I studied economics at the University of Edinburgh, which meant reading a lot about the economic history of Northern Britain — and that, in turn, meant reading a lot of Joel Mokyr, who is one of three economists who won the Nobel prize on Monday. Later on, as I embarked on my career as an economist, I got to know him personally, and his newer research continues to shape my understanding of growth.

Whenever I feel uncertain about the future of the economy, I turn to Mokyr. His work is the foundation of my understanding of why some economies thrive, some stagnate and others decline. It offers both hope and a warning to countries navigating the current economic uncertainty, and sheds some light on big questions about the effect of artificial intelligence and the viability of the Chinese model. As an admirer of his work and in honor of his Nobel, I thought I would offer the five most important lessons of Joel Mokyr.

Growth is often resisted. Economic growth has been critical to prosperity — it is why people live longer, more comfortable lives that are free from the drudgery of hard labor. But it is often resisted, because it involves upheaval and uncertainty.

Mokyr once explained to me how, at first, men refused work in factories. They were used to working for themselves, as small-scale farmers or artisans, even though they were poor and it was not an easy life. It was what they knew. The concept of modern work — being somewhere at a certain time, staying all day, taking orders from a boss you had no relation to — was so offensive and demeaning to men that for years factories had to hire women and children. It took a few generations of social conditioning for men to make the transition.

Growth takes time. Industrialization was made possible by a few key innovations that changed the nature of work and production. But there were critical inventions that no one knew what to do with at first, such as the steam engine, which powered factories and made industrial production possible. It took more than 100 years for its contribution to even show up in productivity statistics.

Often the most pivotal inventions take years to find their best use, and in ways no one could have predicted. It is true the speed at which innovations get adopted gets quicker each year. It’s also true that there are inventions that currently exist that will have a huge impact on the world many years from now.

Growth is unpredictable. New innovations destroy jobs, but they also create new ones — and it is fruitless to try to anticipate what the new jobs will be. Innovations transform the economy in ways that are impossible to comprehend (see above). As Mokyr once told me: “Imagine explaining to someone in 1920 what a cybersecurity expert is.”

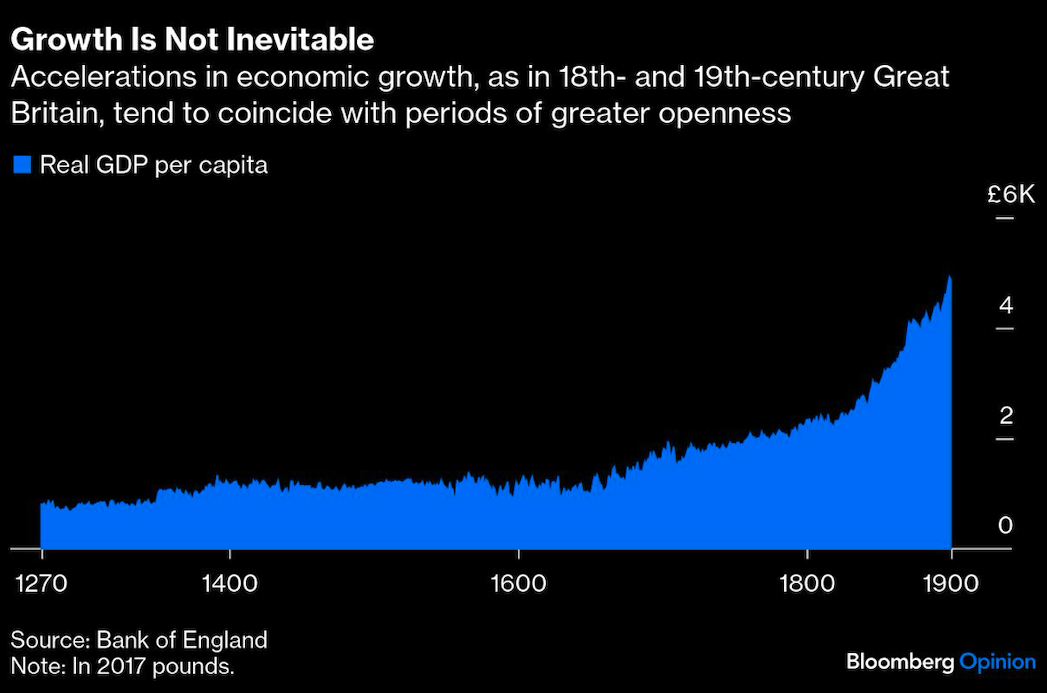

Growth is cultural. One question drove economic history literature for decades: Why was Great Britain the first country to industrialize and get rich? Other countries were also inventing things, or had more wealth and natural resources, or a better climate.