The tech sector’s once relentless push higher in the US stock market has turned into a topsy-turvy ride, forcing investors to seek calmer waters where stodgy, old-economy companies ply their trades.

That’s meant diverting cash from the artificial intelligence trade, where it’s gotten more difficult to discern winners from losers, and into areas like materials and energy producers, or makers of consumer goods.

Some of the non-tech stocks that have helped push their sectors higher since late October include Southwest Airlines Co., which is up 72%, lithium producer Albemarle Corp. (71%), Moderna Inc. (65%) and logistics giant CH Robinson Worldwide Inc. (56%).

The S&P 500 Index, stripped of technology, can return 6% by May, based on the direction of its 20-day moving average, JC O’Hara, chief technical strategist at Roth, said by phone. He said he’s not negative on the technology sector but “giving a round of applause” to the sectors that are contributing to broadening gains.

“Tech is so big that if you just reduce tech by a smidgen, and you take that money and put it into other areas of the market, which are so much smaller, those areas are gonna explode,” O’Hara said.

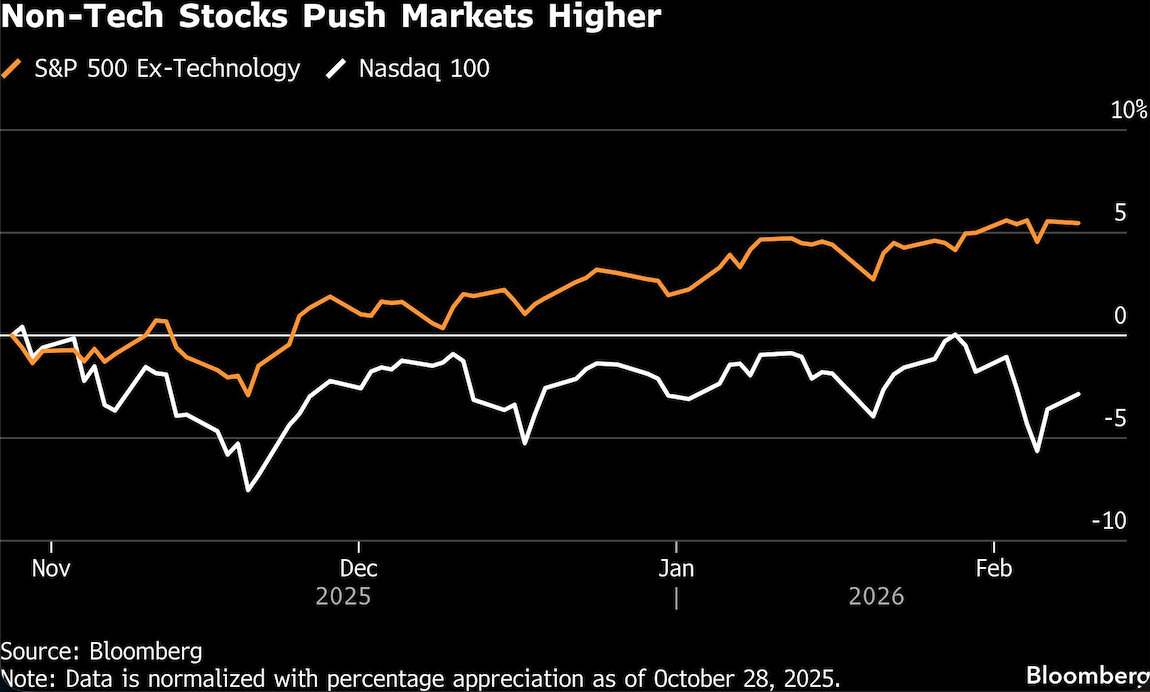

That view has been gaining traction on Wall Street all year, though it came in for a bit of a reconsideration last week when a tech-led selloff spread to all corners of the market. The computer and software companies then drove Friday’s rebound, and outperformed again Monday. The Nasdaq 100 Index traded up 0.1% at 9:34 a.m. in New York, while the S&P 500 was up 0.2%.

But it’s that volatility that has strategists advising investors look for alternatives. After three years of tech outperformance, positioning has become so skewed toward the group that the prospects for non-tech industries have improved.

“Broadening is just beginning,” Savita Subramanian, head of US equity and quantitative strategy at Bank of America Corp., said in a Monday note. The average S&P 500 stock, outside of the Magnificent Seven mega-cap tech names, is held at a rate of 20% below its weighting in the index and owned by a “paltry” 10% of funds on average, according to the bank.

“Years of narrow, large cap leadership have forced active managers into mega caps, leaving the average stock out in the cold,” Subramanian said. By comparison, the Magnificent Seven names are held by up to 90% of funds and all but Tesla Inc. and Apple Inc. are overweight. She said those names look “particularly vulnerable” as a rotation into other corners of the market are funded by selling in mega-cap tech stocks.

A look at earnings expectations support the thesis that leadership will broaden. The median stock in the Russell 3000 is expected to grow earnings by 11% this year, which is the strongest growth in four years, according to data from Morgan Stanley.

That would continue a trend in place since November. The S&P 500 Information Technology sector has slipped by 6.7% since Oct. 28, while the energy sector has climbed by 23%, the materials sector is up 17% and consumer staples and industrials have both risen by 12%. More broadly, the S&P 500 has climbed 1.1% since the tech peak.

“A big movement right now is not away from tech but it’s answering, ‘how do you diversify a portfolio that is so heavily weighted in tech?’ and that’s by going back to the old economy-type stocks,” Roth’s O’Hara said.

The move from a narrow set of tech stocks into a broader range of industrials and other sectors has helped the Dow Jones Industrial Average rise above 50,000 points, he said.

And there remains concern that the technology sector will languish, as declines by mega-cap tech names Amazon.com Inc., Microsoft Corp., Alphabet Inc. and Meta Platforms Inc. dragged on the Nasdaq 100 Index and funds tracking its performance, like the Invesco QQQ Trust.

“I fully expect QQQ to continue to underperform other areas of the market (small caps, equal-weight, value) as we continue to see money come out of these still ‘crowded’ names after years of outperformance,” Jeffrey Jacobson, head of derivative strategy at 22V Research LLC, said in a Monday note.

Jacobson said that an equal-weighted basket of those four tech giants just broke below its November lows after Alphabet and Microsoft both unveiled “aggressive” capital expenditure plans that weighed on their shares. He recommends investors add put spread collars in QQQ as a large-cap sector hedge, “especially after the 2% bounce we saw on Friday.”

Strategists still encourage investors to hold tech stocks — just not as much as they held through the first half of 2025.

“I don’t think you need to be overweight anymore,” Roth’s O’Hara said. “While it’s still good to have tech, you’re seeing other areas of the market that could be playing off the strength of this industrial revival.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Geoffrey Morgan