If owning a home is still the American dream, then it is increasingly out of reach for many young Americans. The average age of a first-time homebuyer is now 40, up from 33 just a few years ago and 29 in 1981.

To which I say: It’s just as well. Buying a home in your 20s is not the best financial goal, nor should it define the American dream of financial success.

I am not here to minimize the housing affordability crisis, which is driving economic populism on the left and the right. And I acknowledge that homeownership has a special value in the US, both psychically (it is associated with “making it”) and financially (it has tax benefits, in the form of the home mortgage deduction, and real estate is seen as a good investment).

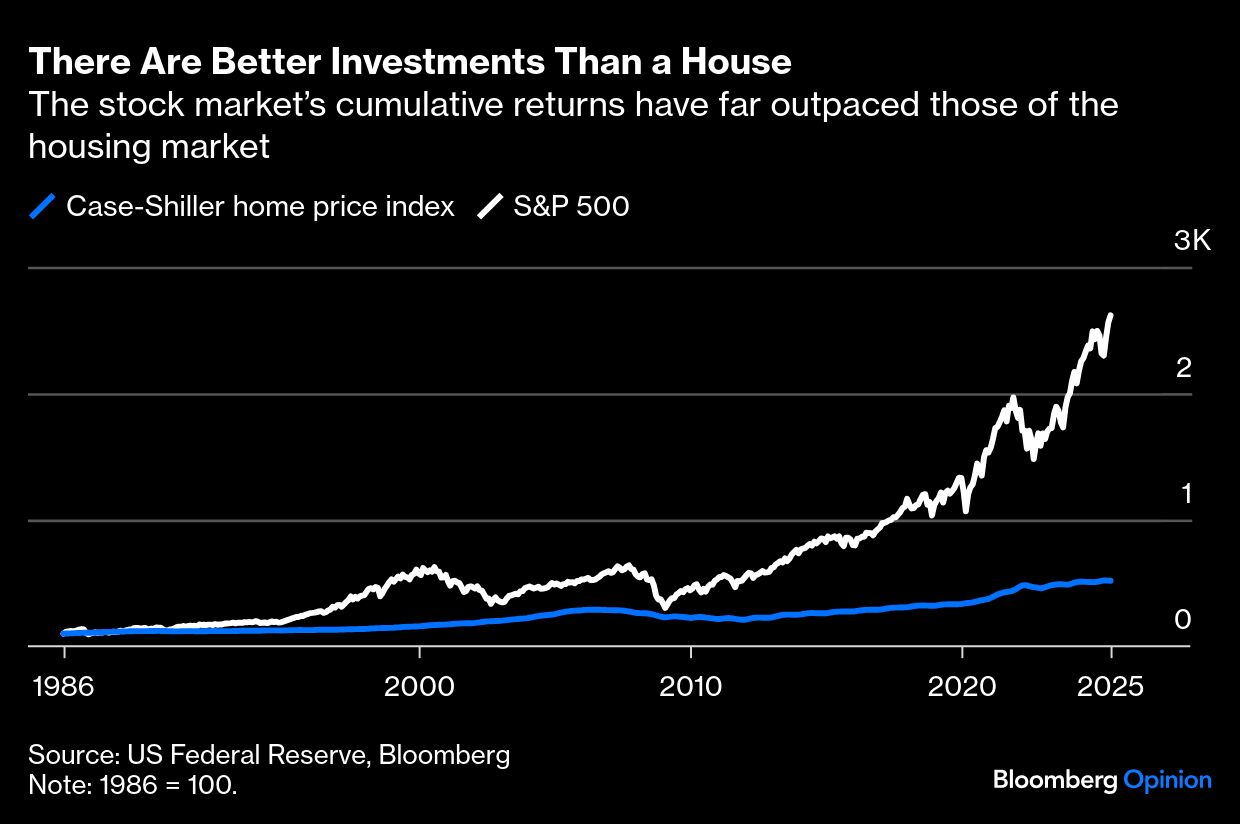

But owning a home does not always make financial sense. First, with taxes, HOA fees, insurance and maintenance, homeownership incurs costs above and beyond a monthly mortgage payment. It is also a risky financial bet. It requires a large down payment — tying up assets in something illiquid. That carries an opportunity cost, especially for young people, who may be better off investing that down payment in a well-diversified market fund.

True, a home can be sold, but that takes time and involves substantial transaction costs — and depending on the real-estate market, could result in a loss.

In short, buying a home is a concentrated bet that is highly correlated with your job prospects, since local real estate markets tend to be tied to the health of the local economy. That’s why most young people would be better off renting. They have less job stability and require more financial liquidity and less debt. And if they do buy, they are more likely to need to sell within a few years.

If you don’t have enough capital to buy a home in your 20s, it’s OK — in fact, it’s normal. And even if you do have enough money, buying real estate is not necessarily your best financial option.

All this said, 20-somethings have good reason to feel like they can’t get ahead, and the cost of housing is a big reason. While Generation Z does have more wealth than their forebears — median net worth (in 2025 dollars) for households aged between 22 and 30 was about $25,000 in 2022, compared to $14,200 in 1989 — they tend to have more student debt.

And money does not go as far as it once did. Buying a home used to be easier. In the 1980s, home prices were lower, though mortgage rates were about three times higher. Back then, people in their 20s tended to live in cheaper, less dense areas, and were more likely to be married with children.

None of this is much comfort in a brutal housing market that is the result of some misguided policies, about everything from building regulations to land use to interest rates. There simply isn’t enough housing being bult in the US, and there are other distortions. The age of first-time buyers shot up after 2022, when interest rates increased. Now buyers are facing both high mortgage rates and high prices — and many existing homeowners, who refinanced when the Federal Reserve’s quantitative easing policy helped mortgage rates go below 3%, aren’t selling.

Unfortunately, the rental market is not much better. This is especially true in New York City, where the average rental in Manhattan has increased 64% since 2021. Again, that increase was due, in part, to nonsensical regulations, which benefit people in rent-stabilized housing but decrease inventory and increase prices for everyone else.

Housing is so expensive in America because politicians and other officials, at the local and national levels, do all they can to limit supply and boost demand. And why do they do that? Because they believe that homeownership is, as the real estate lobby puts it, “the cornerstone of the American dream.”

A home can be an important asset. But it can also be a bad financial investment, especially for the young. The idea that homeownership is a prerequisite for success in America is not only demoralizing. It is also making homeownership more expensive.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Allison Schrager