One of the first things I learned about retirement finance is that there are only three ways to increase income once you stop working:

- Save more

- Work longer

- Take more risk

This is true whether you have a traditional defined benefit plan or a defined contribution plan, such as a 401(k). And yet, the few people running pension funds, savers and much of the financial industry seem unable to accept this hard truth.

Defined benefit pensions are much less common in the private sector, having been largely replaced by defined contribution plans. But the delusion you can get something for nothing makes the traditional pensions much riskier than they appear. Making promises far into the future enables pension fund managers to fully embrace this fallacy as their investment strategy. Sure, defined contribution plans have their own risks, but those are transparent and there are no incentives to ignore risk. People worry defined contribution pensions made the world riskier, but many savers should be grateful they have control over their savings.

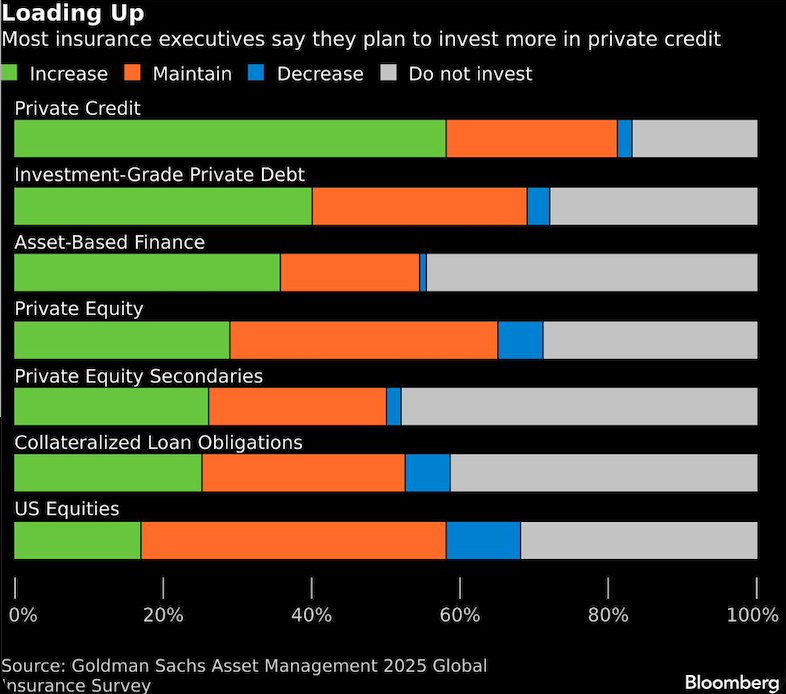

The latest example is the insurance industry, which has taken on the obligations of some large defined benefit pensions. The insurers are funding benefits by investing in private assets with dubious value, have taken on reinsurance to justify holding less capital even though those reinsurance companies are their own affiliates and located off-shore where they are under-regulated. Private credit now accounts for about 35% of the investment portfolios of North American insurance companies, Institutional Investor reports, citing International Monetary Fund research. A decade ago, it was around 31%.

On paper, it looked like a reasonable idea because the strategy promises high returns, which allows insurers to set aside less money to pay out on things like life insurance and annuities. It’s tempting to believe you can get something for nothing, and no one falls for that more than those who should know better, meaning institutional investors such as pension fund managers and insurers. This is why public pensions are chronically underfunded and why many private sector plans went bankrupt before they were better regulated in the 1970s. (And many of those plans closed after being forced to properly account for risk.)

The latest iteration of the good-idea-ending-badly story is funds investing in private markets, whose promise of high returns comes at the expense of liquidity and transparency. It also means no one really knows what the investments are truly worth. So as pensions need their money to fund payouts, many are finding these investments weren’t so great.

Of course, if insurers invest wisely and undertake good risk management, there is nothing wrong with this arrangement. But if an insurer’s investments falter, pension beneficiaries could have few protections given that, depending on the state where they are located, insurers can be less well-regulated than private-sector pensions. It should be noted that the Bank for International Settlements said last month that insurers tend to rely on smaller ratings firms when determining the safety of their private investments, raising the risk of “inflated assessments of creditworthiness.” Insurers often seek higher ratings because of their lower capital requirements, while smaller agencies “may face commercial incentives” to provide better grades, the BIS said.

In principle, traditional defined-benefit pensions seem better than, say, 401(k) plans because the risk is pooled among many beneficiaries and the assets are professionally managed. But history shows the power of managing large pools of assets combined with the temptation to believe you can consistently beat the broad market often leads to underfunded liabilities that need to be paid long into the future. Defined benefit pensions are not, and have never been, risk-free because it is very hard to get the incentives right even with the best intended regulations.

The advantage of defined contribution pensions is they are more transparent and, more recently due to good regulations, invested in low-cost funds. A proposal by the US government to let them invest in private and even more exotic assets is a mistake, But as long as private assets are not included as a default investment (what you automatically get invested in when you sign up for a 401(k) with your employer), they probably won’t cause the same problems that we have seen with traditional pensions.

Defined contribution plans do have one big weakness: They are effective at helping people accumulate assets, but less good at helping people manage the risk around spending in retirement. Neither the retirement industry nor regulators have figured out a solution. But whatever they come up with, here’s hoping it includes options that are well-regulated, transparent and don’t promise something for nothing.

A message from Advisor Perspectives and VettaFi: Are you backed by institutional quality bond funds? Click here to learn more.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Allison Schrager