What Financial Advisors Need to Know About 529 Plans

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

July 4, 2025, celebrated independence in more ways than one. In addition to commemorating the split of thirteen American colonies from Great Britain, the federal holiday marked the legislative passage of the nearly 900 pages of the One Big Beautiful Bill Act (OBBBA). Pursuant to the provisions of what is known as Public Law No: 119-21, individuals enjoy enlarged benefits in the form of increased distributions from a 529 plan and the kinds of expenses deemed eligible for tax-free withdrawals. No longer mainly focused on college-bound students, post-reform 529 plans can be used to help beneficiaries repay student debt, finance trade school tuition, pay for professional licenses and certifications, or purchase non-tuition expenses such as curriculum materials.

ABCs of 529 Plans

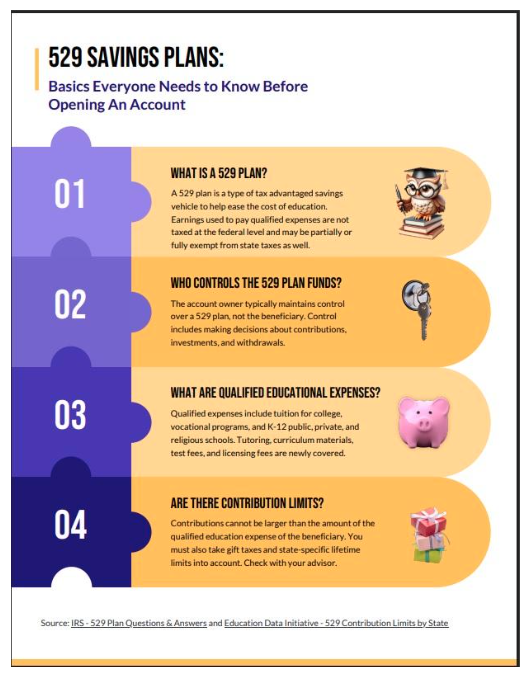

A 529 plan is a tax-advantaged plan, operated by a state or educational institution, and created for the express purpose of saving to pay for education. Earnings are not subject to federal taxation. Depending on where you live and your use of a state-operated 529 plan versus a private plan, your earnings may be exempt at the state level as well.

The savings type of 529 plan is offered by nearly every state and considered more flexible than the second type — a prepaid tuition plan. With the former, your contributions grow tax-deferred, assuming the underlying investments, usually shares in different types of funds, perform well. Some of these 529 savings plans offer age-based portfolios that adjust the asset allocation mix to lower risk as the beneficiary gets closer to requiring money. Contributions can be manual or automatic. At the end of 2024, 38% of 529 plans were receiving automatic contributions. Maximum limits for the savings type of 529 plan are established by each state that offers them. Existing limits range from $235,000 (Georgia) to $589,650 (Wisconsin). States like New York and Pennsylvania offer multiple 529 plans.

You can find summary information by visiting online resources such as “Find My State’s 529 Plan,” published by the 529 College Savings Plan Network, an affiliate of the National Association of State Treasurers. Morningstar and Saving for College publish ratings for many 529 savings plans. These consider ease of use, fee levels, investment selection and monitoring, oversight, and performance, among other criteria. According to Morningstar’s methodology explanation, their ratings reflect an analysis of “investment quality” and the “rigor and resilience of the underlying investment process.” Saving for College employs a weighted approach that yields a score between one to five graduation caps, with five being the “most attractive.”

529 Plan Use Remains Relatively Low

Named after section 529 of the Internal Revenue code, this qualified tuition program turns 30 years old in 2026. Notwithstanding the 2025-2026 expansion of 529 plan rules, designed to assist millions more individuals, the total number of 529 plans and assets is surprisingly low. A lack of knowledge seems to be the major culprit. Savers won’t embrace what they don’t understand.

According to recent statistics compiled by Melanie Hanson, senior editor with the Education Data Initiative, there were nearly 17 million active 529 accounts in mid-2024 with an average account balance of $30,295 and a nationwide tally of $508 billion. While these numbers appear nominally large, they don’t include monies from the 52% of survey respondents who professed unfamiliarity with 529 plans to Edward Jones and Morning Consult.

An even bigger 72% of individuals said they did not realize 529 funds could be used for certain apprenticeships. Sixty-five percent said they were unaware of 529 plan provisions for financing costs for kindergarten to twelfth grade. When asked about their use of a financial advisor, 78% of survey takers said they plan on their own without consulting an advisor, while 21% said they would welcome professional help.

Back to School

Recognizing the need to educate individuals who could benefit from a 529 plan, Julia Bartak, CFP and financial advisor with Edward Jones, spends copious time explaining to her clients how a 529 plan works. She says, “Education is the key to assisting people with whom I work. I focus on their long-term goals, whether it’s lifetime learning or retirement or a combination of goals. I talk about how a 529 plan can fit into their overall preparation for the future.”

UCLA Professor Walter Clarke, author of 401 Kid and chief financial officer for a handful of high-net-worth families, emphasizes the need to teach financial literacy as early as possible. His discussions with clients center on money as a store of value and the importance of setting up a 529 plan to meet goals such as optimizing tax benefits while growing a balance to pay for tuition. Clarke says, “For advisors, it should be about the end goal, not the product.”

Inflation and Behavioral Benefits

Paying for higher education has long been a significant stumbling block for all but the affluent. Greater regulations, lower taxpayer subsidies, the mushrooming cost of providing add-on services, easy access to student loans (which helps increase the cost of college in general), opaque pricing, and diminished competition in a fragmented market persist. The result has been, and still is, a significant sticker price for a four-year degree. J.P. Morgan estimates the average annual increase in college tuition is 5.6%, with a whopping cumulative number for the 1983-2024 period of 899%. No matter how the cost is measured, the college tuition inflation rate exceeds that of other primary household expenses.

Given these continued jumps in costs, it’s no wonder Jonathan Sparling urges financial advisors to recommend 529 plans to their clients. A former financial aid officer and current vice president of strategic partnerships with CollegeWell, he likens his company’s nationwide Private College 529 Plan product to a type of insurance. Sparling says, “My job in working with advisors, grandparents, and parents is to show them the economics, on a tax-adjusted basis.” Unlike 529 savings plans, his company offers a prepaid tuition vehicle to lock in rates at almost 300 participating non-public institutions. To test the sensitivity of assumptions for their clients, advisors can use CollegeWell’s online college savings calculator for free.

David Bauer, partner and wealth advisor with Perigon Wealth Management, LLC, is another advocate of 529 plans. Besides the tax benefits, he believes individuals experience less stress by being able to write a check from their 529 savings plan instead of having to sell stock, dip into their retirement plans or bank accounts, or otherwise liquidate existing investments. Regularly contributing is another plus in terms of discipline and positive behavioral reinforcement. Bauer says, “I’ve seen clients gain a peace of mind when they resolve to set up a 529 plan and commit to growing the account on behalf of their loved ones.”

Bauer is not alone in his views. In 2019, Ross Loehr, then listed as business development officer at Intuition College Savings Solutions, published an essay about how to motivate your children by telling them their parents had created a 529 plan just for them.

Zero Chance of Zero Risk

Savvy financial advisors understand the imperative of addressing both the potential upside of any product or strategy and the downside. Nothing is risk-free, including putting your money under your mattress. This notion of omnipresent risk extends to 529 plans.

The savings plan variety are vulnerable to risk factors such as shifts in market volatility, higher-than-desired management fees, zigzagging returns, potential losses or sub-par growth, restricted investment menus, stiff penalties on non-qualified withdrawals, deficient balances to cover costs, gift taxes due to excess contributions, complexity, diminished eligibility for financial aid, and changes in state laws that could jeopardize tax exemptions.

Prepaid tuition plans are deemed inflexible when a beneficiary’s target school is not on an approved list of participating schools. Pre-OBBBA, trade schools and apprenticeships were excluded. Post-OBBBA, 529 eligibility includes qualified credential program expenses. It remains to be seen whether prepaid tuition plans will change to include Workforce Innovation and Opportunity Act (WIOA)-approved program providers and licensing groups. Opportunity cost is another risk of prepaid tuition 529 plans. Since you are not investing in the stock or bond markets, you won’t directly benefit from outsized performance in the capital markets. Yet other risk factors include an adverse impact on financial aid eligibility, non-transferability of funds to non-participating colleges or universities, and modifications to state residency mandates.

Asset Allocation and Leftover Balances

Advisors differ when it comes to treating a 529 plan as a standalone item versus part of an investor’s portfolio. The question as to what is correct is a complex one. The answer depends on a household’s disposable income, net worth, tax situation, and investment goals. Bauer says, “With my high-net-worth clients, the 529 plan might be treated as a separate pool of capital if they can afford to pay for college tuition on their own.”

Financial advisors and their clients must agree on how to treat a 529 plan. Otherwise, it will be challenging at best to conduct scenario planning and optimize portfolio asset combinations. If a family member contributes to a stock-heavy 529 savings plan such as an early-stage age-balanced 529 plan, the account owner may decide to reduce equity elsewhere such as in their 401(k) plan. Correspondingly, as the equity percentage of an age-balanced 529 savings plan drops as the beneficiary gets closer to matriculation, that same account owner could, subject to short-term needs and long-term goals, ratchet up investment risk in other ways.

Leftover funds can’t be ignored, especially large amounts. Fortunately, you can usually change your beneficiary to a family member if the original person no longer needs or wants 529 plan proceeds. You can apply the balance to graduate school or another eligible venue. Seek expert advice about the tax implications and federal and state penalty amounts before you withdraw leftover funds. In cases such as a beneficiary’s death, disability, or receipt of some types of scholarships, the federal penalty is waived for funds, ex earnings. The Saving for College website illustrates how to calculate the 529 penalty.

Under the Setting Every Community Up for Retirement Enhancement Act, known as the SECURE 2.0 Act, passed in December 2022, you can transfer up to a lifetime limit of $35,000 of unused 529 plan monies into a beneficiary’s ROTH IRA, subject to certain conditions being met such as the 529 plan account having been opened 15 or more years ago.

Alternatives to 529 Plans

Other types of educational savings vehicles include Achieving a Better Life Experience or so-called ABLE accounts, Coverdell Education Savings Accounts (ESAs), and Gift of College gift cards. According to the ABLE National Resource Center, ABLE plans are designed to help qualifying persons with disabilities. A Coverdell ESA, like a 529 savings plan, offers tax-advantaged benefits but has lower contribution limits and is subject to income restrictions.

According to Patricia Roberts, chief operating officer with Gift of College and author of Route 529: A Parent’s Guide to Saving For College And Career Training With 529 Plans, Gift of College gift cards are a powerful device to support students on their education journey. They are easy to purchase and simple to give. These gift cards can be redeemed online into a 529 or ABLE plan account of the recipient’s choosing.

Like other experts, Roberts, a former bank attorney, understands the critical need for advisors to educate their clients. She strongly suggests advisors carefully explain options, noting that education is the second-largest expenditure for most households after purchasing a home. She says, “Education planning is at the heart of a family’s financial plan.”

She also suggests advisory firms eat their own cooking by having their advisor-employees set up their own 529 account(s), assuming it makes sense to do so. This way, advisors can share their hands-on knowledge about 529 plans when they meet with their advisees.

What’s Next

It’s a brave new world for educational savers — and none too soon. In 2025, lawmakers outdid themselves by expanding ways families can help their children or grandchildren obtain a degree or certificate. Those who want to earn a four-year or graduate degree are frustrated by rising costs. Those who opt for a vocation welcome economic support as they pursue the requisite training to meet industry’s rising demands. Just last month, Jim Farley, CEO of Ford Motor Company, joined other executives in bemoaning the dearth of capable mechanics and tradespeople to fill thousands of open positions. Families want help paying for tuition at K-12 public, private, and religious schools.

Clients need knowledgeable partners who understand the intricacies of 529 plans and can guide them as to how best to save for the education of those they cherish.

After a productive career as a Wall Street trader, testifying investment expert witness, and corporate trainer, Susan Mangiero, Ph.D., CFA, CFE, FRM, MBA, MFA currently works as a B2B content strategist, executive ghostwriter, and independent financial journalist. Her articles, books, and thought leadership appear in more than 100 business outlets.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All