The dueling suitors for Warner Bros. Discovery Inc. have had a rough week. Will this rule out an auction? Don’t count on it.

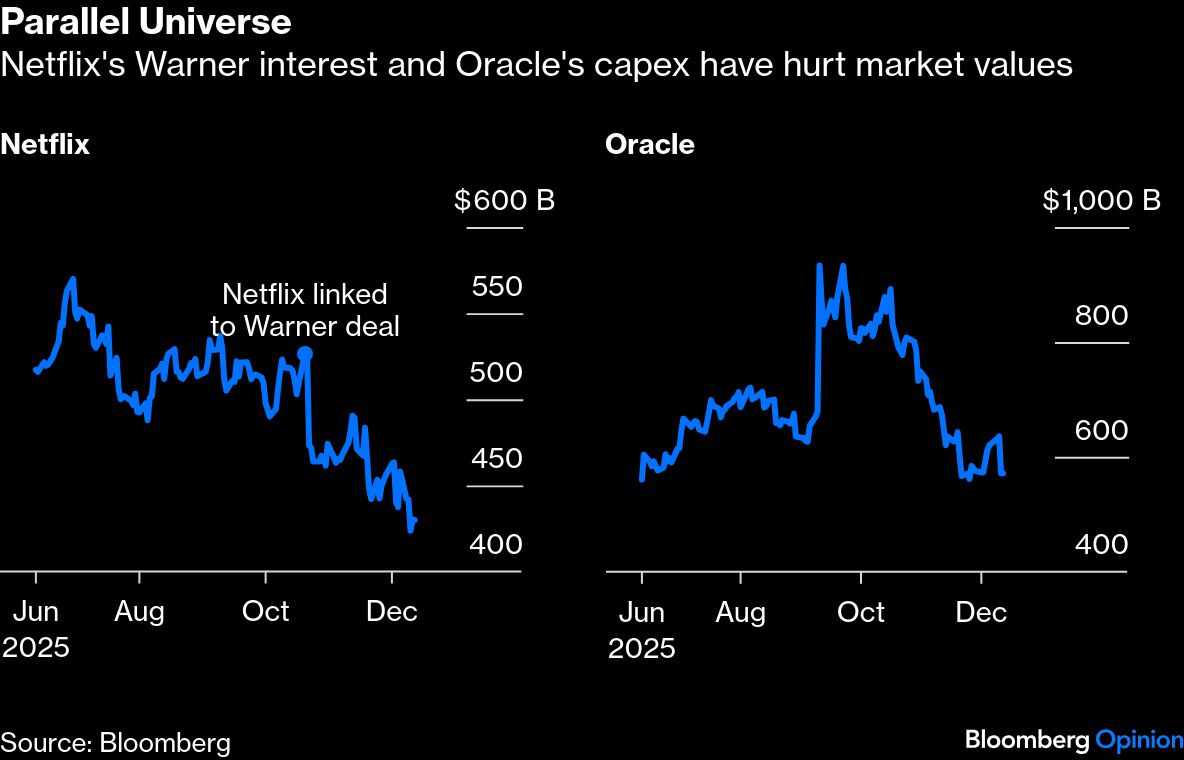

Netflix Inc.’s shares have slid further, to sit nearly 25% below where they were before its interest in Warner emerged. Oracle Corp., the source of wealth for the rival party, the Ellison family, tumbled to take its peak-to-trough fall to nearly 40%. The hits are worth roughly $100 billion and $360 billion respectively.

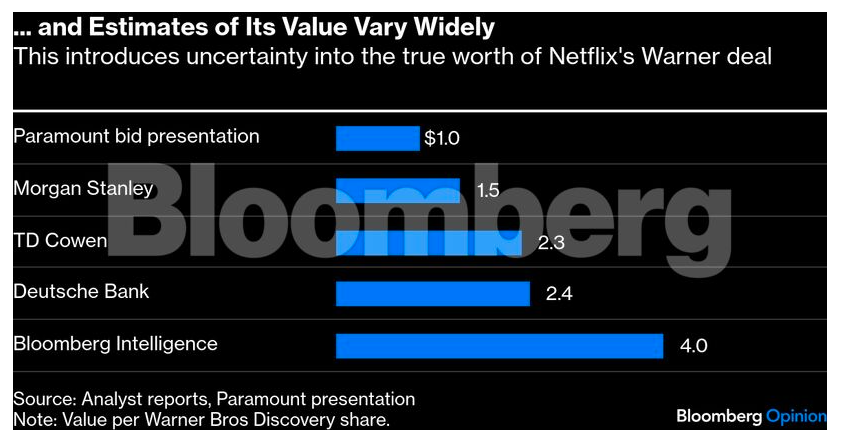

For now, Netflix leads having secured the backing of Warner’s board to buy the company for $27.75 a share in cash and stock, after the cable business is separated next year. Estimates for the value of that legacy broadcast arm that Warner shareholders will vary markedly. Some analysts put it at slightly more than $2 per Warner share. On that view, the full Netflix offer is worth $30 per share, or about $78 billion, before taking into account the risks around antitrust clearance.

Paramount Skydance Corp., backed by Oracle cofounder Larry Ellison and led by his son David, this week bid to buy Warner outright for $30 a share in cash. Some Warner shareholders cheered this simpler pitch. But the Ellisons still need to persuade the target’s board to scrap the Netflix agreement before signing a new deal with them. Until that happens, Netflix doesn’t strictly need to respond.

When the Ellisons made their offer privately last week, they said the terms weren’t best and final. So an auction seems more than plausible.

The plunging shares of Netflix and Oracle matter in varying degrees to both sides. The Netflix offer’s stock component is small and partly adjusts for changes in the bidder’s own stock price. Hence, the implied value of the offer is down less than 1% since being made despite a 9% fall in the streaming giant’s shares.

Nor is Netflix reliant on issuing stock to sweeten the terms. As Bloomberg Intelligence says, Netflix could raise its bid with additional debt while maintaining a strong credit rating. It has barely any leverage today.

A price hike does risk pushing net debt above the psychological pain barrier of three times profit (measured by earnings before interest, tax, depreciation and amortization). But that wouldn’t hurt for long. Rising revenue, profit and cash flow would help bring the leverage ratio back down.

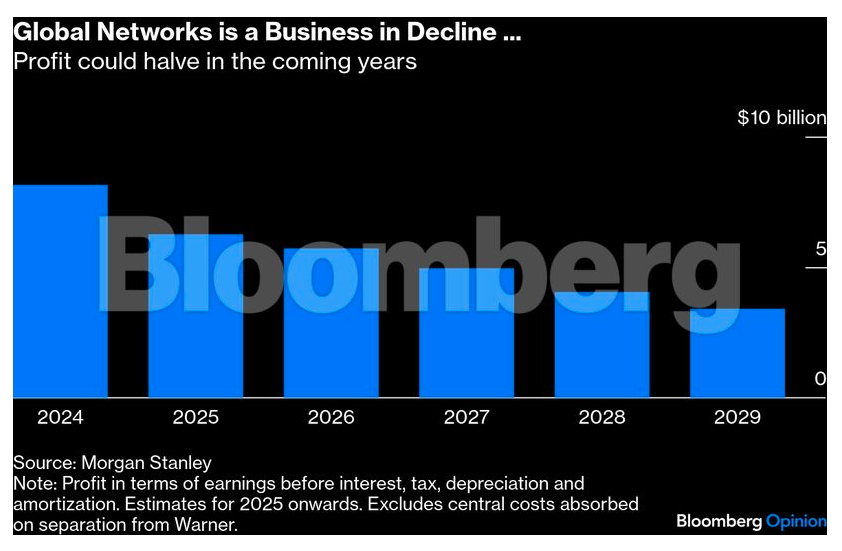

One possible glitch for Netflix is the uncertainty over the value of that declining cable business, known as Global Networks. Paramount says it’s only worth $1 per Warner share based on a 4.5 times multiple of expected Ebitda in the 12 months from Oct. 2026. Global Networks will carry heavy debts, so small changes in its overall value disproportionately affect the per-share value. Its peer AMC Networks Inc. trades on a five-times forward multiple. Warner shareholders will hope Global Networks could command something like that.

As for the Ellisons, they say they have “backstopped” $41 billion of equity to support the transaction alongside private equity firm RedBird Capital Partners. That’s important in guaranteeing the finance if there’s a hitch with the money coming from the other equity partners, who comprise sovereign funds from Saudi Arabia, Qatar and Abu Dhabi plus Jared Kushner’s Affinity Partners.

Paramount has preempted concerns about Middle East states owning a big slice of culturally and democratically important US media and news assets. The wealth funds’ equity carries no voting or governance rights. Paramount says in filings that this renders the transaction immune to CFIUS security scrutiny on foreign investments.

But if the structure becomes a political obstacle, the Ellisons’ backstop will be crucial. Larry Ellison’s net wealth fell $25 billion yesterday. It was still $258 billion, way more than what’s needed here. He still of course needs to write a huge personal check, which means cashing in liquid assets. It’s hard to believe he couldn’t, with such immense resources. And yet the solidity of Paramount’s financing was subject to much back-and-forth in earlier engagement with Warner before Netflix got its deal. It’s a concern for the target.

Maybe at the margins the huge value destruction suffered by both suitors will dampen animal spirits. From the outside, one can only conclude that the volatility in Oracle stock obviously doesn’t help and will likely matter to Warner. As for Netflix, this deal stands to change its profile from a lowly leveraged dependable tech stock into a very different animal. The drop in its share price doesn’t stop it sweetening its bid, but it does scream out the question of whether it should.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Chris Hughes