The boom in capital expenditures related to generative artificial intelligence is generating lots of questions about whether it is sustainable. Coming up with definitive answers to them is something of a fool’s errand. Quantifying the size of the capex surge seems like a more productive endeavor — and one that may offer some hints as to its sustainability.

Even that is easier said than done. After spending the better part of three days making chart after chart after chart (a small sample of which I share here), I now know that there are many different ways to quantify the AI capex boom that lend themselves to many different narratives. My general sense after this exercise is that although AI spending has reached the point of major economic significance it has yet to become quite the force that tech and telecom were in the late 1990s. Yes it is driving a large share of current US economic growth, and if it were to end suddenly there would be unpleasant consequences, but at this point there’s nothing especially alarming. At a few big tech companies, though, the spending is like nothing they’ve ever attempted. Either it pays off, or there will be some very challenging years ahead.

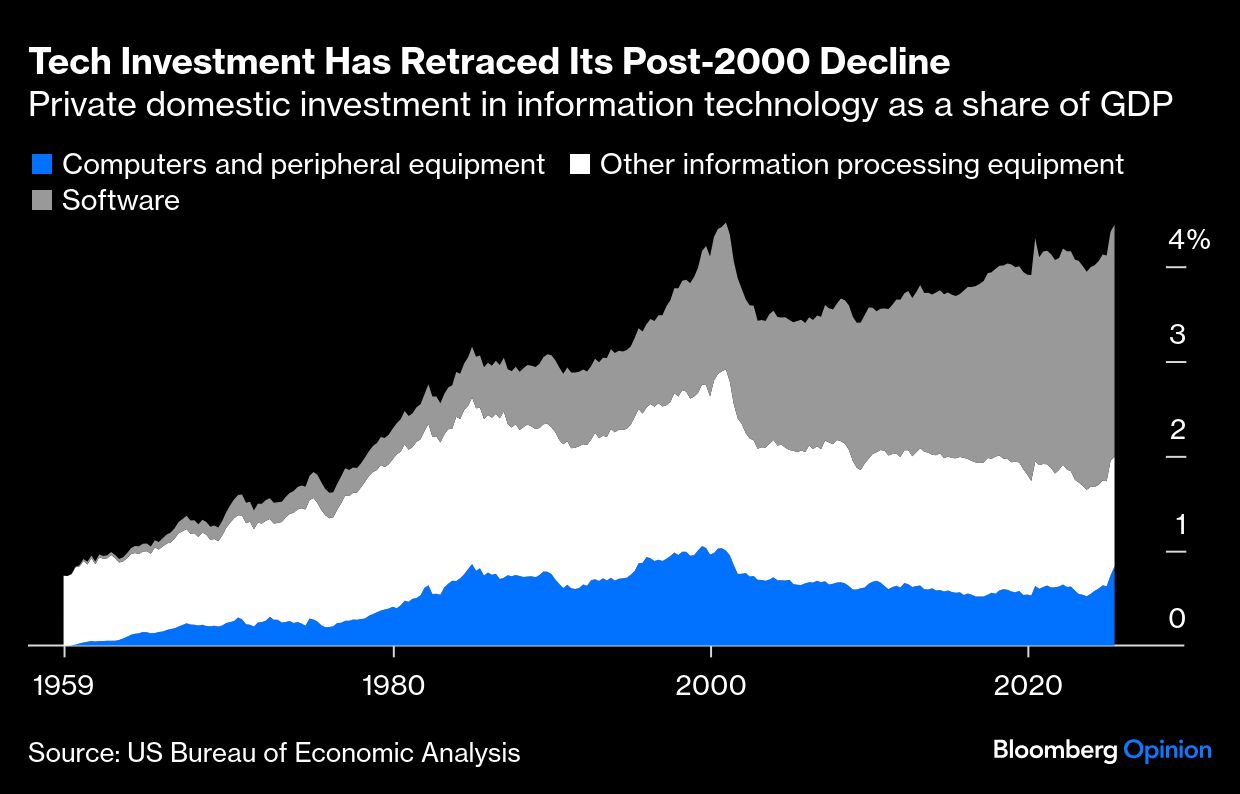

Here’s a top-down view from the most recent gross domestic product data released late last month by the US Bureau of Economic Analysis. Private domestic investment in information processing equipment (split here between computers and peripheral equipment and the rest) and software was 4.4% of GDP in the second quarter, just below its 4.6% peak in the final quarter of 2000. If the pace of increase over the past two quarters were to continue, it would leap past that by the end of this year — but wouldn’t be out of line with the long-run trend of increasing tech spending.

This includes a lot of spending on things not directly related to AI, while excluding some AI-related spending on research and development, which I chose to leave off because it includes R&D in pharma and other industries and its share of GDP has been flat for the past five years. In July, Jens Nordvig of Exante Data Inc. offered a bottom-up estimate, extrapolated from chipmaker Nvidia Corp’s revenue, of $387 billion in capital spending just on AI data centers in 2025. That would be about 1.3% of GDP, up from 0.8% in 2024 and 0.3% in 2023. (Nordvig’s estimates of AI’s impact on GDP growth are larger than that because of estimated multiplier effects, and current consensus forecasts of Nvidia’s revenue for the rest of the year would put the AI-data-center GDP share closer to 1.5%, but I’ll stick with the original numbers for simplicity’s sake.)

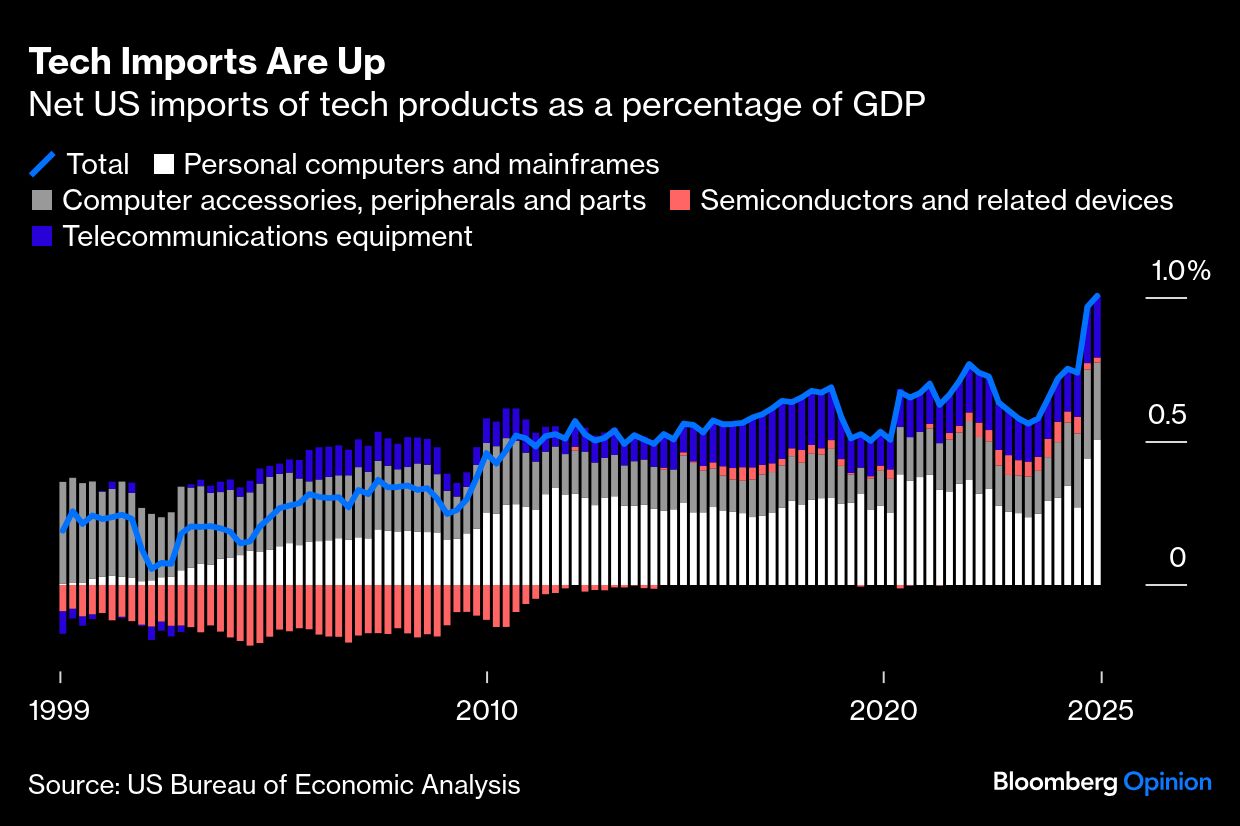

That 1%-of-GDP increase since 2023 is much bigger than the 0.4%-of-GDP increase in information technology investment shown in the above chart. It could be that AI spending is cannibalizing some other tech expenditures, but the main explanation for the disparity seems to be that the BEA’s domestic investment numbers exclude spending on imported technology — and net imports of information-technology products are almost half a percent of GDP higher than they were two years ago. In national income and product accounting, net imports are subtracted from GDP, so I can’t just combine the two charts, but the import numbers do bring the spending increase close to Nordvig’s estimates.

So is 1.3% of GDP going to AI investment a lot? In a post based partly on Nordvig’s work, veteran tech analyst Paul Kedrosky compared his own 1.2%-of-GDP estimate of current AI capex with 1% of GDP for telecom investment at the peak of that boom in 2020, and 6% of GDP for railroads in the late 1800s. “It’s not clear whether we’re at peak yet or not,” he wrote, “but ... we’re up there.”

Up there, perhaps, but not breaking any records yet. As is apparent from the first chart above, there was more to the 1990s tech-investment boom than just telecom (which falls mostly under “other information processing equipment” in the chart). Non-telcos were loading up on computers and software, and the increase in overall tech-related capital spending was much bigger than what we’ve experienced with AI — which could of course change if AI spending keeps growing.

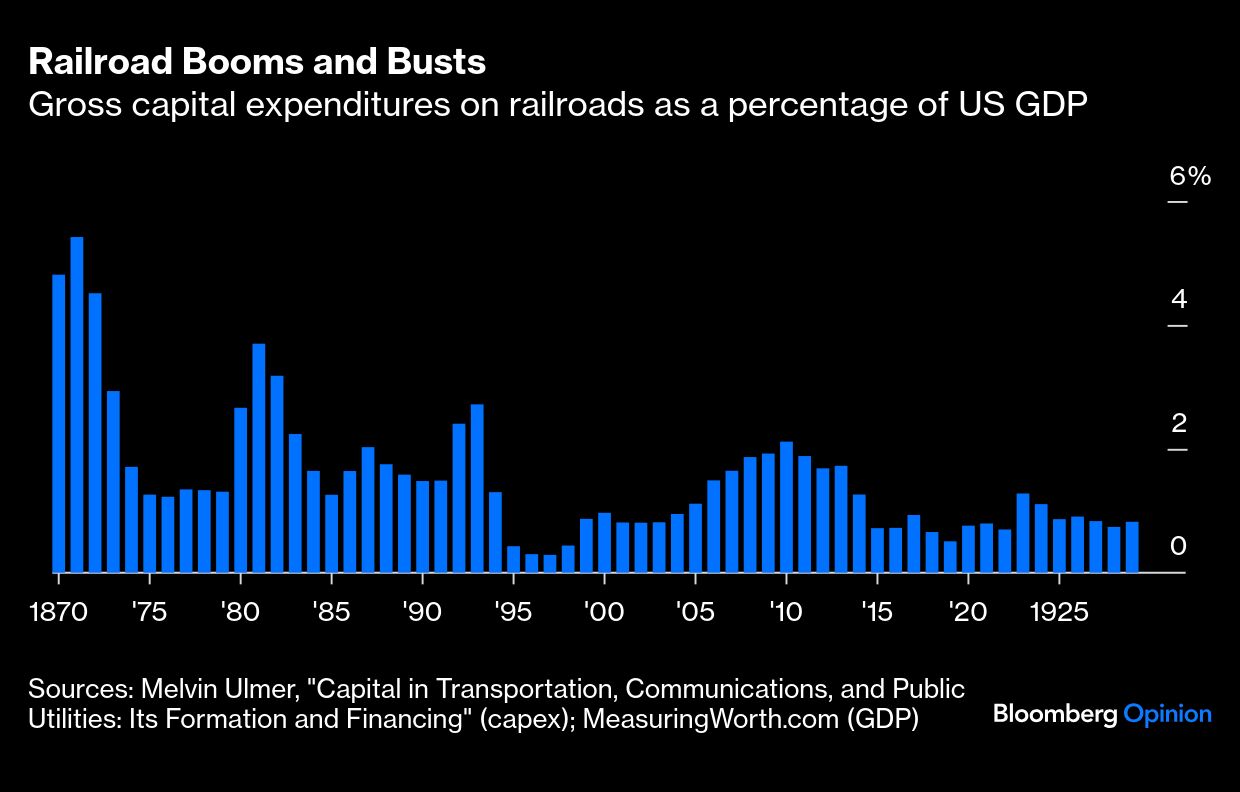

As for the late-19th-century railroad investment boom, AI investment still has a long way to go to match the economic impact of that episode in American history. I assembled this chart from economist Melville J. Ulmer’s 1960 book Capital in Transportation, Communications, and Public Utilities: Its Formation and Financing and the GDP estimates maintained by MeasuringWorth.

Railroad capex averaged 2.4% of GDP in the 1870s and 1880s but fluctuated wildly, approaching 6% near the beginning of the period and collapsing to 0.3% during the long depression that followed the financial crisis of 1893 — before beginning a long era of steadier but lower investment relative to GDP.

Overshooting and correction is in the nature of investment booms, which in the past tended to benefit society even if not always those who did the investing. We’re still using fiber-optic cable laid in the late 1990s and early 2000s, and relying on some railroad infrastructure from 1873. While one can see lots of potential economic benefits from investment in AI, it’s hard to imagine that vintage-2025 Nvidia AI chipsets will be of much use a century or even a decade from now.

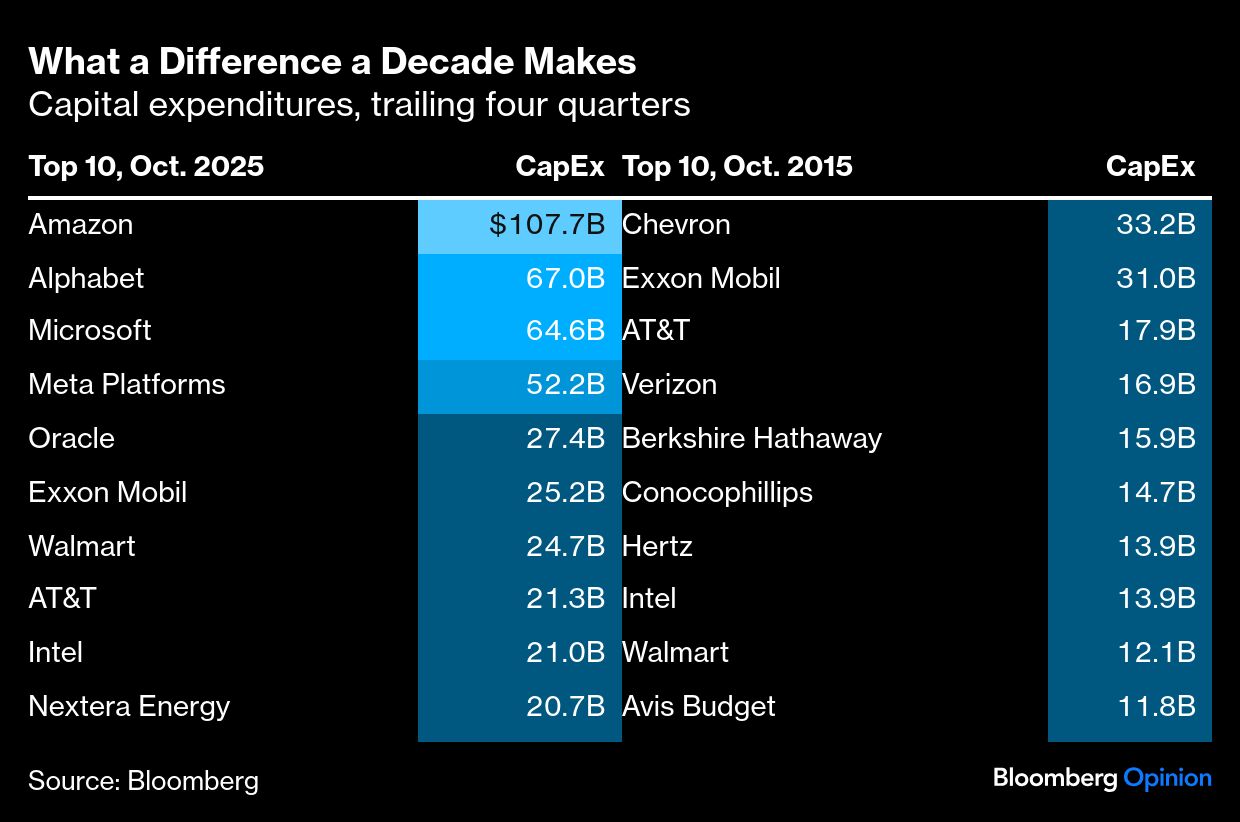

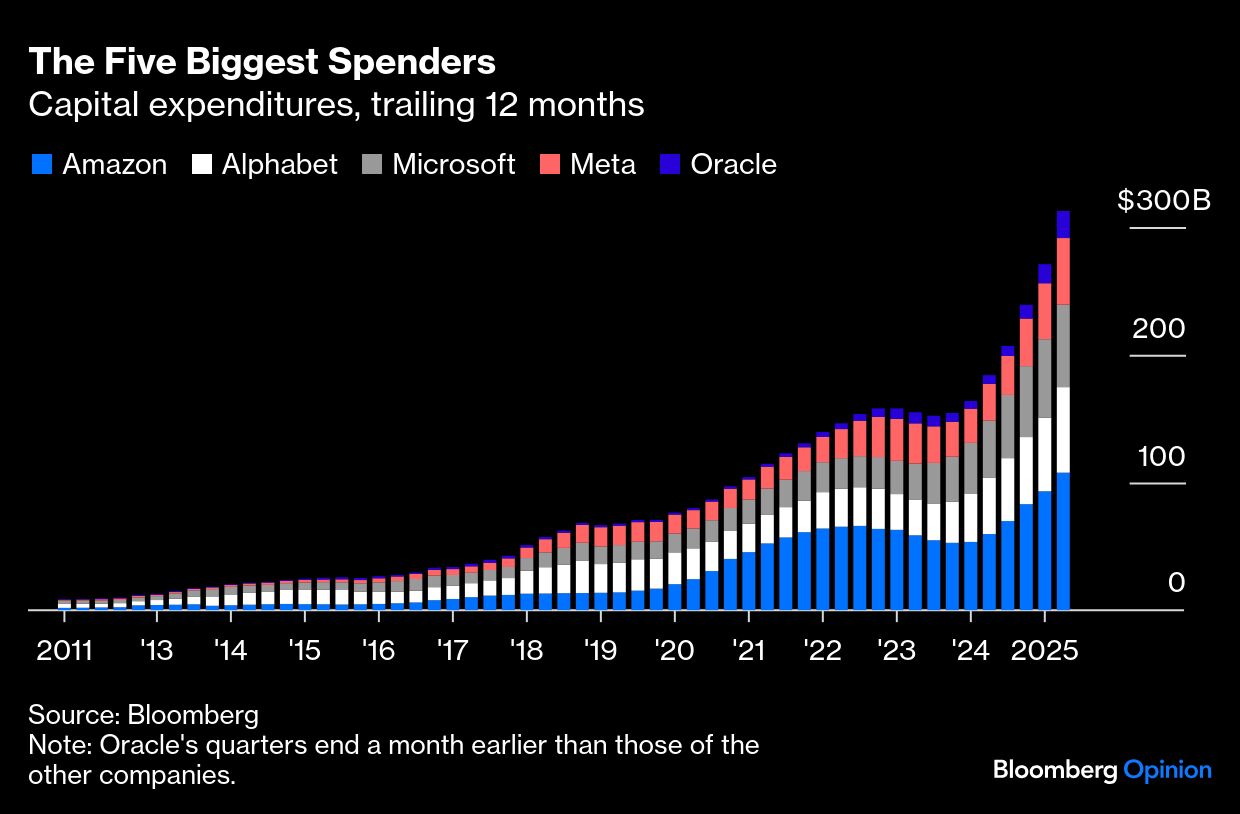

Companies plowing money into AI data centers are funneling it into rapidly depreciating assets, and given that it’s a handful of companies doing most of the plowing, one can’t help but wonder what they’re getting themselves into. Tech companies making huge investments in AI occupy the top five spots in US capital expenditure rankings. None of the five was in the top 10 a decade ago (Google parent Alphabet Inc. was No. 12).

As of the second quarter, capital expenditures at these five companies were running at an annual pace of $313 billion, which is about 1% of US GDP, although not all the spending is in the US. That’s more than double their spending in 2023.

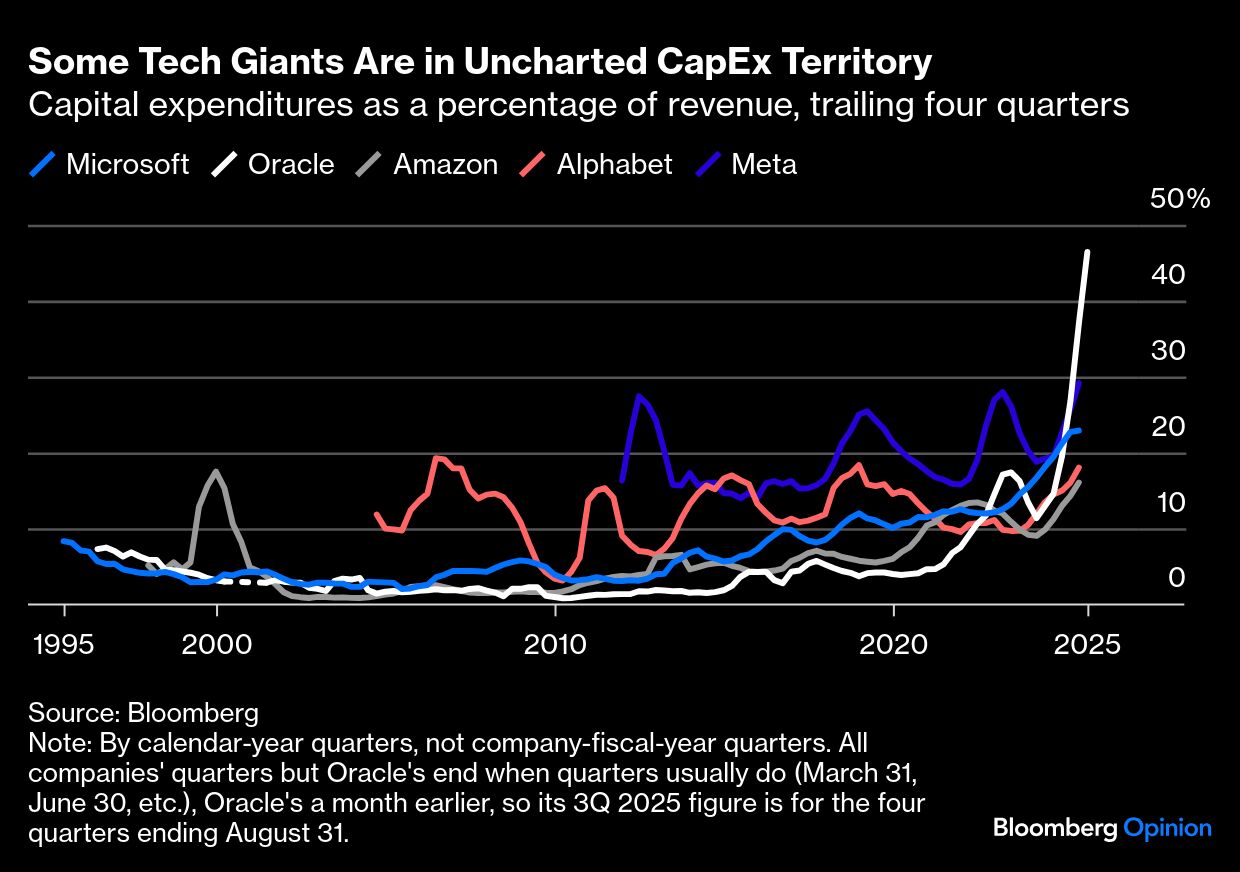

Another way of measuring this spending is as a percentage of revenue. For Google parent Alphabet and Facebook parent Meta Platforms Inc., current ratios are high but not out of line with their spending the past couple of decades. For Microsoft Corp., Oracle Corp. and Amazon.com Inc., where one can track spending back to the 1990s, the current investment boom really is something new. Amazon’s ratio of capital spending to revenue has yet to equal the peak of 17.5% near the end of the dot-com bubble in the fourth quarter of 1999, but it was a small, money-losing company then and is on track to to surpass that record soon anyway. Microsoft and Oracle, already big, profitable companies in the 1990s, were not spending at anywhere near current rates then.

In the 1990s Oracle and Microsoft sold software and Amazon sold books. Now they offer software as a service and hosting for other SaaS providers. That means they have big infrastructure commitments that they didn’t before, so it’s not crazy that their capital spending has risen. But Oracle’s 46.5% of revenue going to capital spending over the past four quarters is a higher share than even infamous telecom high-flyer (and subsequent steep faller) WorldCom Inc. ever hit in the 1990s.

It’s a huge bet — and huge bets don’t always pay off. The wild recent gyrations in Oracle’s stock price, which rose almost 50% in early September and has fallen 15% since, are an indication of the stakes.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Justin Fox