The stock market is looking past the sharp interest rate hikes priced by Europe’s bond market, risking losses for investors backing the wrong outcome.

Swaps imply three European Central Bank rate increases this year, reflecting how the region is particularly exposed to energy shocks triggered by the Iran war. While growth concerns are also starting to emerge, there’s widespread conviction that central banks will be eager to ensure inflation is kept under control.

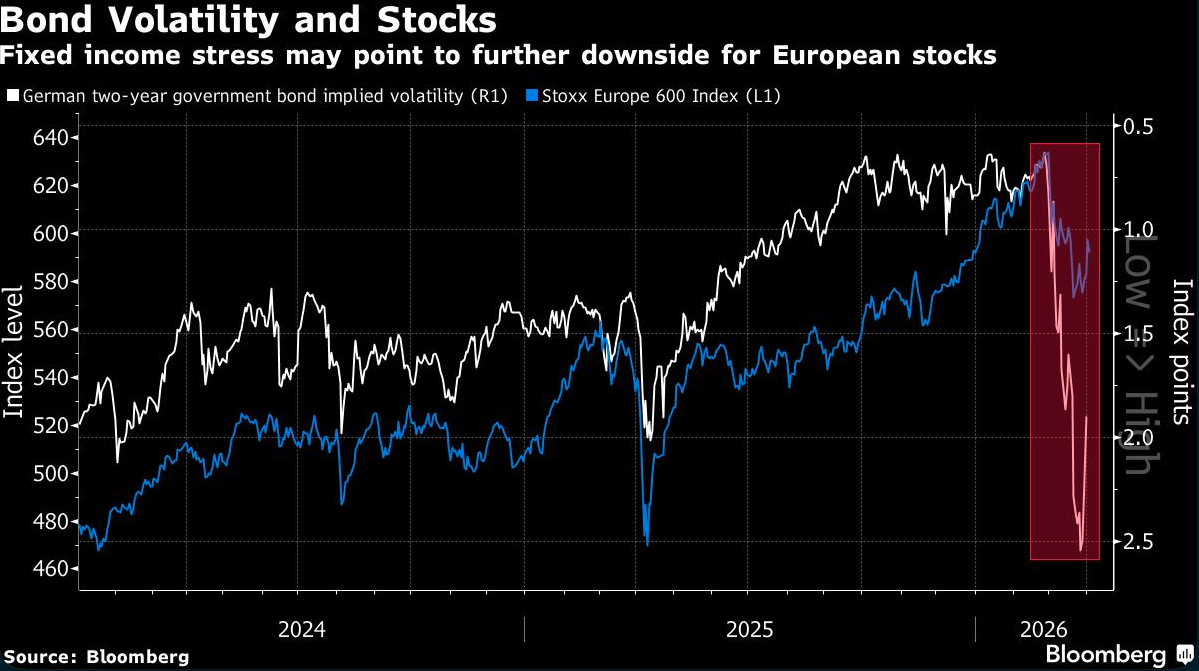

Moves in stocks, however, are more in keeping with slowing economic growth that will keep rates stable, or even lead to easing.

“The market is schizophrenic when it comes to possible ECB rate hikes or cuts,” said Karen Georges, an equity fund manager at Ecofi in Paris, describing the divergence between moves in equities and bonds. “We are clearly among those who don’t see two hikes — let alone three, given how a prolonged crisis would hit economic activity. It’s even possible to envisage a rate cut by the end of the year if there’s a substantial impact on growth.”

Benchmark German 10-year bond yields hit a 15-year high on March 27 and BlackRock Inc. is among major investors betting on further losses. While the Stoxx Europe 600 Index just recorded its worst month since June 2022, valuations remain high. Members of the benchmark gauge trade at around 15 times forward earnings, well above the average of the past two decades.

Market expectations for European earnings highlight a similar contrast: analysts predict profit growth of 11% for 2027. To make that a reality, companies will need benign economic conditions and favorable borrowing costs, rather than the aggressive rate-hike expectations showing up in bonds.

For Amélie Derambure, a senior multi-asset portfolio manager at Amundi in Paris, bond markets are responding to the conflict as if its inflation impact will resemble the fallout from Russia’s invasion of Ukraine four years ago.

“I find the market price reaction in the fixed income market particularly brutal,” she said. “Stock markets are still uncertain as for the economic consequences of the conflict, but the bond market is already looking at a 2022 type of scenario.”

The risk for stocks is that the economy falters, earnings disappoint and central bank easing fails to materialise, putting pressure on valuations that remain fairly rich.

In the US, the S&P 500 Index is seeking to snap a run of five consecutive weeks of losses, the longest losing streak since 2022. But Wall Street equity valuations remain elevated. The cyclically adjusted price-to-earnings Shiller ratio recently rose above 38 times, among its highest readings in over 150 years of data, despite the recent drop in equity prices.

‘Transitory Disruptions’

US investors, too, appear to have learned to ride out geopolitical shocks. The tactic has paid off numerous times in the past few decades, including after the Gulf and Iraqi wars when equity markets were higher within six months of the conflict, even as oil spiked. More recently, this has been true of the start of the Ukraine war and the “Liberation Day” tariff turmoil of April 2025.

“Recent history has taught investors to treat geopolitical disruptions as transitory due to the relatively limited economic impact that they have had,” said George Nadda, a portfolio manager at Altana Wealth in London.

Like in Europe, US equity investors continue to put their faith in increased earnings. American sell-side equity analysts have been reluctant to alter their profit outlooks, with EPS estimates actually trending higher ahead of April’s reporting season.

Investors have also retained the optimism that prevailed before the conflict about strong US economic growth, supported by fiscal stimulus and continued large-scale expenditure in artificial intelligence.

Kevin Thozet, a member of the investment committee at Carmignac, in Paris said that the gap between the fixed income and stock markets could probably be partially explained by a fundamental bias in their outlook. “By definition, stock investors are optimistic and looking for the profits that await in the future, while for bonds, it’s really all about protecting yourself against inflation.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Julien Ponthus and Olivia Levieux