Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Executive Summary

The 2026 investment environment is defined by an unusual but constructive combination: global growth that remains resilient, inflation that is moderating but not disappearing, and policy settings that are shifting away from restriction toward flexibility. After several years dominated by macro shocks, markets are transitioning into a phase where dispersion, selectivity, and disciplined portfolio construction matter more than broad directional bets.

Our central outlook for 2026 is one of extended but aging expansion. Growth is sturdy enough to support earnings and cash flow, yet uneven across regions and sectors. Inflation continues to normalize, but labor market dynamics and structural supply constraints argue against a rapid return to pre-pandemic norms. Monetary policy may ease further early in the year before pausing as central banks balance progress on inflation against signs of re-acceleration in growth.

For investors, this environment favors balance over extremes. We believe equity markets can continue to advance, but leadership should broaden and volatility may be likely to rise alongside returns. Fixed income, after a long period of diminished relevance, has reasserted itself as a meaningful source of income and diversification. Across asset classes, the opportunity set is widening — rewarding patience, selectivity, and risk awareness.

Key themes for 2026

- Inflation moderates, but remains structurally sticky

- Equity leadership broadens beyond narrow concentration

- Income and carry regain strategic importance

2025 in Review: A Transition Year Across Regions

In 2025, markets rewarded investors who remained disciplined amid persistent uncertainty. Despite widespread concerns about recession and trade policy, economic activity proved resilient, earnings held up better than expected, and financial conditions eased as inflation pressures receded in the second half of the year.

United States

The U.S. economy once again exceeded cautious expectations in 2025. Real GDP growth remained solid, supported by consumer spending, strong corporate balance sheets, and continued capital investment tied to data center buildout and reshoring initiatives. While job growth slowed materially through the year, household balance sheets and wage growth helped cushion consumption. Inflation expectations decelerated meaningfully from its peak in April, allowing the Federal Reserve to pivot from restrictive policy toward the early stages of easing late in the year.

Europe

Europe experienced a stabilization year rather than a rebound. Growth remained modest, constrained by weaker industrial activity and lagged effects of prior tightening. However, easing inflation, improving credit conditions, and selective fiscal support helped prevent a deeper slowdown, and allowed central banks to consider stimulative policies. Sentiment improved gradually as energy prices remained contained and real incomes began to recover.

Japan

Japan stood out as a structural story rather than a cyclical one in 2025. Economic growth was modest, but corporate reforms, improved governance, and rising shareholder returns drove strong investor interest. Companies continued to deploy excess cash toward dividends, buybacks, and productivity-enhancing investment. A weak yen for much of the year supported earnings for exporters, while domestic demand showed gradual improvement.

Emerging Markets

Emerging markets delivered mixed but improving results in 2025. Disinflation across many EM economies allowed central banks to begin easing earlier than in developed markets, supporting domestic demand. Growth was led by countries with exposure to AI and the data center buildout, while export-oriented economies navigated uneven global trade conditions.

Equity Market Performance in 2025

Global equity markets posted positive returns in 2025; however, leadership was concentrated overseas. As of December 31, 2025, the S&P 500 Index returned 17.9% (total return), while the MSCI Europe Index returned 36.3%, the MSCI Japan Index returned 25.1%, and the MSCI Emerging Markets Index returned 34.3%.1

Bond Market Performance in 2025

The U.S. 10-year Treasury yield exhibited considerable volatility throughout 2025, starting the year at 4.60% in early January and ending at 4.17% on December 31. The yield reached its lowest point in mid-October, at approximately 3.98%, before climbing back above 4% to close the year. This movement reflected shifting expectations around Federal Reserve policy and inflation dynamics.2

Corporates remained solid, with investment-grade bonds returning 7.3% and high yield bonds an even stronger 8.6%.3

Market Dynamics

Inflation

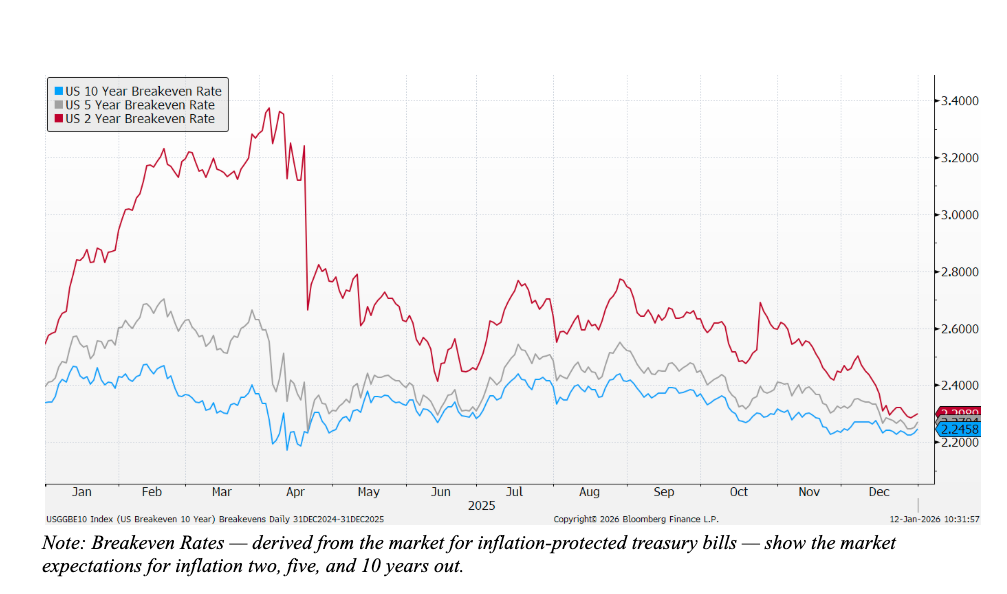

Core inflation fell from 3.3% to 2.6%, crossing the key 3% threshold.4 Breakeven rates, a market-based measure of inflation expectations, peaked during the run-up to the trade policy announcements in April, but fell steadily for the rest of the year, ending lower than where they started. While headlines and commentary have been focused on affordability, the actual data and expectations for inflation have been muted.

As noted in our 2025 Outlook and much of our other macroeconomic work, when core inflation settles below 3%:

- The Federal Reserve begins to focus more on economic growth and employment than inflation, and there is a subsequent resumption of rate cuts.

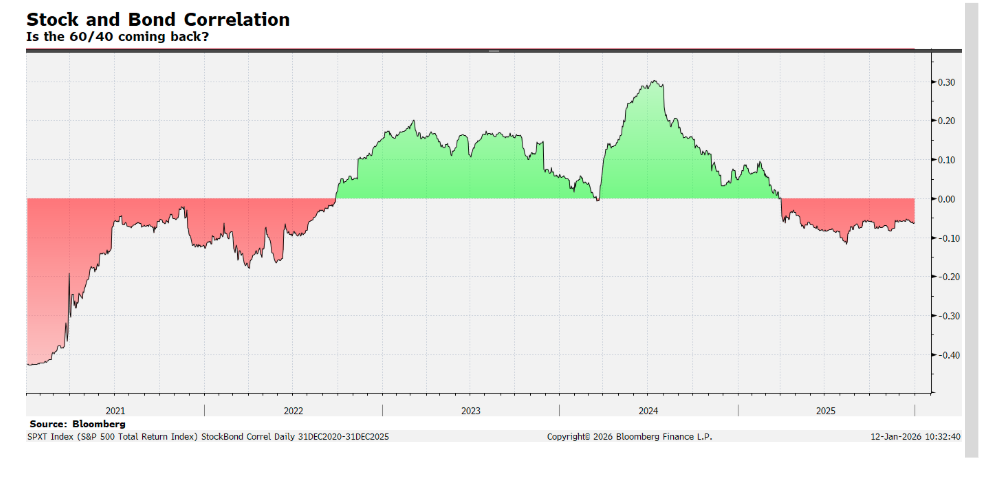

- Returns to stocks and bonds move in opposite directions instead of moving together.

This is indeed what we saw in 2025, putting the diversification benefit of the traditional 60/40 back in play.

The Dollar

Lower inflation and three rate cuts by the Federal Reserve weighed on the dollar, with the trade-weighted dollar index falling about 7.5% in 2025. Long a headwind to returns for international markets, non-U.S. equities and bonds around the world led markets, with almost all equity markets outside the U.S. up more than 25% and emerging market bonds providing double-digit returns.5

Momentum

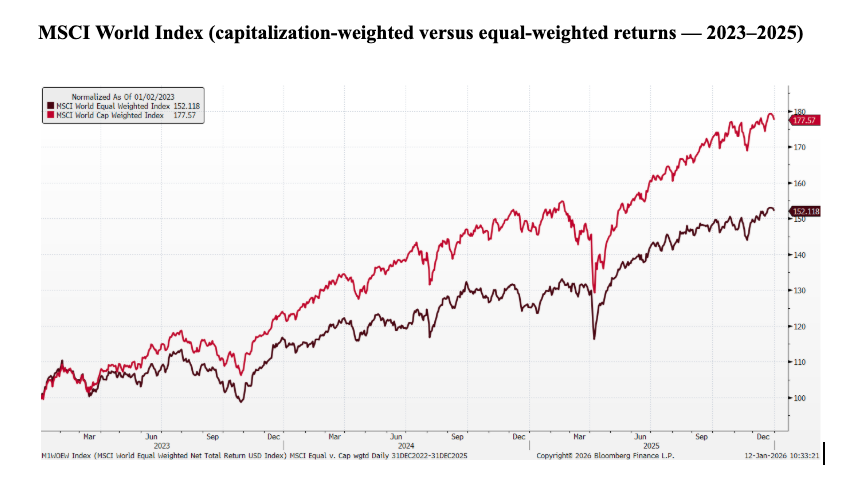

One of the big themes of the 2025 Outlook was the role of momentum in equity markets, and whether stocks that had outperformed the year before would continue to outperform. The report quoted a fall in inflation and the Fed refocusing on the economy as two catalysts of the momentum cycle fading, and it is fair to say momentum as a style of equity investment did execute a “soft landing” in 2025. While large-growth stocks still outperformed in 2025, the overall returns to stocks that had performed well in the past were in line with the broader market, fading after the trade policy uncertainty of April.6

Global Outlook: From Concentration to Broadening Opportunity

The defining shift as we enter 2026 is not the end of growth, nor a dramatic policy pivot — it is the easing of inflation fears. As inflation moderates and tail risks recede, financial conditions have become more accommodative, even in the absence of aggressive monetary easing. This shift has meaningful implications for markets, particularly for leadership.

Over the past several years, equity returns were driven by a narrow group of large-cap growth stocks, reflecting scarcity of growth, abundant liquidity, and heightened macro uncertainty. As inflation pressures ease and policy becomes more flexible, the investment environment is evolving. Broader participation across regions, sectors, and market capitalizations may be increasingly likely.

Growth and the Cycle: Extension, Not Acceleration

We expect global growth to remain sturdy but uneven in 2026. The U.S. continues to grow above trend, Europe is stabilizing, and Japan benefits from structural reform momentum. Emerging markets operate in a more supportive macro environment as local inflation and rates decline.

We don’t see this as a fast-growth environment that consistently favors market leaders. Instead, it may create more room for cyclical areas and companies with improving profits — dynamics that can show up more in smaller-cap and non-U.S. equities.

Inflation: From Constraint to Catalyst

Inflation remains above pre-pandemic norms, but its trajectory — not its absolute level — is what matters most for markets. Goods inflation has normalized, services inflation is cooling gradually, and longer-term inflation expectations have declined. This has reduced the need for restrictive policy and lowered the probability of renewed tightening.

As inflation fears fade, the penalty for taking risks may decline, and capital may become more willing to move beyond a narrow set of large market leaders.

Financial Conditions: Accommodative Without Excess

Financial conditions have eased meaningfully despite policy rates that remain restrictive by historical standards. Lower volatility, improved credit availability, and supportive equity markets are providing an effective easing impulse to the global economy.

Historically, periods of improving financial conditions have often been associated with relative strength in:

- Smaller-cap equities, which are more sensitive to domestic growth and financing conditions

- International markets, where valuations are lower and earnings leverage is higher

- Emerging markets, which benefit disproportionately from lower inflation volatility and a weaker U.S. dollar

Importantly, accommodative financial conditions don’t necessarily require rapid rate cuts. Even a steady policy backdrop can help broaden market participation over time.

Equity Markets: Broadening Opportunity, Higher Dispersion

Equity markets enter 2026 with elevated valuations in select areas, reflecting optimism around earnings growth, technological investment, and easing policy. While this creates sensitivity to macro surprises, it does not preclude further gains.

Key Equity Themes

- Broadening leadership: Market concentration remains high, but earnings growth is spreading across sectors and regions. This market action favors markets with more cyclical exposure, such as Europe and Emerging Markets.

- Earnings durability matters: In a less liquidity-driven market, fundamentals regain influence.

- Volatility rises with opportunity: Periodic pullbacks may be likely, even within a constructive trend.

Regional Perspectives

- United States: The U.S. remains the primary engine of global earnings growth, supported by innovation, capital investment, and relatively favorable financial conditions. Valuations are demanding, reinforcing the importance of selectivity. The U.S. is primarily a technology market now, and insomuch as markets become more cyclically driven, relative performance may weaken.

- Europe: Improving growth expectations, fiscal support, and lower valuations create scope for upside surprises, particularly if sentiment remains cautious.

- Japan: Structural reform, improved governance, rising shareholder returns, and improving return on equity underpin a multiyear investment case rather than a short-term cyclical trade.

- Emerging Markets: While emerging markets are dominated by large technology stocks from North Asia, they still retain a considerable cyclical component and stand to benefit from improved financial conditions and better economic growth.

Active equity strategies may be well-positioned in this environment where dispersion and differentiation can create opportunities beyond index-level exposure.

Fixed Income: Income and Stability in a Late-Cycle Environment

The fixed income environment entering 2026 reflects a market that has navigated a series of macro, policy, and credit-related disruptions while remaining broadly supported. The fourth quarter of 2025 began with a period of heightened risk aversion before stabilizing and recovering into year-end, leaving risk assets near their annual highs.

The early quarter volatility followed a convergence of factors, including a prolonged U.S. government shutdown, renewed geopolitical tensions, and credit stress tied to notable corporate defaults. During this period, markets also began to closely assess the scale and financing requirements associated with large investments in AI infrastructure, contributing to elevated volatility across both risk assets and interest rates.

Interest rates declined during the initial risk-off phase, then fluctuated within a relatively narrow range before ending the year close to where they began. The government shutdown disrupted the flow of economic data, complicating market interpretation of inflation and labor trends and adding complexity to the Federal Reserve’s policy decisions at a sensitive point in the easing cycle. While delayed data releases are now becoming available, revisions and distortions may persist.

Fixed Income Positioning

With core inflation stable, fixed income is generally best positioned as a source of income, diversification, and portfolio stability, rather than a vehicle for outsized duration or spread-driven returns. With economic growth remaining resilient but risks becoming more balanced, fixed income returns may be driven primarily by income rather than price appreciation.

Key considerations include:

- Maintaining core fixed income exposure to help manage portfolio volatility

- Focusing on intermediate duration, which may provide income while retaining flexibility amid rate uncertainty

- Taking a selective approach to credit, emphasizing issuer quality and fundamentals

While credit conditions remain generally supportive, periodic volatility related to refinancing activity, financing needs, or shifts in investor sentiment remains possible, reinforcing the case for disciplined positioning.

Role in Portfolios

Early in 2026, fixed income continues to play an important role in diversified portfolios. In an environment characterized by solid growth, moderating inflation, and evolving monetary policy, bonds may provide a combination of income and diversification that can help support portfolio outcomes across a range of economic scenarios.

Portfolio Construction: Balance Over Bravado

The defining feature of 2026 is balance. Neither recession nor overheating appears imminent, but risks remain two-sided.

The muted inflation data may indicate a return to stock versus bond diversification, but any significant uptick will tie stock and bond returns together again. We believe the use of alternatives to thoughtfully diversify portfolios is still prudent, and investors should be thoughtful when using private investments as an “alternative.” Private equity is still equity, and private credit is still credit — so these exposures can remain economically sensitive and may be correlated with public markets, particularly during periods of stress. Private investments may also involve higher fees and expenses, limited liquidity, less frequent valuations, and additional complexity.

Risks

While our base case is constructive, several risks may warrant monitoring:

- A resurgence of inflation driven by supply shocks or policy changes

- A sharper-than-expected labor market downturn

- Policy missteps that destabilize financial conditions

- Geopolitical developments disrupting trade or energy markets

- These risks may reinforce the importance of diversification and flexibility rather than wholesale shifts in positioning.

Conclusion: A Year for Disciplined Investors

While 2026 may be unlikely to deliver the simplicity of a one-directional market, it may, it may offer something more durable: a widening opportunity set across asset classes for disciplined, long-term investors.

As markets move beyond crisis-driven dynamics, the value of thoughtful portfolio construction, active risk management, and income generation comes back into focus. For advisors and investors willing to embrace balance and selectivity, 2026 presents a constructive — if more nuanced — investment landscape.

Endnotes

1Source: S&P Dow Jones Indices for S&P 500 Index total return and MSCI, using the MSCI USA index for U.S. returns, MSCI Europe index for European returns, MSCI Japan index for Japanese returns, and the MSCI Emerging Markets index for Emerging Market returns as of 12/31/2025.

2Source: Bloomberg

3Source: Bloomberg

4Source: Bloomberg

5Source: Bloomberg

6Some of the relative returns in this chart may be due to different weighting schemes, but momentum returns were certainly lower than in 2024.

Important InformationThis material is for informational purposes only and is not intended as investment advice or a recommendation to buy or sell any security. Views and opinions are those of Shelton Capital Management as of the date of publication and are subject to change without notice. Forecasts, estimates, and forward-looking statements are based on assumptions and are not guaranteed. Past performance is not indicative of future results. Indexes are unmanaged and not available for direct investment.

Derek Izuel is chief investment officer of Shelton Capital Management.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Derek Izuel

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.