Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Since the release of OpenAI’s Flagship Chat GPT Large Language Model (LLM) in November of 2022, there has been a deluge of investment into AI by various big tech and semiconductor companies including Alphabet, Microsoft, Nvidia, Apple, Meta, Amazon, and Tesla. The stock price of these big tech companies — colloquially known as the Magnificent Seven — have soared to unprecedented highs. These companies have significantly increased their capital expenditures into building out data centers and manufacturing GPUs to power LLMs such as ChatGPT, Llama, and Google Gemini.

The massive increase in capital expenditures by these companies has largely lifted investor optimism and dragged the market out of its 2022 lows. The unprecedented surge among the Magnificent Seven tech-related stocks has also led investors and the general public to compare the current state of the stock market to the dot-com bubble. That phenomenon resulted in the exponential rise in the stock prices of companies such as Cisco, Amazon, Yahoo!, and Microsoft. Cisco, Amazon, and Microsoft, in particular, are still around as publicly traded companies and have well-diversified sets of revenue streams, products, and services.

Even if AI products and services fail to generate any tangible value through an increase in worker efficiency and productivity or through improvements in businesses’ bottom lines, companies such as Microsoft and Amazon are still well-positioned to thrive due to their well-diversified set of products and services. The circular investing phenomenon that is currently occurring among the Magnificent Seven companies is very similar to the Japanese Keiretsu concept. Under this business model, companies with interlocking business relationships and shareholders dominate a country’s economy.

For example, in Q1 of 2025, Amazon’s Cloud Division (AWS) acquired 822,000 shares of AMD, since AWS uses AMD’s CPU and GPU processors to run AI workloads. The questions that are on the minds of many investors and tech executives are as follows:

- Are we currently in an AI stock market bubble?

- Is this a rational bubble?

- Does the circular investing among the Magnificent Seven companies prove that we are in an AI Bubble?

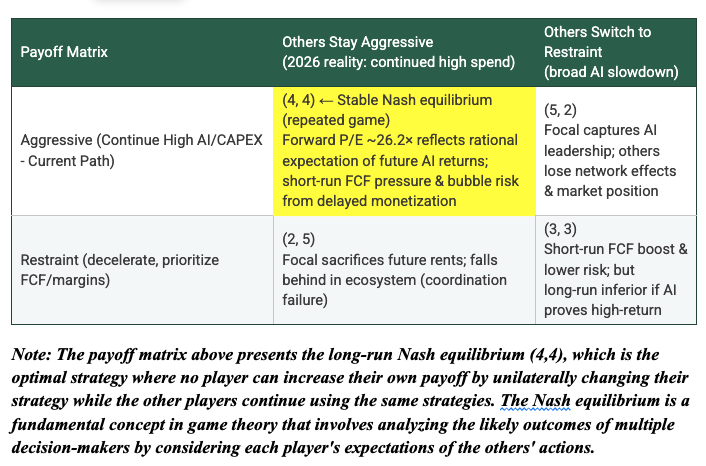

The Payoff Matrix

To answer those questions, we designed a payoff matrix that contains four plausible scenarios that represent the decisions that the Magnificent Seven companies involved in the AI arms race are most likely to make. The payoff matrix also contains the Nash equilibrium, which is the optimal decision that each of these seven companies should make in order to further their own financial gains and generate consistent returns for their shareholders.

It uses fundamental data such as each company’s earnings per share (EPS), free cash flow (FCF), and median forward price-earnings (PE) ratio to calculate the Nash equilibrium. The payoffs for each of the four strategies or decisions were assigned on a 1–5 scale, where 5 represents the best long-term shareholder value. The payoff matrix seeks to answer the question of whether the Magnificent Seven companies are investing in each other to increase their revenue streams or in order to prop up their valuations.

From a game-theorist perspective, it would be in the best interests of the Magnificent Seven companies to keep investing in each other and buying each other’s products and services, such as AMD and Nvidia GPUs, as well as AWS Cloud Services, in order to avoid falling behind and maintain consistent revenue growth. This leads us to the question of when this circular investing cycle between these companies ends, and if there is a scenario where it is in the best interest of Nvidia or Alphabet to defect due to the launch or discovery of a new superior product or technology.

In the long run, circular investing among the Magnificent Seven companies has a high probability of becoming a bubble. Many companies, such as Microsoft and Alphabet, are reporting expected future revenue from their AI capital expenditures (capex). Investors could easily become anxious and begin questioning the pace of capex spending by these companies and whether they will ever see returns from current and past investments in building data centers and designing GPUs to power large language models (LLMs). Should this come to pass, it could prompt companies like Meta or Alphabet to slow their capex spending and reevaluate their past, current, and future capex decisions.

Artificial Superintelligence

Additionally, the economic theory of creative destruction suggests that if a newer technology or innovation emerges that provides more tangible economic benefits at a lower cost — such as increased worker output and higher productivity — it could render various AI products, including LLMs, obsolete. We are currently witnessing a variant of this creative destruction scenario.

Many of the Magnificent Seven companies, such as Meta, Alphabet, and Microsoft, are singularly focused on developing AI products and services, including large language models (LLMs) with artificial superintelligence capabilities. In layman's terms, this means that the AI model can outperform human thinking across all fields. The first step toward achieving artificial superintelligence is reaching artificial general intelligence (AGI), which refers to an AI model's ability to replicate human thinking by understanding, learning, and applying knowledge across any task that a human can comprehend.

This raises the question: What will happen if Google or Meta fail to develop an LLM that possesses either AGI or artificial superintelligence? Would this imply that Meta and Google have wasted billions of dollars in capital expenditures on products that will not generate tangible returns in income, productivity, or efficiency over the long term?

Furthermore, it also prompts us to consider whether the Magnificent Seven companies' singular focus on developing an LLM with both AGI and artificial superintelligence is distracting them from further advancing other products and services that currently generate consistent revenue, such as cloud computing, software, and advertising. Many of these companies’ existing products and services already incorporate AI elements to enhance user efficiency. For example, enterprise users of Microsoft Office 365 can ask Co-Pilot to summarize an email or edit a Word document to improve its flow.

A ‘Rational’ Bubble?

On the other hand, many investors may still believe that the circular investing among the Magnificent Seven companies does not exhibit the classic features of a bubble. Rather, it presents itself as a rational bubble with the potential to revolutionize every facet of our daily lives, ranging from the way we work to our personal lives. They may be right, since many Magnificent Seven stocks such as Microsoft and Amazon do not currently have elevated P/E ratios relative to their respective P/E ratios during the Dotcom Bubble period. Moreover, Microsoft, in particular, is positioned to do very well financially in the current evolving economic and technological landscape. It has a first-mover advantage and was one of the first companies to invest in OpenAI in 2019.

Additionally, investors are starting to heavily scrutinize the pace of AI capex spending by big tech companies. This, in turn, is forcing management at these companies to be more disciplined in the execution of their AI strategies while slowing the pace of capital allocations towards the buildout of AI infrastructure. Capex spending by big tech companies is still elevated and exceeds estimates.

However, management teams at these companies are becoming more cautious and are focused on efficiently allocating their resources towards projects related to AI inference and Agentic AI. These technologies have greater absolute ROI and long-term revenue potential than solely focusing on developing more sophisticated LLMs. More specifically, AI has the potential to transform industries ranging from healthcare to finance by automating redundant administrative tasks such as health insurance billing, providing a patient's after-visit summary, building discounted cash flow models, and calculating financial ratios.

In the short run, ideally the Magnificent Seven companies will engage in the follow-the-leader strategy in order to maintain and grow their market share, while also expanding their profit margins and increasing returns for their shareholders through the rising stock valuations of all the companies involved in the AI arms race. That said, the circular financing loops among the Magnificent Seven companies may risk the creation of a bubble if investors begin to further bid up the prices of these companies’ stocks which will subsequently lead to the stock prices of these companies becoming detached from market fundamentals.

Additionally, for the circular financing loops among the Magnificent Seven Companies to remain intact these companies need to deliver on their AI visions through the launch of new AI products and services that can produce consistent income while also increasing worker productivity. If these AI companies are unable to deliver on their AI Visions, investors and stock analysts may punish them through selling their stock and cutting the stocks’ price targets.

Dr. Derek Horstmeyer is a professor of finance at George Mason University. His research focuses on ETF performance and corporate governance. He also runs the Montano Student Managed Investment Fund.

Akarsh Deiva is currently pursuing a Master of Science in Business Analytics (MSBA) at George Mason University and works as a Data Scientist at the Centers for Medicare and Medicaid Services (CMS). Prior to this role, he served as a Program Analyst at the Office of the Comptroller of the Currency (OCC) and the Department of Defense – Office of the Inspector General (DoD – OIG). While at the DoD – OIG, he conducted evaluations of various Department of Defense programs.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Derek Horstmeyer, Akarsh Deiva

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.