Private Credit Stress: Will the Fed Backstop Exuberant Markets Again?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The Federal Reserve is governed by its dual congressional mandates: price stability and maximum employment. At times, however, the Fed throws these mandates out the window to protect the financial system. With liquidity and credit stress in the private credit market rising, we must consider whether the Fed might once again ignore its mandates to backstop exuberant markets.

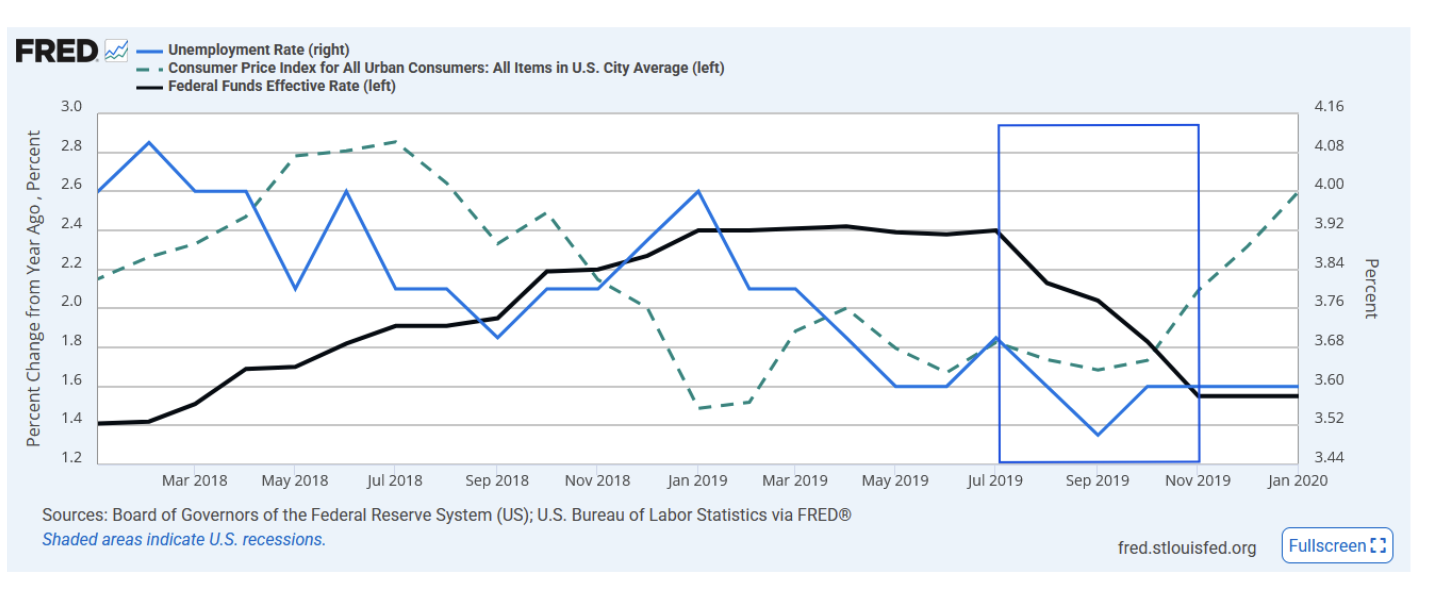

The Fed has a history of cutting rates and boosting liquidity when the labor market and inflation levels don't necessitate action. In 1998, the Fed cut rates three times in rapid succession and orchestrated a private-sector rescue of Long-Term Capital Management to prevent the hedge fund's collapse from cascading through Wall Street. More recently, in 2019, the Fed injected hundreds of billions of dollars into the repo markets and cut rates when overnight funding rates spiked — despite no immediate connection to inflation or unemployment.

To help evaluate whether rising stress in private credit will warrant Fed action, we explain the mechanics of the asset class, identify the key players, compare the current situation to the subprime crisis, and outline how this stress could prompt the central bank to act.

What Is Private Credit?

The term private credit refers to loans made directly by non-bank lenders. The sector has grown immensely, from under $500 billion 10 years ago to approximately $1.2 trillion domestically and $1.7 trillion globally. It is currently one of the fastest-growing sectors of the financial system.

Borrowers are typically companies that cannot access public debt markets. Often, these are small- and mid-cap companies carrying significant leverage — many the result of private equity buyouts financed with debt.

Among the largest lenders are Apollo, Blackstone, Ares, Blue Owl, and KKR. These entities create private credit funds using investor capital and leverage to issue loans. These funds charge relatively high interest rates because they have a captive audience; banks, constrained by post-2008 regulations, are often no longer willing or able to provide financing to these firms.

Investor Benefits

- High yields: Due to illiquidity, private credit loans offer higher yields than similarly rated bonds in the public debt market.

- Senior security: These loans are often at the top of the capital stack. In the event of default, these investors are the first to be repaid. Furthermore, many loans are collateralized.

- Diversification: Funds diversify by lending across different companies and industries.

- Lower perceived volatility: Because these loans do not trade daily and are only priced quarterly, they are perceived as having lower volatility.

- Floating rate: Most private credit loans have floating interest rates, which helps limit price drawdowns when yields rise.

Investor Risks

- Credit risk: As with all debt assets, the primary risk is default and loss of principal. This risk is elevated not only by the borrower's financial condition but also by the leverage employed by many private equity funds.

- Liquidity: Investors are often unable to sell holdings due to lock-up periods, which are typically five to 10 years. Recently, many funds have limited repayments to levels well below what investors requested.

- Floating rate: While a benefit to the lender, rising rates increase the borrower’s rates, thus increasing the risk of default.

- Lack of transparency: Because these loans do not trade or have a current market price, investors have little insight into their real-time value. As a result, debt prices can drop from par to near zero with no warning.

Private Credit Investors

The largest holders of private credit funds are pension funds, insurance companies, sovereign wealth funds, endowments, and family offices. These are generally accredited, sophisticated investors who understand that the yield premium comes at the cost of illiquidity. In many cases, these investors can absorb significant losses without disrupting the broader system.

Systemic Risk

At first glance, $1.2 trillion in debt sounds manageable — roughly 2% of the $55 to $60 trillion total U.S. debt market. However, an unraveling in the private credit sector can introduce systemic stress.

The 2% figure is misleading for several important reasons. First is concentration. The debt is heavily concentrated in riskier leveraged buyouts and the software and technology sectors, which are particularly exposed to potential disruption from AI.

Second is transparency. Private credit is priced quarterly by managers using internal models rather than market prices. Credit stress can build without visibility, resulting in sudden, large price adjustments.

Along the same lines as the headline above, this excerpt is from our article, "Fitzpatrick: Soros CIO Warns Of A Reckoning:"

A third risk is integration. In some cases, the insurance company, the investor, and the private credit fund are a single entity. Over the last decade, large alternative asset managers acquired life insurance companies to use as funding vehicles. For example, Apollo bought Athene, KKR purchased Global Atlantic, and Brookfield acquired American Equity. These insurers collect annuity premiums from American households and invest some of those premiums into private credit originated by their parent companies. This circular arrangement benefits all parties when times are good, but the ultimate risk lies with individuals depending on annuity income for retirement.

Comparing Bubbles: Private Credit vs. Subprime

The instinct to compare recent private credit stress to the 2008 subprime mortgage crisis is understandable, but the comparison is nuanced.

Similarities

- In both cases, credit was extended aggressively, with loosening underwriting standards.

- Both involved opaque assets — subprime mortgages were bundled into CDOs, while private credit is valued quarterly using models rather than observable market prices.

- Risk was initially funded through entities thought to be capable of withstanding volatility, making concentration risks.

Differences

- Consumer vs corporate: Subprime was a consumer credit problem that threatened homeowners. Private credit is primarily a corporate problem concentrated in leveraged buyouts of businesses.

- Subprime was embedded in the banking system through exposure to CDOs, creating direct contagion channels to systemically important institutions. Private credit sits largely outside the banking system, in private funds with locked-up capital — meaning there are no depositors to run and no repo lines to pull — which is a genuine structural advantage over 2008.

The critical difference, in our opinion, is the entanglement of insurance companies. While this makes private credit structurally safer than bank funding, it shifts the risk to the retirement savings of mom-and-pop investors.

Why the Fed Would Cut Rates

The Fed will not announce it is cutting rates specifically to protect private credit. However, it would respond to the consequences of private credit stress if they threaten economic stability. This could happen in three ways.

If private credit stress leads financial institutions to pull back on lending, small- and mid-market companies will find capital scarcer. Tightening conditions slow investment and put pressure on unemployment, giving the Fed legitimate cover to ease.

The second is the wealth effect. If insurance balance sheets are impaired, regulators may force asset sales. Furthermore, if policyholders face uncertainty regarding annuity values, they may reduce spending, resulting in weaker consumption and slower growth.

The third is the financial stability channel. If stress leads to a crisis of confidence in systemically important banks or markets, the Fed would likely respond with quantitative easing (QE) and lower rates.

Summary

Private credit is not subprime. It is better structured, less leveraged, and sits largely outside the major banks. However, it is larger and more deeply entangled with retail beneficiaries than in the past. At $1.2 trillion domestically, it is now comparable in size to the entire high-yield bond market.

The Fed will not cut rates because of private credit stress, but it will cut if that stress morphs into tighter credit or weaker consumption.

The more important question for investors is whether rate cuts can solve a problem that is, at its core, about credit quality rather than the costs of borrowing.

Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information, contact him at [email protected] or 301.466.1204.

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All