When someone says a retiree is “living off Social Security,” it’s not usually $100,000 a year. But some US retired couples will be receiving that much in a few years — and a proposal to cap their benefit at that amount has started a painful and much-needed conversation about who should get government benefits and how much.

America’s welfare state is not just a safety net for the most needy or unlucky. Over time, it has become a significant source of income and services for the middle and upper-middle class. There is nothing wrong with that, in principle, if it’s what Americans want. In reality, however, the federal government cannot afford it. Cutting benefits for wealthy retirees is an obvious first step, but truly getting the debt under control will require reductions for other people, too.

The $100,000 annual Social Security benefit — which will go to about 0.05% of retired couples at first — may seem unbelievable. But if you and your spouse have both earned the maximum salary for the last 35 years (it was $53,400 in 1991 and is currently $184,000), and you each claim your own benefits, your household will get $99,648 this year, indexed for inflation. If you both wait till age 70 to claim, you’ll get nearly $125,000.

Under the proposal, from the Committee for a Responsible Federal Budget, individual benefits would be capped at $50,000 if claimed at the normal retirement age (currently 67 for most people), or $62,000 if delayed to 70. These benefits would not be adjusted for inflation for 20 to 30 years (depending on how it is implemented), and there would be a ceiling on benefits for future higher-earning retirees.

The CRFB, a nonpartisan think tank, estimates that its plan would reduce the Social Security shortfall by one-fifth over the long term and three-fifths over the next 75 years. That’s similar to the savings that would be gained if payroll taxes were applied to earnings above $184,000. It’s also a better idea, because it avoids a very large tax increase and, at least for the first decade or so, would be more progressive.

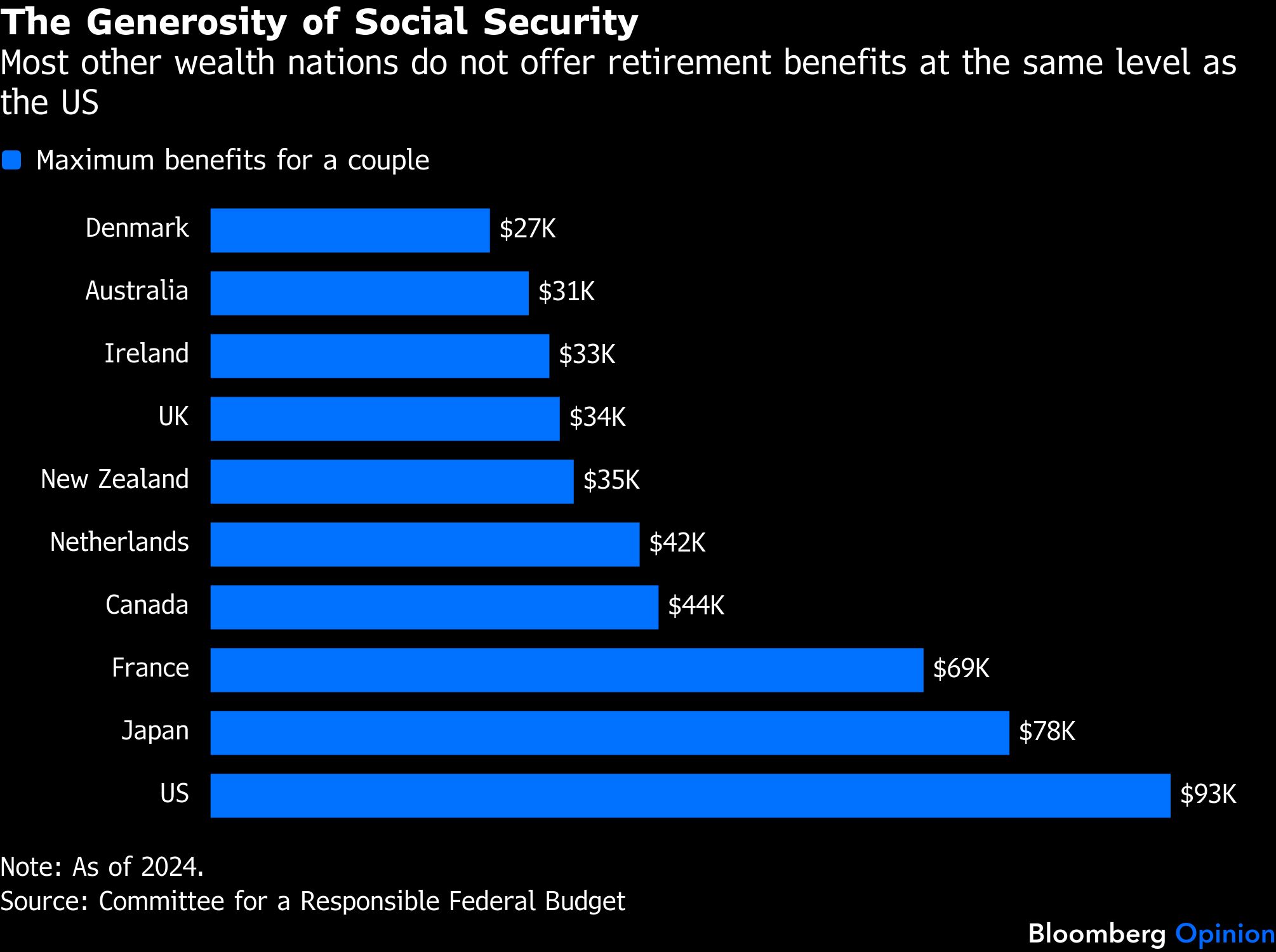

Most other wealthy countries don’t offer such generous public benefits. In the US, if you and your spouse earned at least the taxable maximum for most of your careers, you probably have other forms of saving (or at least the ability to save) and don’t need more than $100,000 from the federal government.

But Social Security was never just about needs. It is intended to be both an insurance program to keep people out of poverty in old age, and a savings program to replace a decent share of income. Offering such generous benefits may have been realistic when the population was younger and payroll taxes were only 2%. Now the population is older and payroll taxes are 12.4%; if nothing is done, benefits will be cut more than 20% in 2034.