Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Introduction

U.S. stock buybacks are on track for a record in 2025: estimated at $1.2 trillion according to JP Morgan, with expectations of surpassing $1.8 trillion in coming years [Bloomberg 2025]. This dwarfs new equity issuance through IPOs and secondary offerings and represents 2% – 3% of U.S. equity market capitalization — 50% to 100% more than the annual payout from dividends.

Buybacks raise important questions. Foremost amongst them are whether, and how much, buybacks push up stock prices, and whether they create other distortions relevant to investors and public finances. This article explores these questions by drawing on economic theory and broadly held views of real-world investor behavior.

Central to our analysis is estimating the impact of buybacks assuming investors follow some combination of these three common, real-world approaches to asset allocation:

- fixed weight,

- dynamic driven by expected cash-flow, and

- dynamic driven by past returns (we’ll refer to this group as extrapolators or return-chasers).

Buybacks in Theory

Franco Modigliani and Merton Miller laid down some of the cornerstones of modern corporate finance in the late 1950s. The most relevant of the Modigliani-Miller propositions for our purposes is their result that, given certain assumptions, payout policy through dividends and buybacks shouldn’t affect the enterprise value of a firm, which instead should be driven by the firm’s earnings and assets. They and their followers also showed that dividends and buybacks should be exactly equivalent.

These results only strictly hold under a strong set of assumptions, including frictionless and complete markets, rational investor behavior, and neutral tax treatment between dividends and capital gains. These assumptions are clearly not uniformly true in practice, as we’ll discuss below — nonetheless, Modigliani-Miller remains a useful starting point for expectations around the impact of dividends and buybacks.

Why Executives Love Buybacks

In practice, executives favor buybacks for several reasons:

-

Flexibility: Executives believe that reducing dividends invites sharp market penalties compared to scaling back the pace of buybacks.

-

Tax efficiency: U.S. taxable investors can defer realizing gains from buybacks, often avoiding taxes altogether through deferral or stepped-up basis treatment. By contrast, dividends face an immediate top marginal rate of 24%. Buybacks are also more tax-efficient for non-US investors, who are subject to 15% – 30% withholding tax on dividends but no tax on capital gains.1

-

Share price support: Although rarely stated explicitly, executives are aware that buybacks can boost stock prices, aligning with incentive structures (i.e. increasing management compensation). In general, executive stock option awards would be worth less if companies returned funds to shareholders by paying higher dividends versus doing share buybacks.2

Market Impact of Buybacks

As described above, theory suggests that buybacks shouldn’t impact stock prices under the Modigliani-Miller assumptions because, while the count of shares is reduced, the firm also has less cash because of the buybacks and these effects exactly offset each other. In effect, it is assumed that shareholders value companies as a sum of their parts, and in particular that they value cash in the company or in their hands the same.

Empirically, however, there’s strongly suggestive evidence that buybacks do impact stock prices, and there are a number of models which can explain why this might be the case — all of which rely on investors not being fully rational. An important assumption of these models is that, to some extent, if the companies did not buy back their shares, then that cash would either be retained and productively invested by the companies or paid out as extra dividends which investors would either consume or keep in a higher allocation to fixed income, rather than reinvest in shares of the companies.

The “endowment effect” is a cognitive bias described in behavioral economics, whereby people demand more to give up an owned item than they would be willing to pay to acquire it if they did not own it. In the buyback context, it suggests that investors would accept a lower fraction of equities in their portfolio if cash is returned to shareholders through dividends versus buybacks. Investors are likely to demand a higher price to sell their shares into a buyback than the price they’d be willing to pay to buy new shares with extra dividends.

Given these assumptions, the impact of buybacks on share prices arises from many investors using incomplete heuristics to determine how much of an asset they want to hold. For example, if they want to hold a constant proportional amount of some asset, and the available amount of the asset is reduced, the only way this can be accommodated is for the price of the asset to go up.

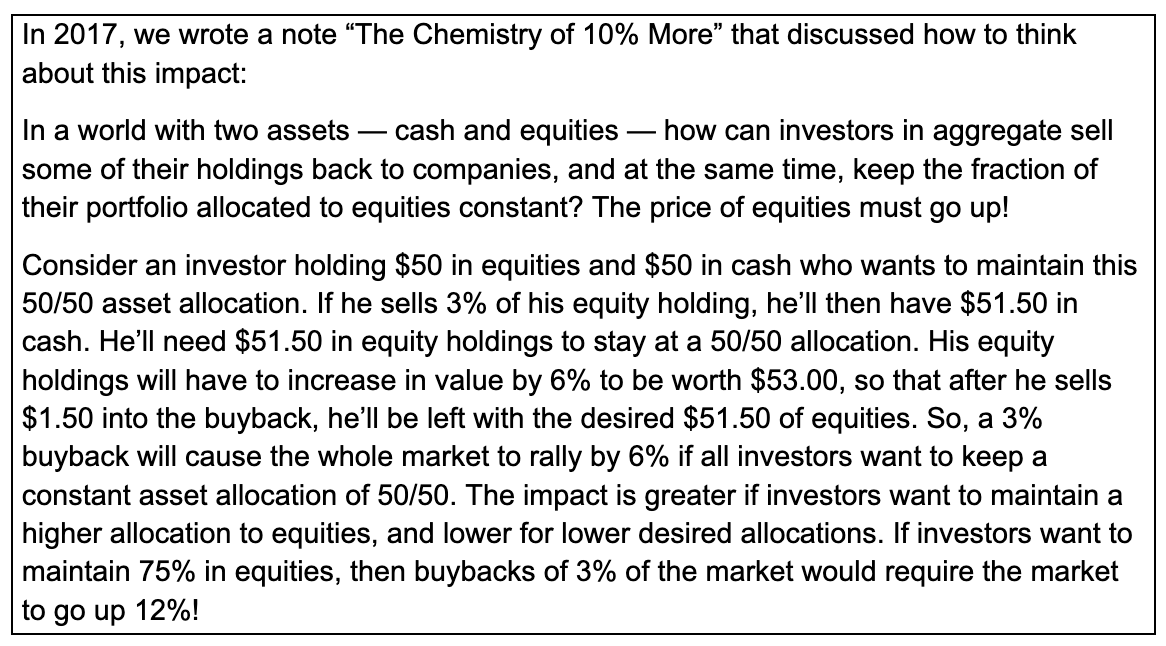

To estimate the price effect of large-scale buybacks, consider three types of “model” investors:

-

Fixed-weight allocators (e.g. 50% equities / 50% other assets): To absorb 3% of stock repurchases, prices must rise ~6%.

-

Expected cash-flow driven allocators: Adjust holdings based on expected return. For them, a ~1% price rise suffices, because they will want a proportionately lower allocation to equities as their long-term return declines due to the market price going up.3 These “fundamental” investors increase stock market price elasticity relative to the other two types of investors described above and below.

-

Return-chasers: These investors extrapolate past returns into the future, increasing their demand for equities as prices rise. We can’t sensibly assume that all investors are return chasers, because then buybacks would set off a never-ending rising price spiral. However, if we assume that about one-third of investors are return chasers (and 1/3 each the other two types) then buybacks could push prices up ~7%.4

These model investors can exist in different combinations, operate over different time horizons, and have complex multi-year effects with one another. While finance theory would suggest most investors are Type 2 “expected cash-flow allocators,” we believe that in reality the preponderance of investors are of Types 1 and 3. Fixed-weight asset allocators are probably the most common investor type, considering the trillions of dollars invested in target date funds, balanced funds, and in endowments, pension funds and foundations who very infrequently change their asset allocation.5 Putting this all together and simply looking at the range of results without fully considering all of the possible interactions, we can see how buybacks on the order of 3% could plausibly push up prices by 3% – 5%.

It is interesting to note that over the past ten years, the US Price-Earnings multiple has increased by 4% per annum. The 3% – 5% per annum potential impact of buybacks provides one explanation of this increase.6

Other Estimates

One much-cited academic perspective comes from Gabaix and Koijen (2023), who argue that stock markets are “inelastic,” so relatively small shifts in demand can move prices dramatically. They estimate that every $1 of buybacks moves the market up by $5!7 Also see Barberis et al. (2015) and Haghani and White (2017) for earlier explorations of these effects.

For an alternative practitioner perspective, hedge fund portfolio managers we’ve spoken with often base their estimates of market impact on share of daily trading volume. A common rule of thumb they use is from Grinold and Kahn (1999), and discussed and connected with other models of price impact in Bouchaud (2022):

The parameter k is usually set to 1. Stock buybacks running at around $1.5 trillion per year represents about $6 billion of buying each day, which is close to 0.5% of daily equity trading volume. Stock market daily price volatility is about 1%, so the impact from this formula would be about 0.07% each day, or about 20% per annum!

We think both of these estimates of buyback price impact are too high, though they can be lessened in increasingly realistic models which incorporate factors such as a decay of the price effect over time. However, while the precise magnitude of impact is uncertain, the consensus is that buybacks can exert significant upward pressure on stock prices.

No Free Lunch

And yet, buybacks are not a panacea which can deliver permanently higher investor welfare. In our view, it’s surely right that the enterprise value of a stock is derived from its earnings and assets, and stock price dynamics which don’t increase earnings or assets can’t increase the ultimate benefit investors derive from stock ownership. In our note Unexceptional US Stock Market Earnings?, we discuss how companies can’t just “surf” GDP growth without also reinvesting earnings. Thus, to the extent buybacks are a substitute for reinvestment rather than dividends, they may in fact be decreasing future earnings and long-term investor welfare.

One consequence of this earnings-centric perspective is that if buybacks raise stock prices, they must also lower forward-looking expected returns, thus resulting in neutral long-term investor welfare.

Potential Distortions Between Individual Stocks

Direct stockholders

Investors in individual stocks will tend to require a premium to the market price of the buyback stock that prevailed before the buyback was announced or executed, and indeed there is some evidence of buyback-heavy stocks having excess returns [Bloomberg 2025]. It is likely that the predictability of stock buybacks invites some front-running by astute trading firms and hedge funds. To the extent such trading firms make attractive risk-adjusted returns from buybacks, the likely losers are the stock-picking investors who sold too early. We suspect that over time, competition among trading firms will erode such profits, but not completely.

Investors who hold stocks directly and do not sell into buybacks find themselves increasingly overweight in buyback-active companies relative to benchmarks. Over time, this heightens portfolio idiosyncratic risk — often evading investors’ notice.

Index fund investors

Market-cap weighted index funds must rebalance as companies repurchase shares. This results in selling stock in companies doing buybacks and reallocating into companies not doing buybacks (or doing less buybacks). Note that market capitalization weighted index funds are behaving as theory would predict, willing to sell into buybacks at the prevailing market price. To the extent their activity has impact on relative stock prices, they will be pushing non-buyback stocks higher relative to buyback stocks, countering the impact of stock-pickers requiring a premium to sell their shares into buybacks.

Practitioners and researchers, such as Gabaix and Kroijen (2023), find that the price elasticity of individual stocks is greater than that of the the overall stock market. They explain this finding by noting that Apple and Microsoft are likely viewed as closer substitutes than the overall US stock market versus the total US bond market. We would add that the prevalence of index funds also can reduce price impact between stocks, at least in the case of buybacks.

Cyclical Risk

Buybacks are highly pro-cyclical. They surge in bull markets and collapse in downturns—falling by over 50% in 2008 and 2020. This cyclicality can amplify both rallies and declines, exacerbating volatility. Looking ahead, large-scale equity issuance (e.g., from capital-intensive AI firms raising trillions for infrastructure) could have the reverse effect of today’s record buybacks, increasing supply and pressuring valuations.

Tax and Policy Implications

Buybacks are also a tax policy issue:

U.S. taxable investors: Benefit from deferral and favorable treatment of capital gains versus dividends.

Foreign investors: Avoid 15–30% U.S. dividend withholding tax, meaning the Treasury collects nothing when capital is returned via buybacks.

Revenue impact: If one-third of U.S. equities are held by U.S. taxable and foreign investors, foregone revenues amount to $100–150 billion annually [Tax Policy Center 2024].

This helps explain why Congress imposed a 1% excise tax on buybacks in 2022, with proposals to raise it further. Policymakers argue this offsets revenue losses and curbs distortions created by large-scale repurchases.

Connecting the Dots

Estimating the market impact of buybacks, or indeed any shifts in the supply and demand of stocks, is an area where theory and practice have not come to agreement. In researching their 2023 article, Gabaix and Koijen asked about 300 economists: “If a fund buys $1 billion worth of US equities, slowly over a quarter, how much does the aggregate market value of equities change?” The median answer they received was about 1/500th of their estimate of $5 billion and about 1/100th of ours. That’s a pretty big difference of opinion!

Our analysis of buybacks rested on the behavior of three types of investor, all of whom were assumed to be less than fully rational. Our discussion left out an important fourth investor type – fully rational investors who make their decisions based on predictions of what less-than-fully rational investors will do. Researchers have long believed that these rational investors will tend to destabilize markets by exacerbating the impact from exogenous supply and demand shocks, such as buybacks.

For example, see DeLong, Shleifer, Summers and Waldman’s 1990 article, “Positive Feedback Investment Strategies and Destabilizing Rational Speculation.” Indeed, perhaps one explanation for the extraordinary financial success of quantitative trading firms, such as Jim Simon’s Renaissance Technologies Medallion fund, is their understanding of the behavior and interaction of the investor types described herein.

In practice, we believe there’s compelling evidence that buybacks:

- Increase equity prices, possibly explaining part of the remarkable returns delivered by U.S. stocks over the past several decades in absolute terms, and also compared to the rest of the world. The resulting increase in prices, and consequently in price-earnings ratios, translates into lower long-term expected returns for investors.

- Create distortions and frictions for index funds and direct investors.

- Amplify cyclicality, boosting bull markets and deepening bear markets.

- Erode U.S. tax revenues, benefiting both domestic taxable investors and foreign shareholders at the Treasury’s expense.

In sum, buybacks are not a neutral corporate finance choice but a force shaping market dynamics, investor welfare, and fiscal policy. Their rise since the 1990s may be one of the most under-appreciated drivers of U.S. equity market performance and warrants greater attention from academics, investors, and policymakers.

Further Reading and References

- Barberis, N., Greenwood, R., Jin, L., and Shleifer, A. (2015). “X-CAPM: An extrapolative capital asset pricing model.” Journal of Financial Economics.

- Bouchaud, JP. (2022). “The Inelastic Market Hypothesis: A Microstructural Interpretation.” arXiv.

- Brosy, T., & Rosenthal, S. (2024). “What is the U.S. Tax Advantage of Stock Buybacks over Dividends?” Tax Policy Center.

- DeLong, B., Shleifer, A., Summers, L. and Waldmann, R. (1990a). “Noise Trader Risk in Financial Markets.” Journal of Political Economy.

- DeLong, B., Shleifer, A., Summers, L., Waldmann, R. (1990b). “Positive feedback investment strategies and destabilizing rational speculation.” Journal of Finance.

- Gabaix, X., & Koijen, R. (2021). “In Search of the Origins of Financial Fluctuations: The Inelastic Markets Hypothesis.” NBER and SSRN.

- Grinold, R. and Kahn, R. (1994). Active Portfolio Management: A Quantitative Approach for Producing Superior Returns and Controlling Risk. McGraw Hill.

- Haghani, V. and White, J. (2017). “The Chemistry of 10% More.” SSRN.

- Haghani, V. and White, J. (2024). “Leverage It or Leave It? Making Sense of Turbo-charged ETFs.” SSRN.

- Lou, D. (2012). “A Flow-Based Explanation for Return Predictability.” The Review of Financial Studies 25 (12).

- Shleifer, A., and Summers, L. (1990). “The noise trader approach to finance.” The Journal of Economic Perspectives.

- Stamm, L. (2025). “JP Morgan Sees Record U.S. Buybacks Jumping by Another $600 Billion.” Bloomberg.

-

“S&P500 Q2 Buybacks Press Release”. S&P Dow Jones.

- Wigglesworth, R. (2025). “Lunch with the FT: Investor Jean-Philippe Bouchaud: ‘The whole bull run is because of an influx of money.’” Financial Times.

Endnotes

1 Though U.S. company executives rarely cite this benefit to foreign investors as a reason for buybacks.

2 Furthermore, that executive stock compensation is generally based on share price and not market capitalization creates incentives to return capital to shareholders by foregoing marginally positive net-present-value projects or through issuance of debt.

3 These investors are not acting fully rationally, though their heuristic is more complete than that of the fixed allocators. The Modigliani-Miller framework would suggest that these return- and risk-driven investors will not want to change their allocation to stocks after the return of capital through buybacks (or dividends) as their exposure to the risky earnings stream of the market remains constant without needing prices to move or to do any trades. The assumptions we used to come to the 1% impact from 3% buying is a starting allocation to equities of 25%, given a 3.5% expected real return and 1.5% risk-free rate. After a 3% buyback, they now have a 24.5% equity allocation, which is optimal for a lower risk premium of 1.96%. That risk premium is achieved by prices going up by 1.2%.

4 Lots of assumptions need to be made around how return chasers form their updated expected returns based on past returns. In this case, we’re assuming that a 1% rise in stock prices leads return chasing investors to increase their forward looking expected excess return by about 8%, e.g. from 4% to 4.32%.

5 And when they do, they seem to be as likely to be changing due to an extrapolation of historical returns as based on changes in future cash-flow based returns.

6 From US stock market data provided by Robert Shiller The US multiple expansion over these years of heavy buybacks is even more remarkable considering that the real yield of US 10-year TIPS increased from around 0.5% at the start of the period to around 1.7% today.

7 And also that the effect can be quite long-lasting unless buybacks are expected to be quickly reduced in the future.

This is not an offer or solicitation to invest, nor are we tax experts and nothing herein should be construed as tax advice. Past returns are not indicative of future performance.We are grateful to Dave Blob, Aneet Chachra, Richard Dewey, Larry Hilibrand, Sudi Mariappa and Steve Mobbs for their valuable comments and discussion, and to Vladimir Ragulin and Jeff Rosenbluth for their comments and collaboration on our ongoing research into multi-agent market models. As always, thank you to our partner Jerry Bell for his help in shaping our thoughts and to Steven Schneider for pulling us through the last mile. Finally, thanks to Perplexity AI for the final proofreading of the article.

Victor Haghani is founder & CIO of Elm Wealth, a Philadelphia-based asset manager. James White is Elm Wealth’s CEO.

Learn more at www.elmwealth.com.

A message from Advisor Perspectives and VettaFi: Are you backed by institutional quality bond funds? Click here to learn more.

Read more articles by James White, Victor Haghani

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.