The rebirth of private equity dealmaking has been supposedly just around the corner for well over a year. But even as investment bankers cheer a rush of mergers & acquisitions and the reopening of the market for initial public offerings, many financial sponsors are still struggling to catch the same wave.

The lack of exits from portfolio companies by private equity has been a burden since interest rates shot higher in 2022. It’s left many managers struggling to raise fresh money from investors amid a drought of payouts in the other direction. It also led sponsors to hunt out new and potentially riskier ways to return cash to their backers. I predicted in summer 2023 it would take a long time to unjam the private equity machine; today, the cogs are still turning slowly.

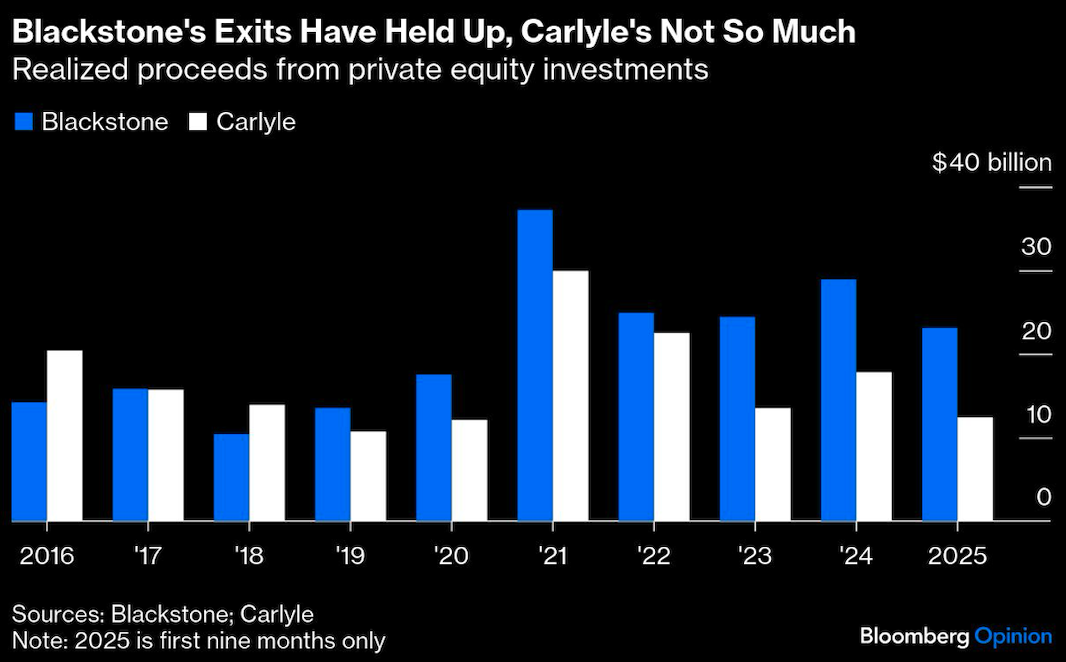

But they are starting to rotate, even if all firms aren’t enjoying the same successes. One leader this year is Blackstone Inc., on course for the most private equity exits since the boom year of 2021 if it maintains the pace set over the first three quarters of this year. “This deal dam is breaking,” the firm’s president, Jon Gray, told investors last month. Blackstone got three new listings done in the third quarter, and founder Stephen Schwarzman predicted that the IPOs it intends to pursue over the next 12 months add up to one of the biggest years for business sales in its history – if they all get done.

The Carlyle Group Inc., in contrast, just reported its weakest quarter for exits since the third quarter of 2020: It got just $2.3 billion of sale proceeds in the third quarter of 2025, although its total of $12.4 billion over the first nine months is ahead of the same periods in 2024 and 2023.

Carlyle has announced $5 billion of planned exits, including the IPO of Medline Inc., that it hopes to complete later this year or early next, according to Justin Plouffe, Carlyle’s incoming chief financial officer. “While Q3 was a lighter realizations quarter, we expect a significant step-up in Q4,” he told investors on Friday.

Apollo Global Management, which is more focused on the hotter markets of private credit, said on Tuesday that disposals by its equity funds were light in the third quarter with exits "prudently delayed" in the uncertain environment.

For the industry as a whole, the cash flowing back to investors has been poor this year, adding to disquiet among the pension funds, endowments and other big institutions that back private equity funds. Quarterly payouts of less than $52 billion from the buyout industry in the second quarter of this year were the lowest since the second quarter of 2020 during the shocking onset of the Covid-19 pandemic, according to data from MSCI.

Bankers and private equity dealmakers were convinced that this would be the year of a major rebound in activity, with David Solomon, Goldman Sachs Group Inc.’s chief executive officer, predicting a reacceleration into 2025 during the bank’s earnings call in July 2024.

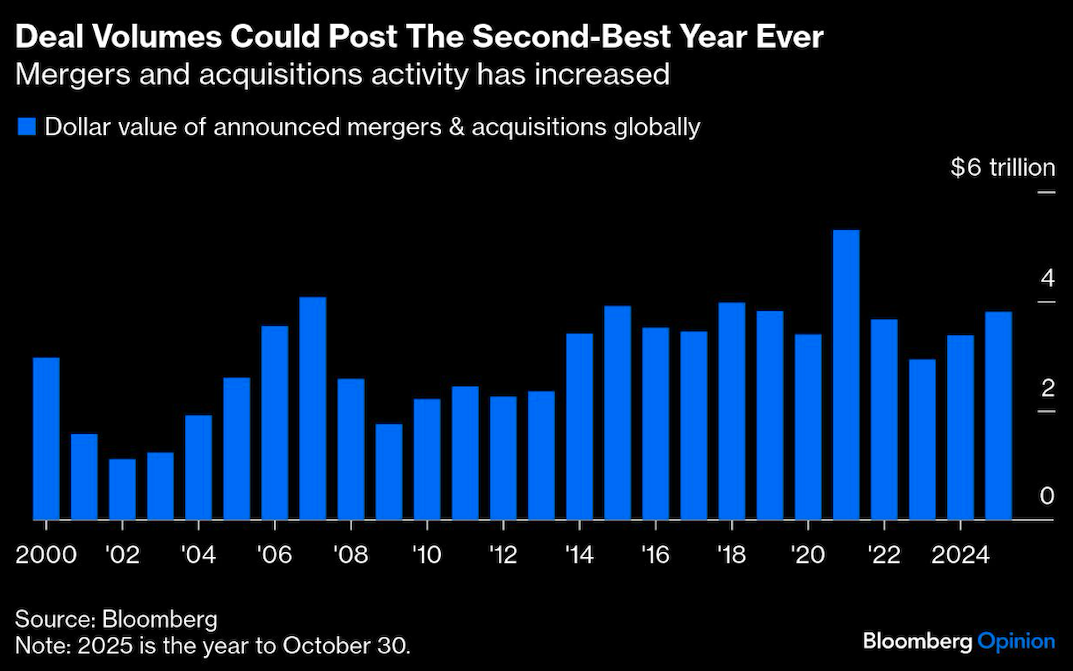

Of course, one big spanner in the works was President Donald Trump’s carpet-tariffing of the entire world in April this year. However, IPOs have come back since the summer, while global M&A could be on course for the second-biggest year ever, according to Bloomberg News. By the end of October, $3.7 trillion worth of deals had been announced, compared with the all-time high of $5.3 trillion in 2021 — only a handful of years have gotten close to $4 trillion for the full 12 months.

This year’s activity has been primarily driven by the artificial intelligence boom, especially OpenAI’s dizzying spree of investments and chip-sourcing deals, as well as traditional corporate transactions. There has been activity among financial sponsors, such as the $55 billion buyout of Electronic Arts Inc., and the recent Blackstone and TPG $18 billion offer for Hologic Inc. However, the industry’s trouble raising new funds means its “dry powder,” or money waiting to be invested, has shrunk 6% since its peak in the first quarter of 2024, according to MSCI – although there’s still more than $1 trillion of committed cash in that pot.

The biggest issue for the buyout barons is they spent too much at too high valuations when money was fast and loose in 2021 and early 2022. The injection of central bank and government cash into households and markets to help economies cope with pandemic shutdowns has left private equity with too many investments that are worth less now than when bought.

As long as IPO markets were effectively shut, sponsors could tell their backers they had few good options. They could roll investments into so-called continuation funds, which raise questions about valuation and many investors aren’t keen on, or they could sell to a strategic buyer that could often dictate the price.

Now that stock markets are buying new companies again, more private equity managers should have two proper exit routes to judge against each other — IPO, or strategic sale. They may not love the prices available, but they’ll have to explain why they don’t want to sell rather than arguing that they can’t. Investors are likely to see that as more about managers protecting their bonuses rather than a concern for the returns that backers want to see.

Trump could still knock markets off course with more ill-judged policies, and there are real worries about overexuberance in markets inflated by tech and AI. But while the current animal spirits last, private equity must squeeze more deals out of those pipelines, whether or not those sales are at the prices managers want.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.