Nvidia CEO Jensen Huang’s insistence this week that he did not “believe we’re in an AI bubble” is all well and good when you’re the man selling the finest shovels for the artificial-intelligence boom. But what of the companies that are expected to turn all that AI building into gold?

Five of the so-called Magnificent Seven — Amazon.com Inc., Alphabet Inc., Meta Platforms Inc., Apple Inc. and Microsoft Corp. — will report earnings this week. Optimism going in could not be higher, with shares of the world’s largest technology companies driving up stocks to records this week in what is largely a story about AI and its promise.

But when it comes to searching for signals on AI’s potential to provide a healthy return, Wall Street has often proved to be fickle, reacting harshly to even the slightest blip. Here are the signals I’m looking for Wednesday and Thursday as the tech giants discuss their performances.

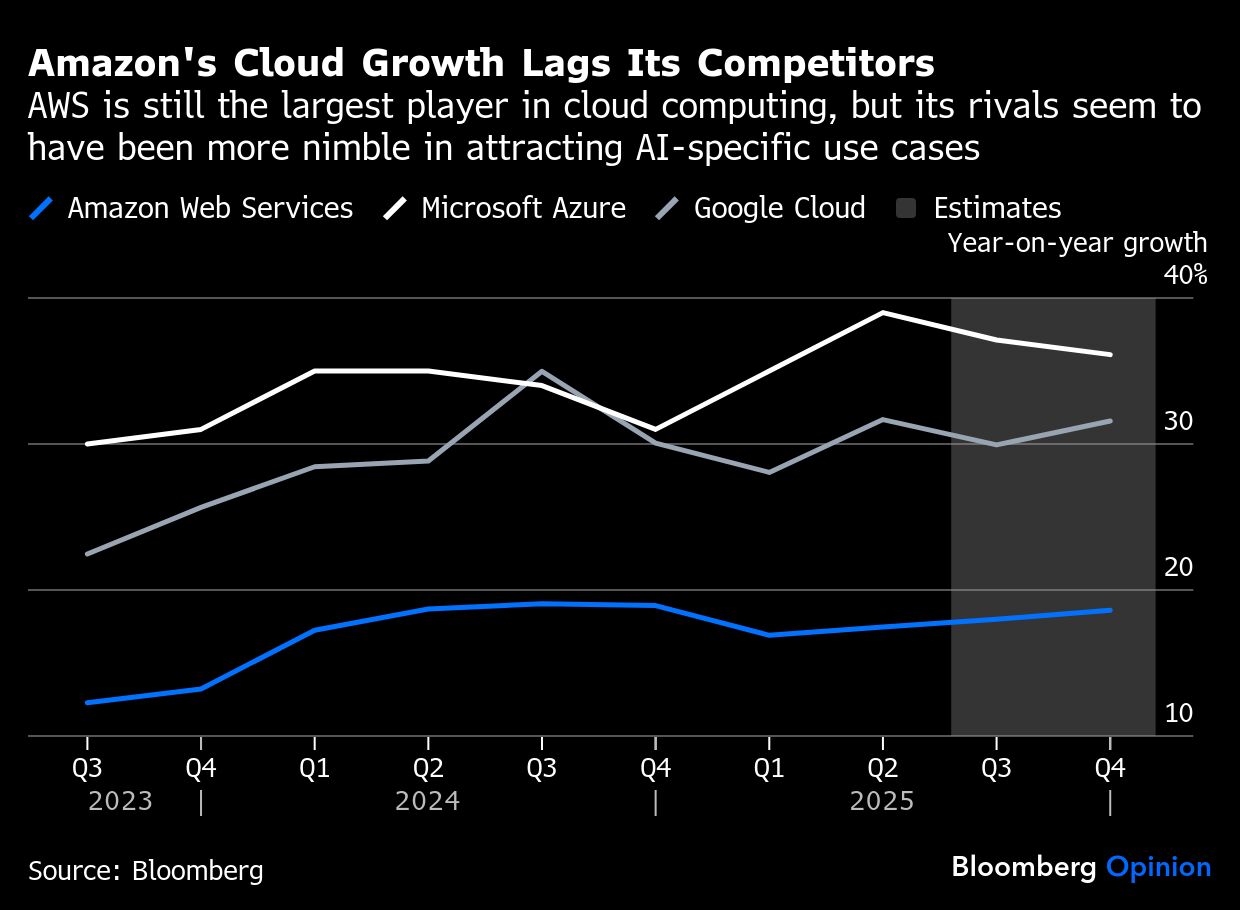

Is AWS improving against Microsoft Azure and Google Cloud?

This month’s 15-hour-long failure affecting vast swaths of Amazon’s cloud client base was deeply embarrassing. Memories, however, are short — and with the problem patched up and operations running smoothly again, investors will now be far more concerned by the broader trajectory of Amazon Web Services, particularly how it’s faring in the AI race. While it is still comfortably the largest cloud provider in the world, its ability to attract AI-specific use cases — training and inference — are in question. Microsoft just sealed a revised pact with OpenAI that will allow it to keep its close relationship and associated cloud income, at least for the next few years. Google Cloud has been picking up big money deals, and its homegrown chips are starting to gain a reputation as an alternative to those made by Nvidia. Amazon is competing on all of these fronts — investors will want indications of how well.

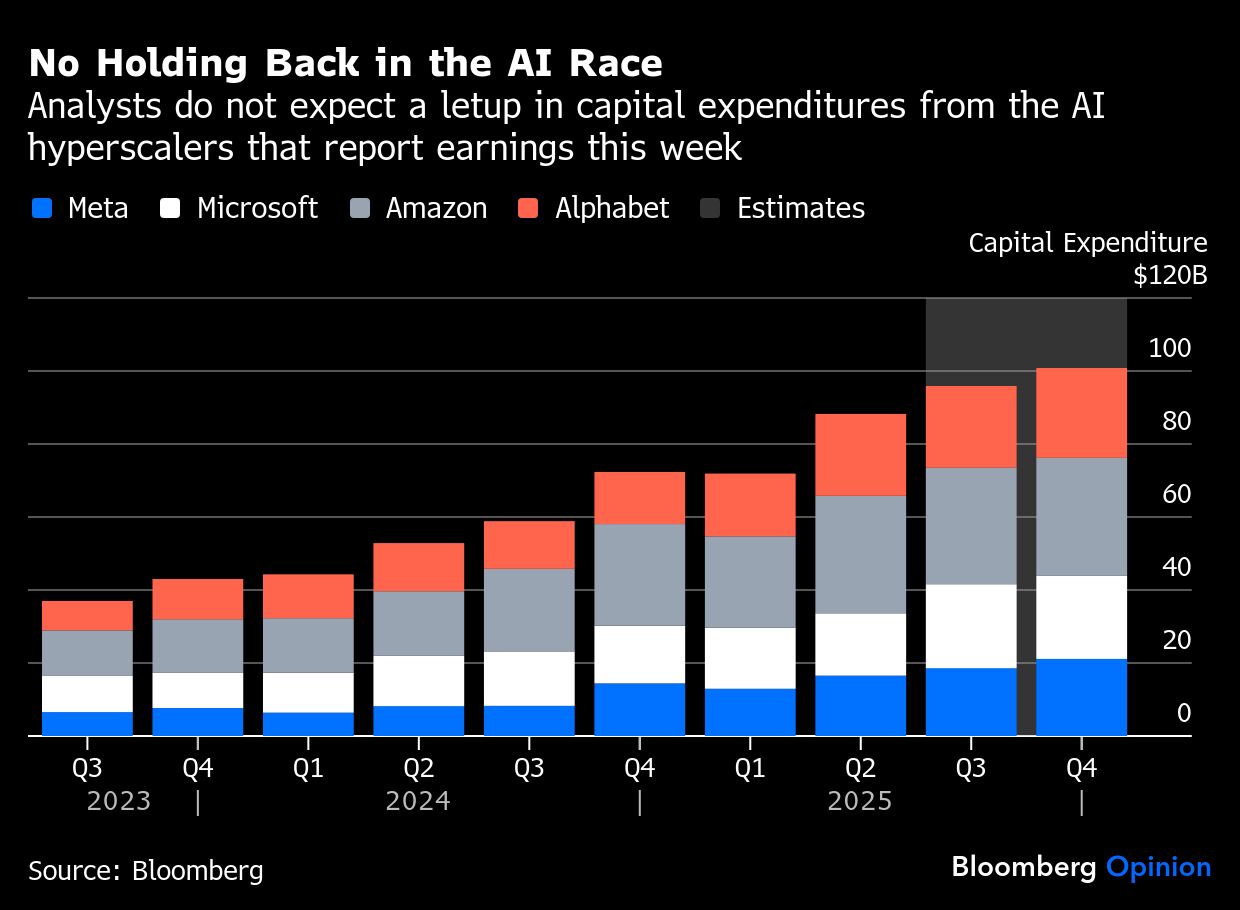

How much is the demand crunch pushing up capital spending?

There’s a reason every new day brings news of a huge deal for data center construction. Demand for computing power is currently outstripping supply. That’s why we’ve seen an explosion in capital expenditures this year that is expected to continue through 2026. The question for this week of earnings, then, is whether those projections are adjusted and by how much.

Who needs AI when you’ve got the iPhone?

Apple hit its first record price of 2025 on indications that the latest line of iPhones experienced stronger-than-expected demand in its first 10 days on sale. Data from Counterpoint Research suggested that the new lineup outsold last year’s iPhone model by 14% in the US and China. The new lineup includes the ultra-thin iPhone Air for the first time, though demand has reportedly been limited for that device (as was somewhat predictable).

Optimism is high going into Thursday’s earnings. On Tuesday, Apple became the third company ever to top $4 trillion in market capitalization. But if that enthusiasm is fueled at least in part by iPhone performance, investors on Thursday should be looking closely at product and geographic mix. Does the increase in share of entry-level models, as suggested by Counterpoint’s numbers, mean more consumers are opting for the cheaper model? And, perhaps most important, how much iPhone demand has been drummed up by “heavy” promotions in China and India, as suggested by UBS analysts on Monday? Flatter demand in the US would reignite worries that consumers are holding off on upgrading while Apple gets its AI features in order.

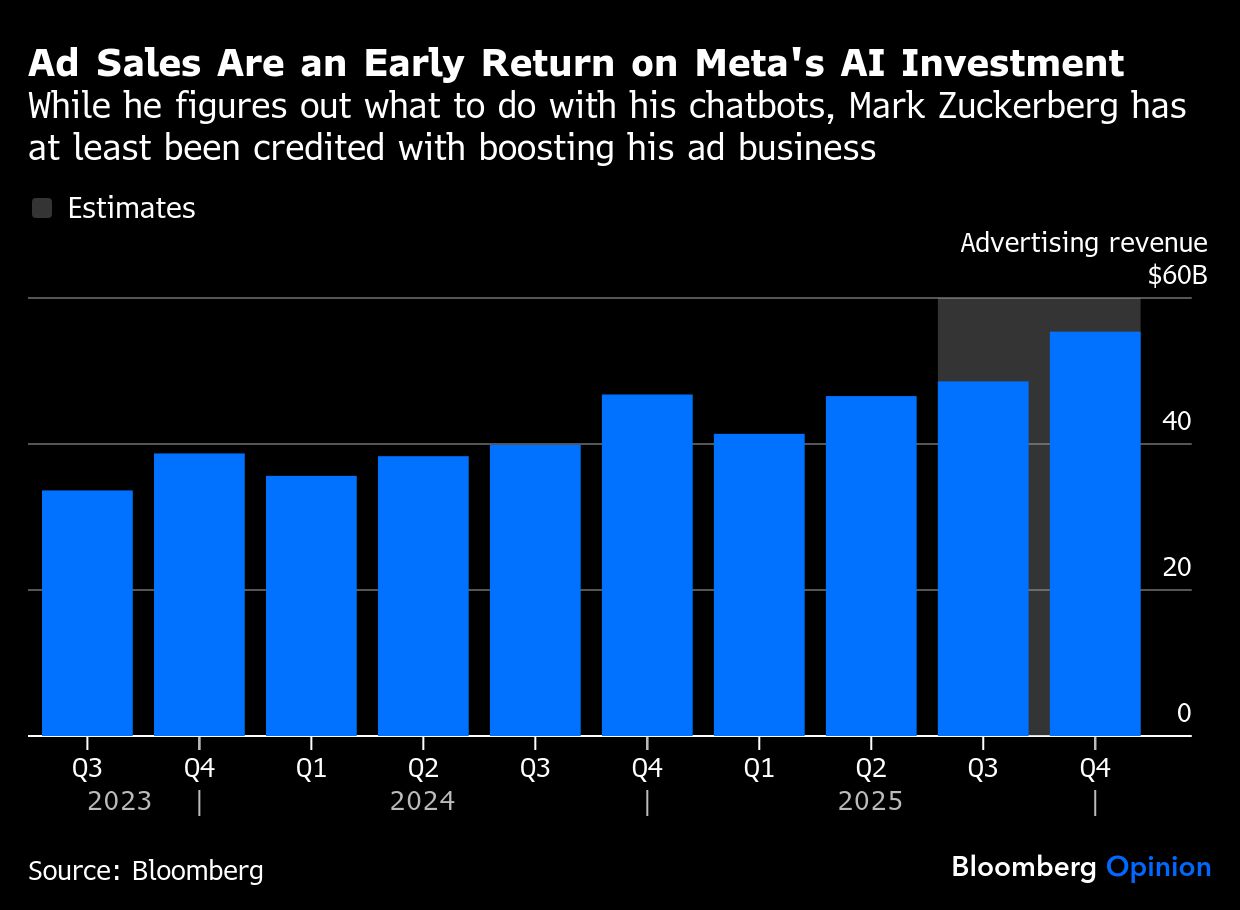

Will Meta’s advertising gains be enough of a distraction?

For as much as I’m unconvinced by Meta’s consumer-facing AI strategy — which so far largely consists of annoying bots crowbarred into its popular apps — its impact on its bread-and-butter advertising business can’t be ignored. Meta says it is using AI to help advertisers create ads but also better target consumers. Analysts are looking for $48.6 billion in advertising revenue for the quarter — a 22% boost from the same quarter last year.

Meeting those expectations will be the minimum required if it’s to fend off the more complicated questions it faces. As Minda Smiley of eMarketer puts it: “The company seems to be more focused on keeping up with the Joneses than thoughtfully determining how AI fits into its broader road map or considering the various implications of this technology.”

Meta isn’t struggling to prove its users are using AI — the company has made it almost impossible to avoid. But to what end, and with what business model in mind?

Bonus question: Might we see a shift in tone around the Metaverse? The Financial Times reported that a key executive has been moved from the Metaverse team to the one working on AI. I don’t think investors would hate the idea of a broader pullback on Zuckerberg’s obsession with mixed reality.

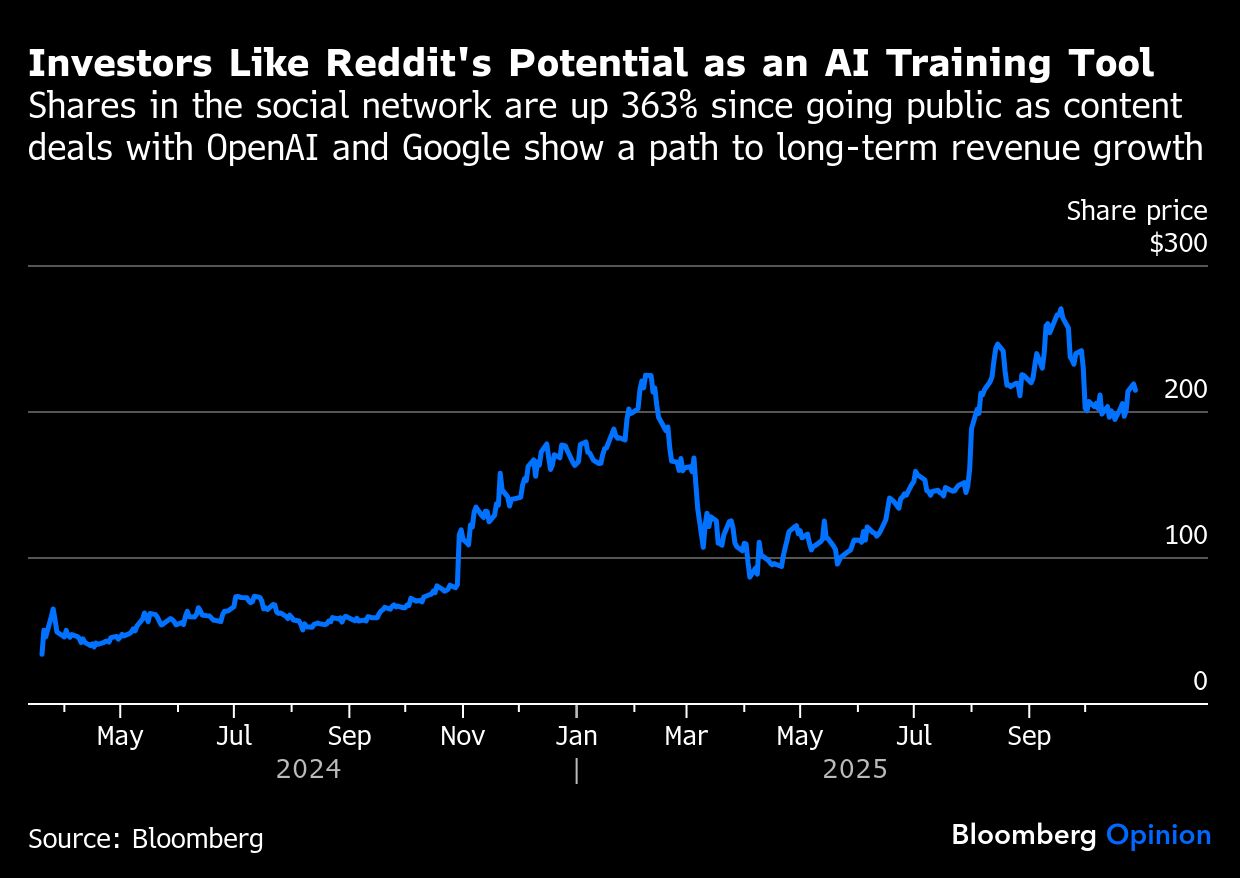

Does Reddit have enough takers for its data?

Reddit is not part of the Magnificent Seven and is much smaller than the others on this list, but as a new tech name in the public markets, its fortunes are being watched closely, so I’ve included it here.

Last week, faced with accusations that it was illegally scraping Reddit’s data, AI company Perplexity came out swinging. It said Reddit was suing because its business of selling content to AI companies was struggling as firms were “cutting back on deals with Reddit or walking away completely.” Whether that is true will be a focus for Reddit investors when it reports Thursday.

One part of Reddit’s success as a public company — its shares are up 363% since its IPO — has been the potential for it to sell its vast amount of user-generated content to AI companies. So far, it has struck deals with Google and OpenAI. But how many more will there be?

Reddit doesn’t break out its revenue from content deals, instead bundling it into an “other” category, which analysts expect to reach $36 million for the quarter. That represents about 7% of total revenue, with the rest coming mostly from advertising. But Reddit’s role as an engine room for AI development is seen as a big part of its growth potential — its prospects are brighter if Wall Street sees it as an AI stock rather than a pure-play social network.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Dave Lee