JPMorgan AM Sees Long Bond Revival as Supply Glut Ebbs

Long-dated bonds are looking more attractive as governments and central banks take steps to curb the glut in that segment of the market, according to JPMorgan Asset Management.

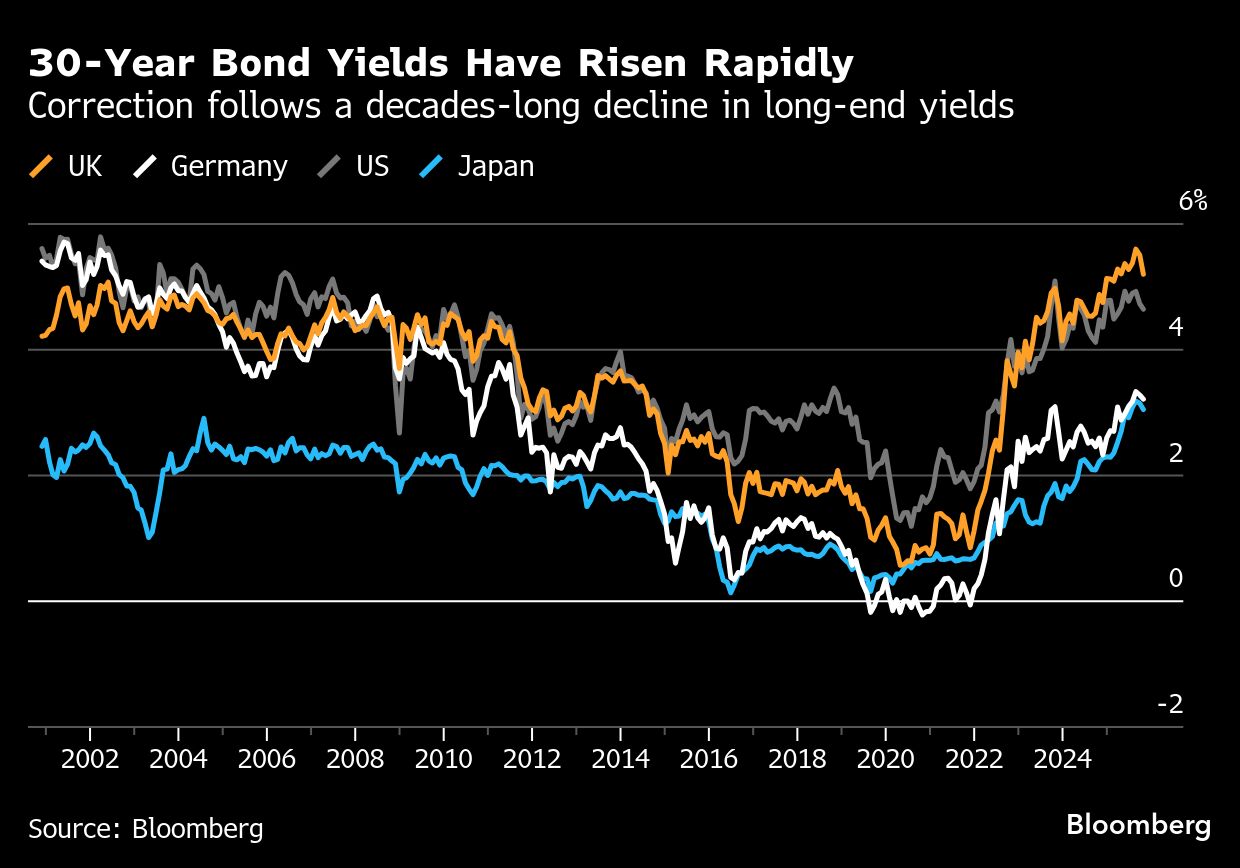

With debt offices slashing sales of longer-maturity debt and central banks easing the pace at which they offload the securities held on their balance sheets, the recent drop in 30-year bond yields is likely to run further, said Seamus Mac Gorain, head of rates at the $3.4 trillion firm.

The fund favors longer-dated British and Australian bonds, and is also positioned for Japan’s yield curve to flatten, led by long-end outperformance.

“The past few years has been about the excess of government bonds but the tide is changing,” Mac Gorain said in an interview, noting that officials are aware of the drop in buying interest for long-dated bonds, and are pro-actively realigning supply.

“The government and official sector are now trying to address that supply-demand imbalance a little bit,” he said.

The selloff in long bonds panicked markets earlier this year, when concerns grew about swelling government deficits. However, since early-September, yields on 30-year Treasuries have slumped over 30 basis points, while UK gilt yields are down 55 basis points. Japanese long yields have dropped 30 basis points from their early-October record high.

One reason for the recent calm is a shift in debt issuance toward shorter maturities from countries such as Japan and the UK. Meanwhile, the US Treasury has employed buybacks to ease pressure on the long-end.

In addition, the Federal Reserve, the Bank of England and the Bank of Canada have all been tweaking their quantitative tightening programs, and slowing the pace at which they shrink their crisis-era portfolios. The Fed said this week it will halt its $5 billion-a-month runoff of Treasuries from Dec. 1.