Imagine you recently set a goal to lose 10 pounds. At the moment, you’ve lost about 9 and you look and feel great, but your doctor warns you about an emerging nutrient deficiency that could lead to serious health complications if you don’t stop dieting. What should you do? This isn’t a trick question: You should take the win and not gamble on unintended negative consequences.

This is how the Federal Reserve should feel, too, after announcing Wednesday the imminent end of quantitative tightening, the process of letting maturing securities roll off its formerly bloated — but now relatively right-sized — $6.6 trillion asset portfolio. The development should address a series of yellow flags in money markets in recent weeks that seemed to heighten the risk of a financial accident, and it should stem any lingering concerns about liquidity in Treasury markets. To mitigate any minor inflationary consequences, policymakers should hold off on a further interest rate cut in December.

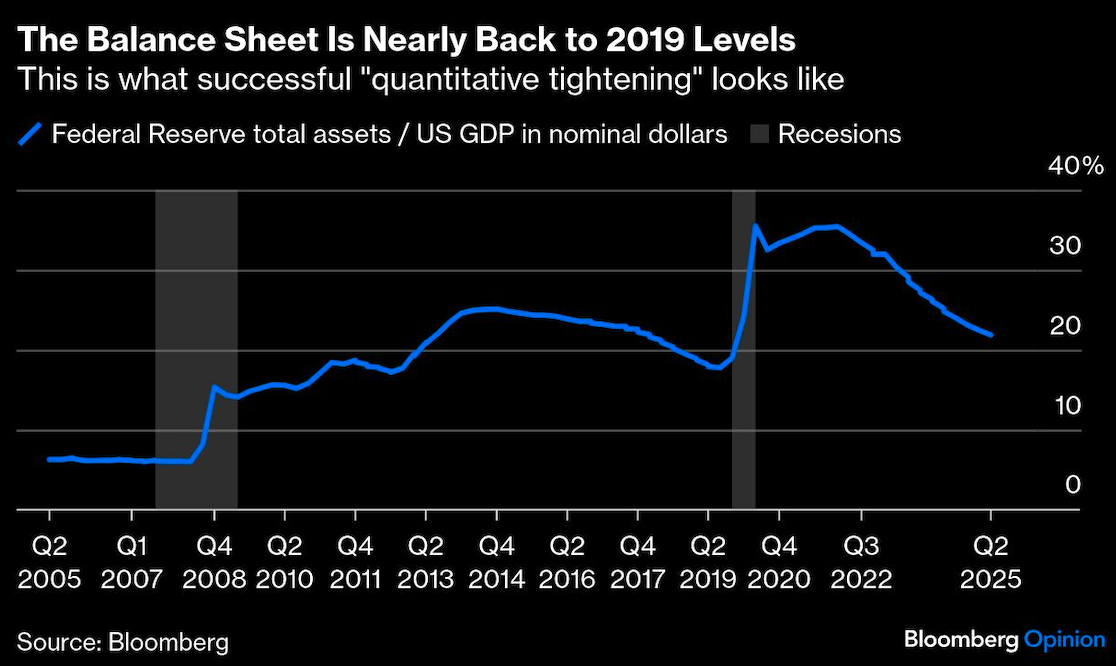

It’s important to remember that QT, at least in the current context, was never really a proactive policy. Rather, it’s the undoing of a policy — quantitative easing — that the Fed used to support markets and the economy during the Covid-19 pandemic. By that definition, success means getting back roughly to where we started and avoiding any catastrophic mistakes along the way. Even if we’re only around 90% to 95% of the way there, the costs of going too far are much greater than not going quite far enough.

There are also ways to mitigate the costs of stopping a bit early. While QT was never seen as the primary instrument for fighting inflation, some analysts have argued that the Fed’s balance-sheet runoff was the equivalent of one or two rate hikes. In practice, the Fed will now be reinvesting the proceeds from maturing securities into more Treasuries, leaving a slightly larger footprint in the fixed-income market.

Still, with the consumer price index up 3% from a year earlier, policymakers will have to be careful not to let financial conditions ease too far, especially after they cut the main policy rate 25 basis points on Wednesday to 3.75%-4%. I’ve advocated since the last inflation report for a pause in the rate-cutting cycle, and Wednesday’s decisions add further weight to that argument.

Next, the Fed can limit its footprint through changes to the construction its portfolio, as it looks poised to do after it ends QT on Dec. 1. While I don’t share all of her beliefs about the balance sheet, I appreciated Fed Vice Chair for Supervision Michelle Bowman’s suggestion in a September speech that the Fed move toward a System Open Market Account portfolio that “mirrors the broader Treasury market” and is, thus, neutral in its impact across the curve, rather than potentially favoring longer-run securities.

The committee appears to broadly agree. “We will continue to allow agency securities to run off our balance sheet and will reinvest the proceeds from those securities in Treasury bills, furthering progress toward a portfolio consisting primarily of Treasury securities,” Chair Jerome Powell said Wednesday. “This reinvestment strategy will also help move the weighted-average maturity of our portfolio closer to that of the outstanding stock of Treasury securities, thus furthering the normalization of the composition of our balance sheet.”

For some perennial critics of the Fed’s balance sheet, the end of QT is bound to spur a new round of handwringing. They blame the balance sheet for all the ills in markets and the economy, and they openly fantasize about a world in which the balance sheet returns not to pre-2020 levels but to those seen prior to the financial crisis. Specifically, they draw specious links between the balance sheet and inflation, asset bubbles and inequality. But they overlook the fact that the era of large balance sheets has — with the exception of the pandemic experience — been a successful period for central banking and the US economy. Since the advent of quantitative easing, the combination of inflation and unemployment (as measured by the “misery index”) has generally gotten better over time, not worse. The Fed is far from the failure that tin-foil-hat commentators would have you believe.

Clearly, there are valid risks from carrying a too-large balance sheet. First, it can sometimes cause the Fed to go through periods of large unrealized losses, as it has recently, when interest payments it made to the private sector exceeded those it received on its longer-dated asset portfolio. But those losses should balance out over the course of an economic cycle. Second and more importantly, a failure to shrink the balance sheet at all would leave the Fed with less fire power to conduct QE later when the next emergency comes along. Fortunately, that’s not a problem today.

Even those who would shrink the balance sheet much further have to face a practical reality: They may not be able to do so without causing a crisis, and even a small hiccup will cost the Fed its precious credibility. A couple of leading picks for Fed chair, Kevin Warsh and Bowman, are among those openly musing about a meaningfully smaller balance sheet. My bet is that they’d change their tune if they got the job and their reputations were on the line. Treasury Secretary Scott Bessent has also griped about the balance sheet in a pair of essays published last month, but I doubt he would put market and economic stability at risk to test his theories.

As former Fed Chair Janet Yellen famously described it, QT was supposed to be a non-event — “like watching paint dry.” Unfortunately for her, it ended up getting a little too exciting for comfort in 2019, the last time the Fed was trying to shrink the balance sheet after a period of quantitative easing. She had to wrap up QT in a hurry after some high-profile disruptions in repo markets where financial institutions help fund themselves.

By contrast, her successor, Chair Jerome Powell, appears to have pulled off the elusive nothing-to-see-here balance sheet runoff. That won’t end the incessant conspiracy theories about the Fed’s large portfolio, but you can’t please everyone and there’s no point in trying. Better to play it safe and conclude what, for the time being, looks like a successful operation.

A message from Advisor Perspectives and VettaFi: Thinking about starting your own RIA, making a move to a different firm, or specializing in a new area? Read our latest articles on financial advisor transitions.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin