The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

My clients often seek my opinion on matters beyond financial planning that sometimes involve life choices. I respond that I’m strictly a financial advisor and have absolutely no qualifications to tell them how to live their lives. I assure them that I’m still a work in progress in my own life. Despite having little expertise when it comes to the subject of happiness, I’m fascinated by the subject of money and happiness.

What insights I do have mainly come from three sources: my own mistakes; research from Harvard psychology professor and author of the book “Stumbling on Happiness,” Daniel Gilbert; and lessons from the late Jonathan Clements. Jonathan wrote over 1,000 columns for The Wall Street Journal and many more for his HumbleDollar.com website.

Below, I discuss my own failed experience, review research on money and happiness, and offer my hypothesis on investing and happiness.

The Theory of Saving & Investing (a Sad Tale)

Why do we save and invest? The answer is obvious. We defer immediate gratification (spending) so that later in life, we can enjoy the financial freedom to do what we want. We invest the money we save in the hope that it will grow faster than inflation and taxes, so we can reach financial freedom sooner. That financial freedom will allow us to do what we want with our lives, which will make us happy — at least that’s how the theory goes.

I lived by that theory for the first two decades of my career in corporate finance and management consulting. Although I enjoyed much of that part of my career, I didn’t love it. I couldn’t wait to be financially independent, so I lived quite frugally and saved a bundle.

That frugality included investing, and I have been an indexer since the late 1980s. That frugality in spending also meant I never got on the hedonic treadmill and was proud to live beneath my means to secure the future. I was part of the FIRE (financial independence retire early) movement before there was such a thing. I thought I was doing everything right.

It finally happened about 22 years ago. My family and I became financially independent. I could do almost anything with the rest of my life. Yet, to my utter surprise, I wasn’t happy.

I had no idea what I wanted to do with the rest of my life. The realization dawned that the central space my work had occupied in my life could not easily be replaced with hobbies or make-busy projects. My sense of self-worth was depleted, along with my social network, which included friends I would regularly see at work.

Where did I go so horribly wrong? Though I had financially prepared for retirement, I had not really prepared to be retired. I just assumed financial independence meant I would be happy, but as noted in the book “How to Retire” by Christine Benz, I had completely failed in visualizing what would make me happy in retirement.

Ultimately, my retirement lasted about a month. It was an epic failure.

Research on Money and Happiness.

As Daniel Gibert’s research shows, and my experience supports, we are terrible forecasters of future happiness. Happiness is strongly shaped by how we’re doing relative to others, not just by objective conditions.

Johnathan Clements did more research on the subject of money and happiness than anyone I’m aware of. He asserted that we should use our money to purchase experiences, not possessions.

“One reason experiences bring so much happiness is that they’re often shared with others,” he observed. By that logic, spending money on a family vacation is likely to yield more happiness than a fancy luxury car.

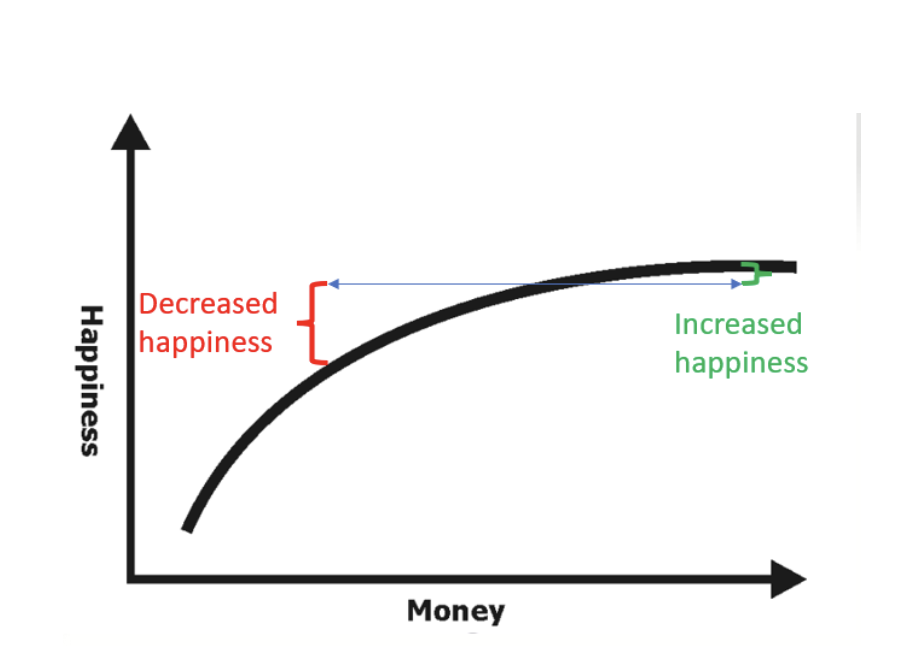

Maslow’s Hierarchy of Needs provides a nice framework. While money may not buy happiness, lack of money will buy misery if you don’t have enough to meet physiological needs like food and shelter, or a safe environment. But when those needs are met, spending money on those social, esteem, and self-actualization components may be the key to increased happiness.

Applying Maslow’s framework with prospect theory from the research of Daniel Kahneman and Amos Tversky (getting more pain from losing an amount than pleasure from gaining the same amount) is illustrated below. The marginal increase in happiness declines as wealth increases, but losing money always hurts more than making the same amount provides pleasure.

Investing and Happiness

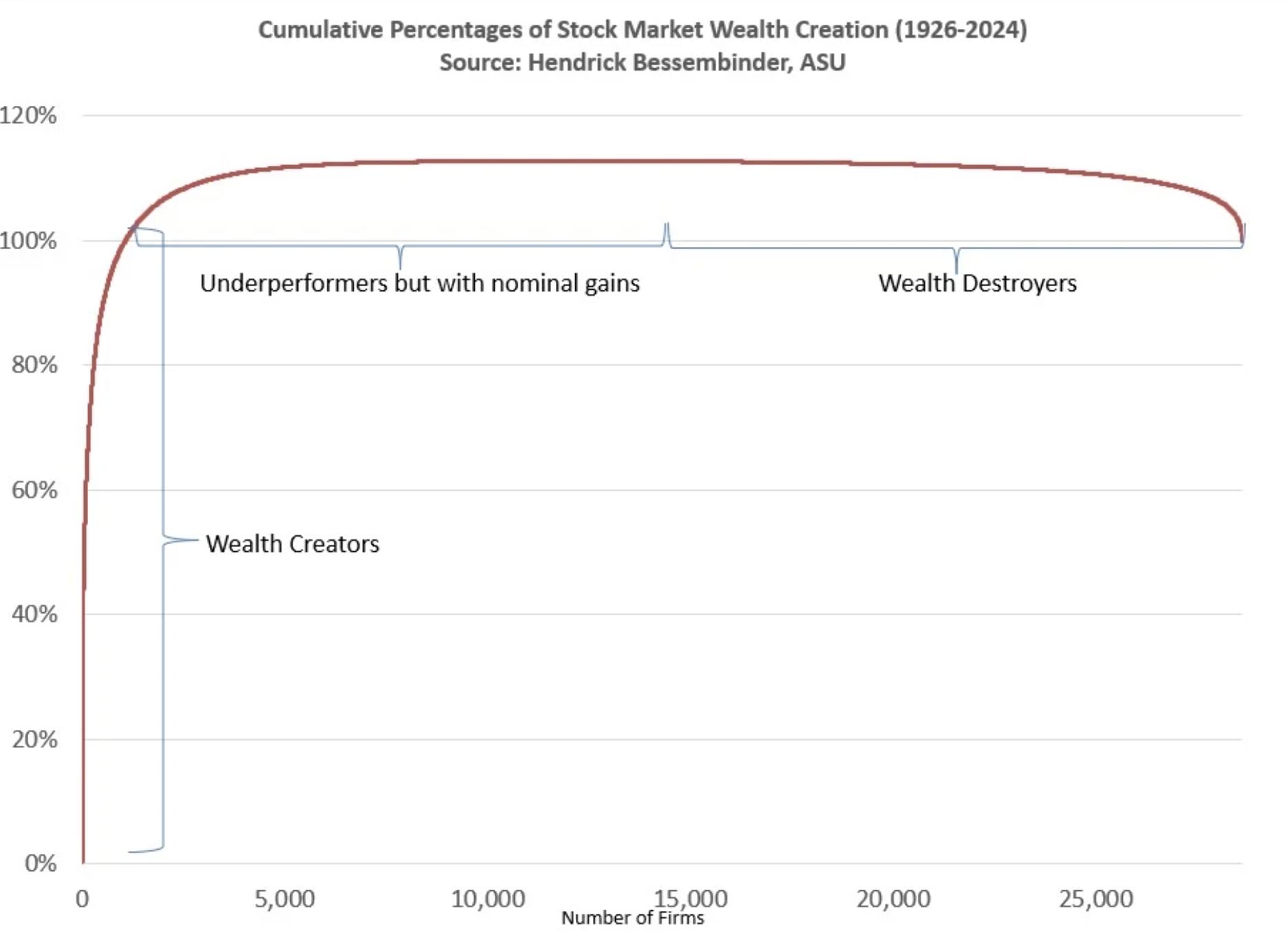

Investing in Treasury Bills is very unlikely to grow wealth faster than inflation. But do stocks outperform Treasury Bills? Hendrik Bessembinder found that 96% of stocks perform on average the same as a Treasury Bill. Below is a distribution of stock returns he sent me.

As discussed earlier, we invest to grow our money faster than inflation so we have the freedom to pursue greater happiness. Jim Cramer’s new book, “How to Make Money in Any Market,” claims that he shows you how to get rich by understanding the market and investing in the right growth and income stocks — ones that he can help you identify.

Now, picking the right 4% of stocks that create wealth would succeed in making one rich. Yet there is very little evidence Cramer has been a good stock picker and significant evidence of underperformance versus a broad index fund. The stock market creates real wealth, but most individual stocks (51.6%) actually lose wealth and don’t even keep up with the Treasury Bill. A recent Reddit post details how Cramer cost the poster ten years of work and significantly underperformed against the S&P 500 and funds tracking it during that period.

The implications on investing and happiness are as follows:

Given:

- Statistically, a portfolio of even a few dozen stocks is likely to underperform the market.

- Relative wealth matters more than absolute wealth (we must have more than our friends and neighbors).

- We get more pain from losing money than pleasure from making the same amount. That is especially true if we have little wealth and can no longer meet our physiological and safety needs (those Jordan Belfort preyed on).

Then:

My hypothesis is that stock picking (using Cramer’s or any method) is far more likely to make you far more unhappy than owning the whole market. I ran my hypothesis by Dr. Gilbert, who responded:

“It makes you happy when you win (and you rarely win), and it makes you very unhappy when you lose (and you usually lose).”

This hypothesis can be applied to more than just stock picking. Morningstar research has shown us two things regarding fund performance:

Conclusion

While a broad index fund is more likely to increase wealth, it’s also more likely to increase happiness because your wealth relative to others will likely increase faster. You just have to remember that the neighbor bragging about their brilliant stock pick isn’t mentioning their losers. Indexers have a much higher likelihood of becoming financially independent sooner than active investors.

Daniel Gilbert’s work shows that, contrary to popular belief, having more freedom and choice can lead to less satisfaction. When a choice is final, we tend to find reasons to love it; when we have the option to change our minds, we remain critical and less satisfied.

Don’t make the mistake I did. Have a plan for what you will do with the rest of your life by examining what makes you happy.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Allan Roth

The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.