Bank of America Corp. and Morgan Stanley exposed a stock market puzzle on Wednesday. Both reported record third-quarter earnings following roaring results from rivals the day before. The stock market rewarded the two banks and Citigroup Inc. after their results, but not Goldman Sachs Group Inc. and JPMorgan Chase & Co.

The divergent response wasn’t just because the chief executive officers of JPMorgan and Goldman made downbeat comments on credit risks and overexuberance on Tuesday. It was more to do with the huge gap in valuations between the banks, especially the two playing catch-up — Bank of America and Citigroup. Morgan Stanley stands out for its greater defenses against financial panics and crashes than the rest, although no one will be immune if there is a bubble in artificial intelligence or credit that bursts.

Wall Street boomed in the third quarter. It was the busiest three months for new share listings since 2021 and brought a flurry of takeover deals alongside very active trading. Almost everything ran hot.

Bank of America reported a 14% jump in equities trading revenue versus the same period last year to nearly $2.3 billion, its highest ever for a quarter. Its total revenue for all trading and investment banking fees hit a record, too, just topping the previous high in the first quarter of 2021.

Meanwhile, Morgan Stanley reported its best-ever quarterly top line at $18.2 billion, up 18.5% year on year, and a record quarterly return on tangible equity at 23.5%. Its total revenue across investment banking and markets came in at $8.39 billion, within a whisker of its previous highwater mark of $8.45 billion in the first quarter of 2021.

What will really raise cheers on the bank’s trading floors is retaking the lead in equities from Goldman — its revenue jumped 35% year on year versus Goldman’s 7% gain. Lending to hedge funds played a big part, and although Morgan Stanley doesn’t break out numbers for prime brokerage like Goldman, it said the unit produced record results.

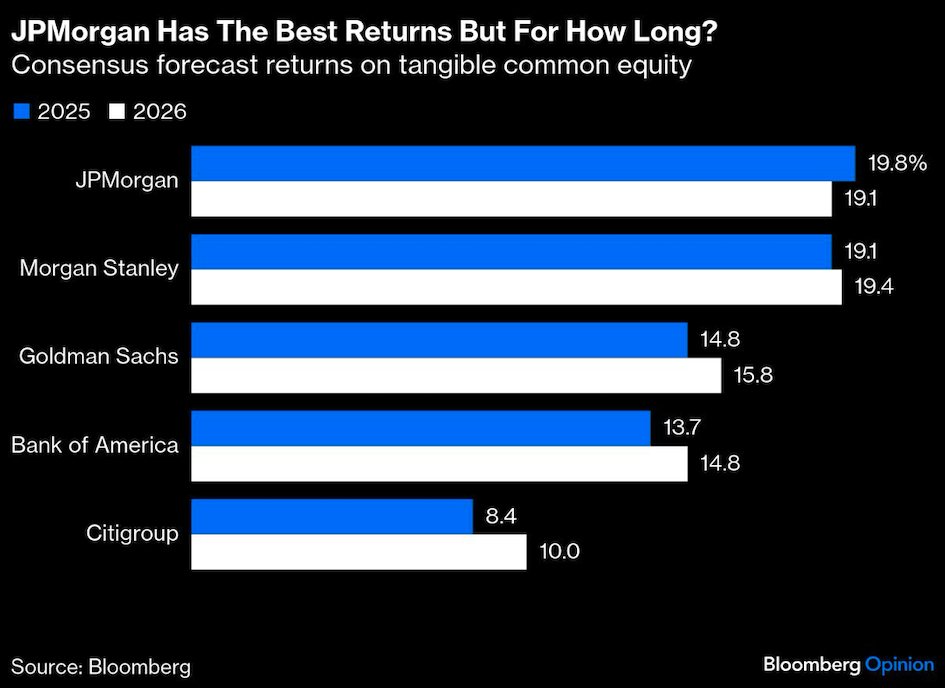

Morgan Stanley’s shares jumped 7% in morning trading making it the most highly valued stock of the big five banks on multiples of both forecast earnings and book value. At 17 times forward earnings, it is now well ahead of JPMorgan’s 14.9 times and Goldman’s 14.5. Bank of America and Citigroup lag some way behind on 12.7 times and 10.6 times, respectively.

Morgan Stanley has made its business less vulnerable to sudden stops in dealmaking and initial public offerings by building its wealth and asset management divisions over the years. These typically account for more than half its revenue in any given period. Investors have fully bought into the idea that Morgan Stanley will keep gathering assets, and its revenue and profits will keep compounding.

At JPMorgan, the wealth businesses only bring in about 15% of revenue. Most of the rest is split fairly evenly between consumer banking and the corporate and investment bank side. Consumers can be just as volatile as markets and deals, but one of CEO Jamie Dimon’s long-term bets is that they often move in opposite directions and counterbalance each other.

Morgan Stanley isn’t totally invulnerable to the stock market tumbling or free-flowing credit causing nasty accidents. Anything that cuts the value of clients’ assets automatically hits wealth management fees charged on a percentage basis, too. And in equities trading, if markets tumble or hedge funds cut the leverage behind their bets for some reason, prime brokerage balances will fall and the interest and fees Morgan Stanley earns will drop, too.

Goldman is spending nearly $1 billion to buy a venture capital firm, Industry Ventures, to add more heft to its alternatives business, but it still has a way to go to rebalance like Morgan Stanley. JPMorgan, meanwhile, is so big that it’s hard to find any additional business that really moves the needle without worsening returns or taking unnecessary risks.

At the other end of the scale, Citigroup continues its slow-moving recovery. Analysts forecast it will only just reach a 10% return on tangible equity by the end of 2026. Still, it is coming from such a low base that its shares are the best performing of the five banks over the past year.

Bank of America is a different kind of puzzle. It may be that CEO Brian Moynihan’s mantra of steady, responsible growth has left investors cold. The bank will hold its first investor day in years next month to try and convince them that it’s more exciting than they realize. That will be a tricky circle to square. Its trading business, for example, has already been growing strongly, especially in financing hedge funds and other leveraged investors. That’s gone well so far, and the last thing Moynihan should do is ease up on the responsible-growth idea when markets are in danger of turning truly frothy.

If a bubble is going to burst, Goldman and JPMorgan could suffer from the hits to investment banking and trading, where they are both big leaders, with less room to grow easily elsewhere. Morgan Stanley will definitely lose revenue, too, but unless something nasty emerges in its books, it looks like investors are justified in treating it as their bank for all seasons.

A message from Advisor Perspectives and VettaFi: Stay ahead of market changes with our daily updates on key market and economic indicators. Visit the AP Charts and Analysis site for our expert insights.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul J. Davies