monetization will bring rampant inflation.

Interest Expense

As shown in the following graph, the U.S. is paying 2.55% interest on its $39 trillion national debt — amounting to $995 billion — making it the third- 3rd largest expense behind Social Security and Medicare. 2.55% is well below (by 1.15%) the current yield curve, so the blended rate will increase if the Federal Reserve leaves interest rates as-is or higher.

The Treasury increases its borrowing by $2 trillion each year, which means that new bonds are issued that yield at least 3.7% currently. This drives up blended interest expense above the current 2.55% and increases the individual share above the current $357,000. If the blended rate reaches 5%, debt service will become the U.S.'s largest expense. The Fed could move to lower interest rates, but this exacerbates inflation that is already on an upward trajectory.

Double Whammy

The amount of debt is increasing while the interest on that debt is also increasing, begging the question: How high is too high? Part of the answer lies in the fact that the current debt at 125% of GDP is its highest ever — even higher than after World War II.

Highest ever feels like it’s probably too high. Something will break, like monetizing the debt — basically money printing that fuels inflation fires.

Adding to this concern, President Trump has requested approval to increase national defense spending well above the currently budgeted $933 billion. The wars in Ukraine and Iran have cost more than $700 billion so far and growing, so there is not much left in a $933 billion budget.

Conclusion

Inflation fears are not new, but the current path is beyond alarming. The U.S. is spending its way into a rampant inflation catastrophe. That is why gold and commodities are being bid up in price and will likely continue to be bid up. Investors see the inflation threat and are protecting themselves.

Treasury Inflation Protected Securities (TIPS) also defend against inflation. It will be interesting to see if the Treasury limits or halts new issues of TIPS. Will the promise be kept to tie redemption value to inflation?

Diversification into inflation protected securities is smart at this time. I suggest TIPS even though they are not currently among the best-performing asset classes. Stocks are not a good inflation hedge, although investors have recently preferred non-U.S. stocks over expensive domestic stocks.

What do you think? Are you protecting yourself against inflation? Should you?

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Ron Surz is president of Target Date Solutions, developer of the patented Safe Landing Glide Path and Soteria personalized target date accounts. He is also co-host of the Baby Boomer Investing Show. Surz’s passion is helping his fellow baby boomers at this critical time in their lives when they are relying on their lifetime savings to support a retirement with dignity, so he wrote a book, “Baby Boomer Investing in the Perilous 2020s,” and he provides a financial educational curriculum.

For anyone who relies on TDFs — or advises those who do — Surz’s new book is a must-read guide to understanding the risks, solutions, and future of a secure retirement.

Read more articles by Ron Surz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.