The question of the moment in markets is whether we are in an AI bubble, as stocks seem awfully expensive amid hopes that artificial intelligence will transform the economy. But there is another curiosity that is far more concerning: low credit spreads. That suggests a low-risk environment — which describes precisely nothing about this market.

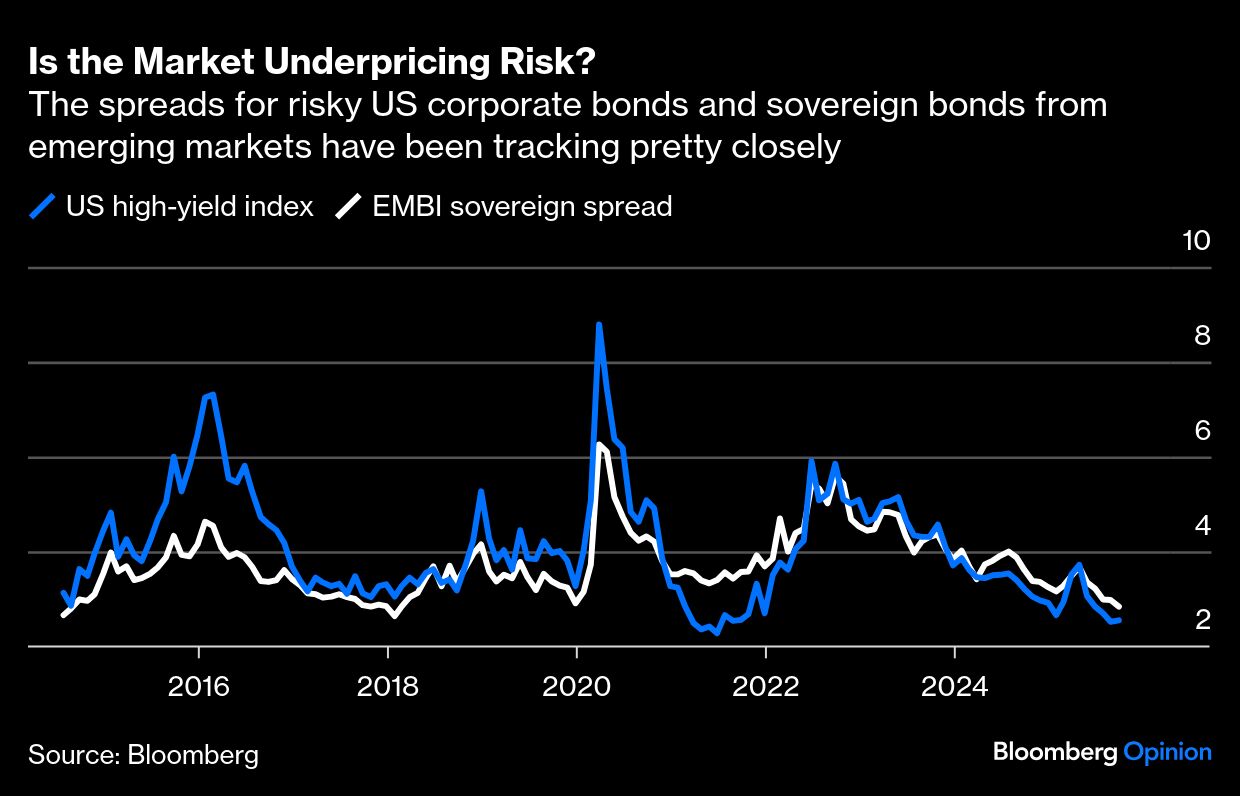

The credit spread is a measure of the difference in yield between high- and low-risk bonds. Risky debt is normally low-rated corporate or emerging-market bonds. Both tend to trade at a much higher rate because there is a higher risk of default or future volatility. And yet spreads on risky corporate debt are low by historic standards.

That means one of two things: Either these bonds aren’t so risky — or markets are underpricing risk. That second scenario never ends well.

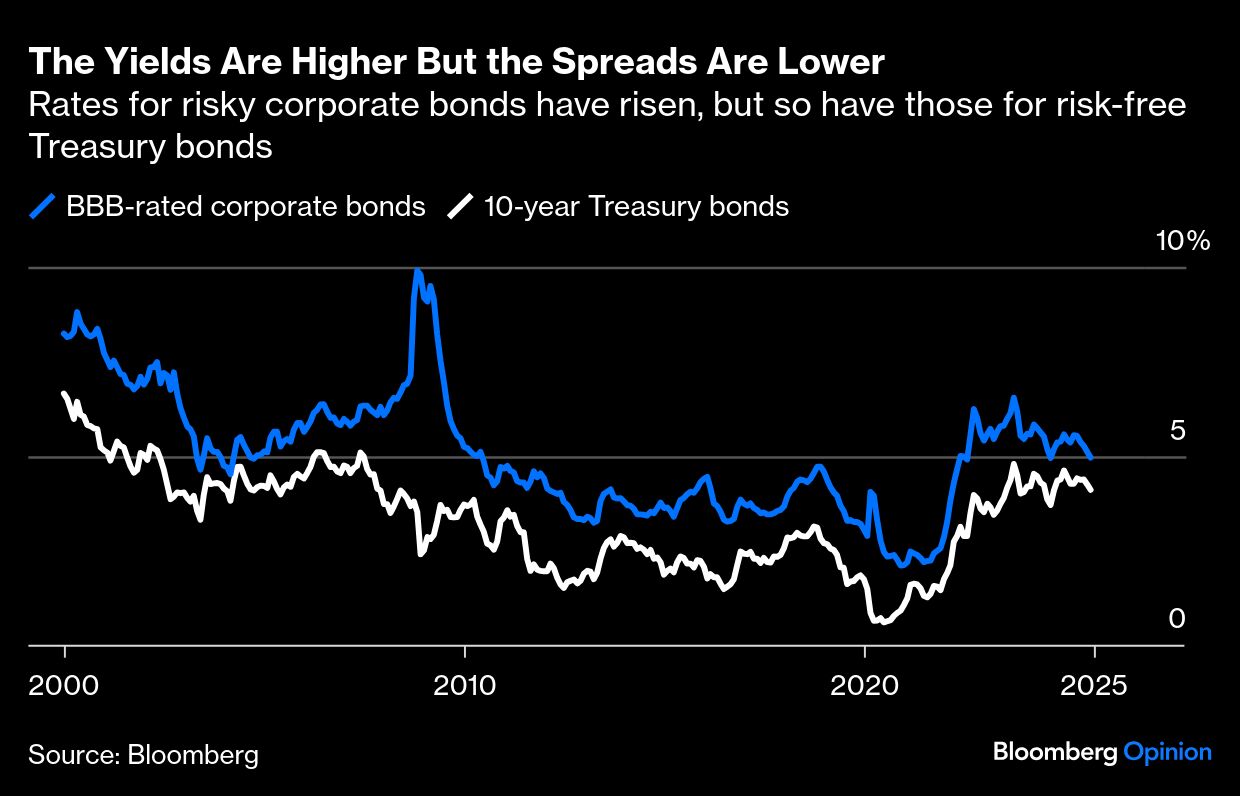

To be sure, there are reasons not to worry, or to worry for a different reason. The yields on these bonds are higher than they were several years ago; it’s the difference between them and the low-risk bonds that is smaller. And that’s because risk-free bond yields, such as a 10-year Treasury, are much higher.

This could be because risk-free bonds aren’t looking so safe anymore. Not only is the US government taking on a lot of debt, but the future of trade, inflation and the dollar looks uncertain. All of that increases bond yields. It’s also possible that the difference between risky and risk-free just isn’t as meaningful as it used to be, so the credit spread isn’t the measure of risk that it once was.

Another potential explanation for the low credit spread is the rise of private credit. As credit-cycle finance guru Edward Altman has noted, the growing size of the private credit market means that much more capital is chasing risky bonds, which is a factor in decreasing spreads. It could also be that firms that are less well suited for public markets may be seeking credit from private lenders, leaving relatively stronger borrowers. A big influx of foreign buyers of debt, seeking higher yields, has also added to demand.

Yet none of this is entirely reassuring. First, while spreads may be low, firms face a higher cost of borrowing, and many borrowers have not yet had to refinance. When their debt reaches maturity in the next two to three years, they will face higher debt payments. Weaker firms will have a harder time servicing their debt and risk bankruptcy.

In fact, bankruptcy rates and leverage are already rising. Some companies with private loans can’t make their debt payments and are rolling them into their principal. The market will eventually have to come to terms with the fact that the rates of the 2010s aren’t coming back, possibly triggering more bankruptcies.

Another indicator is that credit spreads and the VIX, a measure of stock risk, have slightly diverged recently. The VIX is now increasing more than spreads.

All this suggests that risk may be underpriced — and all things considered, underpriced risk in debt markets is more dangerous than a stock-market bubble. When equities crash, people lose money. In a debt crisis, payments aren’t made, collateral becomes worthless, and firms go bankrupt.

A big reason that spreads are so low is the same reason that the price of gold went up: There is a lot of demand and a limited supply. As long as that is true, the price of risk will continue not to make sense, encouraging even more leverage.

This can go on for a while — but not forever. One day the demand for risky bonds will fall, perhaps because dollar-denominated assets become less attractive, or a wave of bankruptcies scares investors. And then things will get pretty gnarly pretty fast.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.