The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

Some colleagues pointed out to me a recent Morningstar article by Larry Swedroe. Swedroe is a researcher, consultant, and author of 18 investing books. The article titled “The Hidden Costs of Passive Investing” made the following claim:

While passive funds advertise low expense ratios, investors should recognize that the total cost of ownership includes these hidden implementation costs. For example, a fund with even a 0.04% expense ratio might actually cost 0.4% or more when including trading impact.

I was stunned by Swedroe’s claim that total expenses might be 10 times higher than the stated expense ratio, but he cited academic research that supported it.

Part of Swedroe’s argument has to do with when an index is reconstituted. He cites research that asserts stocks added to the S&P 500 trade at steep valuation premiums (~92% more expensive than the market), while deletions are deep discounts (~55% cheaper).

Swedroe notes that “new entrants beat the S&P 500 by 41.5%; deletions lagged by 29.1% (gap of 70%). In the year after, deletions outperformed additions by 22%. Around announcement: Additions gained around 5%, while deletions lost around 7%, creating a 12%–16% swing largely stemming index fund trading pressure.”

Swedroe points out other indexing flaws including cash drag, limited tax efficiency, and post-IPO underperformance. He concludes:

While media, academic, and advisor scrutiny of index funds has focused on expense ratios and management fees to investors, the empirical research we have reviewed shows that the hidden costs of passive investing represent a significant, yet underappreciated, drag on investor returns. While passive investing remains a valuable tool for most investors, understanding these costs is crucial for making informed decisions about fund selection and portfolio construction.

Fact-Checking the Hidden Costs

These types of claims are not new. I argued against them with financial advisor Ric Edelman more than a dozen years ago when he twice publicly claimed Vanguard was hiding fees. It was easy to disprove by looking at the Vanguard S&P 500 Index Fund Admiral Shares (VFIAX) to compare performance to the total return (including dividends) of the S&P 500 itself. The finding was that the fund not only performed as well as the index total return minus the expense ratio, it actually made up some of the fees, performing better than the expense ratio would have predicted. Edelman attributed that to luck.

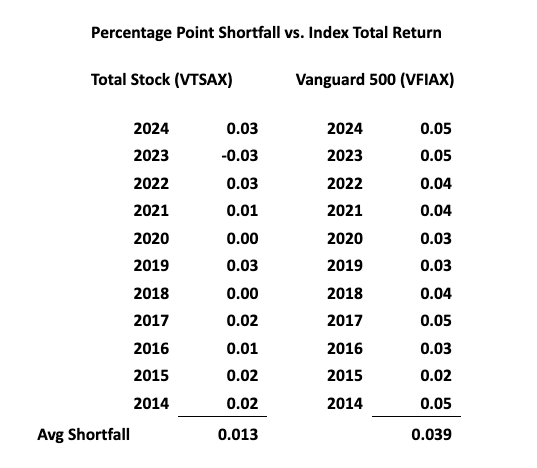

My initial reaction was to compare the performance of the total stock and S&P 500 index funds to the total return of the indexes they track — the CRSP US Total Market Index and the S&P 500 index. Morningstar researcher John Rekenthaler already beat me to it in an email he sent me and others. Rekenthaler looked at the performance of the two largest index funds on the planet. He used the mutual fund Vanguard Admiral share classes, which have the same 0.04% annual expense ratio Swedroe stated “might actually cost 0.4% or more.” Below is the data Rekenthaler sent.

Rekenthaler stated the two funds alone account for 30% of U.S. equity index assets, and similar numbers apply to every major S&P 500 fund (such as those issued by Fidelity, Schwab, iShares, etc.). Morningstar reports that all Vanguard share classes of the total stock fund have about $2 trillion in AUM collectively, while the S&P 500 fund’s share classes have about $1.4 trillion AUM.

Rather than have a 0.40 percentage point average shortfall versus the total return of the indexes, they actually made up some of the 0.04% annual expense ratio through securities lending and other methods, aligning with my previous finding. Both of these index funds have an ETF share class with an even lower 0.03% expense ratio.

Thus, at least for the largest U.S. stock index funds, there appear to be no “hidden costs” and, in fact, the expense ratio actually overstated the total net expenses paid by investors. Even the S&P 500 index itself, which the Swedroe article claimed was selling deletions at “deep discounts” and buying new entrants that underperform, did not appear to supported by the data.

I showed the data to Larry Swedroe, who responded:

I have not seen any research on the total market and would not expect that since almost no trading done, so no, this doesn't apply to TSM funds. Never mentioned them in my piece. It is the replication issue of other indices that can have important consequences that are not disclosed.

But he stuck to his view on the S&P 500 index fund arguing that the index itself was flawed, as turnover caused the index to underperform. He suggested I talk to Matthew Zenz, a former DFA portfolio manager. Zenz, now chief investment officer at Longview Research Partners, estimates that S&P 500 turnover causes index managers to trade 20-30 times the normal volume of those stocks on one day, which creates a drag on returns in the 0.05%-0.15% range annually.

The S&P 500 has outperformed the total stock market over the past 15 years as the large tech stocks have become larger and smaller and value companies have grown more slowly.

Finally, Swedroe also makes a claim that index funds have limited ability to pursue tax-saving strategies, including avoiding short-term gains and offsetting capital gains with losses.

How tax inefficient were these two index funds? It turns out that the total capital gain distributions over these years was zero for each fund. That’s pretty tax efficient. My DFA funds — which Swedroe has said are designed to reduce turnover expenses and improve tax efficiency — have underperformed and distributed capital gains, though less than most mutual funds. ETFs now virtually solve the tax-efficiency issue.

Lessons Learned

Swedroe’ s article does a great job of citing academic literature, and much of it could be true for many of the thousands of narrower index funds, though there are few that have the 0.04% annual expense ratio he claims has the 10x hidden costs. Rekenthaler told me that 80% of U.S. index assets are in either total stock or S&P 500 index funds, noting that this did not include strategic (also known as smart) beta funds.

In my view, the majority of index funds are active. Though I agree with Swedroe’ s point that the S&P 500 has a committee that adds and deletes companies, I strongly doubt 2% annual turnover creates an annual drag of an additional 0.36 percentage points above the 0.04% expense ratio.

In fact, 15 years ago, I wrote a piece titled “The Case Against the S&P 500 Index Fund" that made similar points. It resulted in a response from John Bogle himself agreeing with my assertion that a total stock index fund was better, but also pointing out that since 1928, the S&P 500 has bested the total stock market by 0.2 percentage points annually. Bogle had a habit of being right, and the last 15 years — ending November 3, 2025 — showed the S&P 500 besting the total market by more than 0.4 percentage points annually.

Yes, additions and deletions have added costs. But Morningstar reports that VFIAX had only a 2% annual turnover, so I find it hard to believe that this small turnover could take 0.4% annually from returns. By comparison, my DFA Small Cap Value fund (DFSVX) had a turnover of 12% annually, or six times the turnover. Swedroe told me, “There are lots of hidden costs of all systematic strategies, and the bigger you get, the more they are.”

‘Total Stock’ Means Every Stock

In my view, passive investing involves owning, as close as is economically feasible, every stock weighted to market capitalization. So this means total stock index funds. There is no committee selecting additions or deletions to an index. Funds that pick styles, sizes, sectors, industries, themes — or anything else — are active, as they pick parts of the market that investors hope will outperform.

Low-cost total stock index funds mathematically must beat the average dollar invested, which translates into a virtual certainty of besting most investors. As Nobel Laureate William Sharpe put it:

“Properly measured, the average actively managed dollar must underperform the average passively managed dollar, net of costs,” Sharpe’s paper noted. “Empirical analyses that appear to refute this principle are guilty of improper measurement.”

Criticisms to Sharpe’s The Arithmetic of Active Management note that the market is not a closed system where, for every buyer, there is a seller. For example, new IPOs and stock buybacks change the composition of the stock market. Does that invalidate the arithmetic? In a previous article examining Sharpe’s claims, Rekenthaler stated, “The impact of new issues and stock buybacks strikes me as an immaterial wrinkle.”

Is Vanguard hiding costs in their index funds? I think not! Technically, the Vanguard Total Stock Index Fund has systematic positive tracking error by making up some of its expense ratio. A Vanguard spokesperson explained that Vanguard adds value through securities lending, participation in syndicate offerings, managing complex corporate actions, and proprietary trading techniques that allow them to pick up fractions of basis point here and there throughout the year.

Be wary of claims that indexing and passive investing have huge hidden costs, or my personal favorite, the claim that passive investing is worse than Marxism. More recently, ARK Invest CEO Cathie Wood posted on X that “Index-based investing is a form of socialism.”

In the case of Swedroe’ s claim that funds with a 0.04% annual expense ratio actually had 10 times the total fees, he now says he didn’t mean it for total stock index funds, yet they hold a huge proportion of the assets in U.S. stock index funds. And though S&P 500 index funds have bested total U.S. stock index funds, I believe total stock index funds are superior.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Allan Roth

The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.