Once upon a time, being a pension fund manager was a relatively straightforward job. The objective is simple: Invest the pension’s assets in such a way that its beneficiaries will be paid.

If you play it safe and the fund doesn’t generate sufficient returns, it will require more contributions, often from taxpayers. But if you take too much risk, it could also go wrong and leave the fund without enough money. The task requires balancing risk and reward.

OK, so maybe it was never easy — but as I said, the objective is clear and there are some simple truths that have long served as the industry’s guiding principles. One is that US bonds are the world’s safest asset. Another is that private investments offer higher returns and less volatility. And a third is that the so-called ESG strategy is the best way to manage long-term climate risks.

The last five years have raised doubts about each of these beliefs. The world is now entering a new era not just for pensions, but for institutional investing itself.

Consider three recent events that have rocked the pension-geek world (and we do not excite easily) in the last few months. These stories can’t be brushed off as market blips or the anomalous activities of a few overly political pension funds. Each points to a big shift in the conventional wisdom in pension investing, in both the big European funds and the state and municipal pension funds in the US that followed a similar strategy.

Potentially the biggest news is that the Danish pension fund AkademikerPension and the Dutch pension fund ABP are selling their holdings of US Treasuries, while the Swedish pension Alecta has been dumping Treasuries for the last year. They all say they are concerned about new geopolitical risks and have less confidence in Treasuries as the global risk-free asset.

These Scandinavian moves may be more politically motivated than prudent. US bonds are still, relative to any other option, the most liquid and safe asset around. No other sovereign market can match them. Commodities such as gold or silver don’t offer duration and are very volatile, which means they don’t offer a great hedge for pensions (or any long-term liability).

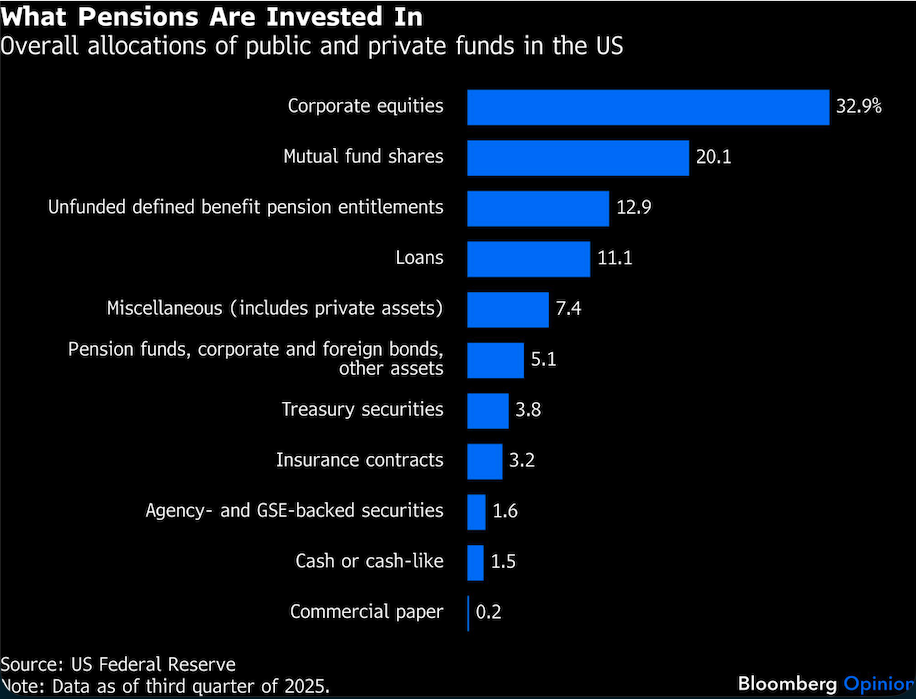

Also worth noting: US Treasuries have held up pretty well overall, despite extreme chaos and the possibility of a new economic world order. American pension funds slightly increased their exposure to Treasuries in the last year.

Still, even if Treasuries are just the least dirty shirt on the floor, the Scandinavians are right to be concerned. Sovereign bonds are not offering the same low-risk hedge as they used to, and any acknowledgement of that fact is significant. Mounting debt and the possibility of inflation do pose a serious long-term risk to US bond returns and the dollar.

In the future, hedging will probably require holding a variety of bonds, or just being more thoughtful about diversification. If US Treasuries are no longer seen as risk-free, hedging not only becomes much harder, but valuing anything becomes much more complicated and arbitrary.

Another story is the underperformance and illiquidity of private investments . For a while, private assets seemed like the answer to underfunded pension funds’ problems. The biggest funds have half a trillion dollars in private exposure — some even doubled their exposure in the last decade. Private investments promised higher returns, and because they can’t be marked to market, lower volatility.

This promise of higher returns seemed reasonable. After all, these funds had experts picking the best companies and getting involved in their management, and meanwhile the risk of illiquidity promised the reward of higher returns.

But as these investments have matured, some pensions have discovered they did not get the returns they were promised — if they can get their money at all. It is not just pensions; university endowments, which also went heavy into private assets, would have done better with a 70/30 public equity/bond split. Many pensions are still in private assets, but if they follow the lead of endowments, they may be reducing their exposure soon, too.

One final news item: Last year, the Dutch pension fund PME pulled its money — about $5.9 billion — from BlackRock because it the investment firm was no longer complying with ESG principles. Many pensions in America have also pulled back from ESG investing, under which funds invest only in companies with acceptable environmental, social and governance standards.

ESG seemed to promise the best of all worlds: It would avoid companies that might fare poorly as the climate changes while earning higher returns. In practice, the question of which companies are “ESG compliant” tends to be political and arbitrary — which is hardly surprising, since the markets’ reaction to climate change is still a big unknown. ESG investors were also constrained by the reality that a limited portfolio tends to underperform one with fewer restrictions.

Some pension funds in Europe still choose an ESG investing strategy. Maybe that’s because their managers are more certain about the market impact of climate change, or because they’re more worried about the politics of abandoning ESG. In any case, in other countries, an aging population means fund managers need to get the highest return possible.

The bottom line is that, as the geopolitical world becomes more uncertain and the global economic order more unstable, what “responsible investing” means is not so clear anymore.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Allison Schrager