How might policymakers alter their 2% inflation targets without getting attacked by the bond vigilantes for playing fast and loose with their mandates? The post-pandemic experience of soaring consumer prices demands a review of how central banks conduct themselves; policymakers should bite the monetary bullet by asking their political masters to allow them to adopt individual inflation bands, and fend off potential critics by adding an obligation to embrace some broad growth measure that embraces the wider economy in guiding interest rates to an appropriate level.

As I've argued before, attempting to steer multitrillion-dollar economies to land with laser precision onto a micro-specific inflation pin is a fool’s errand. The aura of invincibility and omnipotence has cracked; central banks should be voluntarily seeking reforms, or they will be reformed in ways that may prove less than ideal. The current omerta surrounding the topic is unsustainable, especially when politicians are starting to question the independence of their central banks.

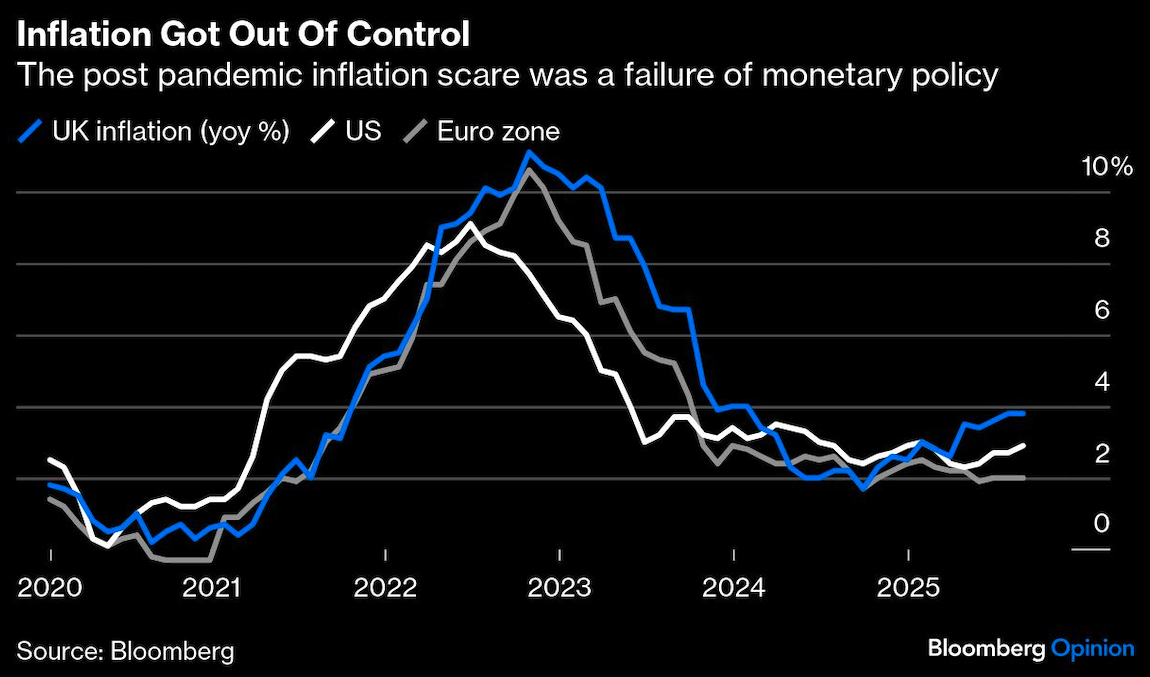

Too little attention was paid at the start of the decade to the likely hangover from a heady cocktail of cutting interest rates close to zero and increased bond buying via quantitative easing — at the same time as governments delivered a bucketload of fiscal stimulus. A deliberate avoidance of accountability combined with antediluvian communications and a spreadsheet-driven mentality endanger what central bankers revere most — their independence.

Key to any reevaluation of how monetary policy is conducted has to be an attitude change. Rigid academic adherence to backward-looking datasets has to be scrapped, especially as the quality of the numbers in far too many countries is being questioned. An overhaul that pays more attention to the multitude of agents and decision makers that policymakers already informally consult when setting borrowing cost would be helpful for a start.

Above all, enhanced flexibility ought to be the new mantra. The Federal Reserve's pre-pandemic Flexible Average Inflation Targeting was short lived because the market detected a lack of conviction — it was really designed to breathe more stimulus in after a bout of sluggish growth — and, credit where it’s due, the central bank ditched it quickly as consumer prices started to accelerate. Nonetheless the initial idea is valid.

Moreover, one size doesn't have to fit all. Clumping around a 2% inflation target may seem to offer safety in numbers, but what suits the Fed isn’t necessarily appropriate for the European Central Bank. Setting a target range rather than a single mark can work provided policymakers feel confident to sometimes make clear that one end of the range is what they're aiming at for a particular period.

Multiple mandates encompassing economic variables such as maximum employment or nominal growth all have merit. And steering interest rates across the yield curve, not just overnight rates, should at least be a topic for consideration. Not paying due attention to how steep the curve is and how that affects investment and crimps government budgets leads to policy errors; the importance of calibrating short-term interest rates with the longer-dated repercussions of shrinking or expanding central bank balance sheets in an age of quantitative tightening and easing can’t be underestimated.

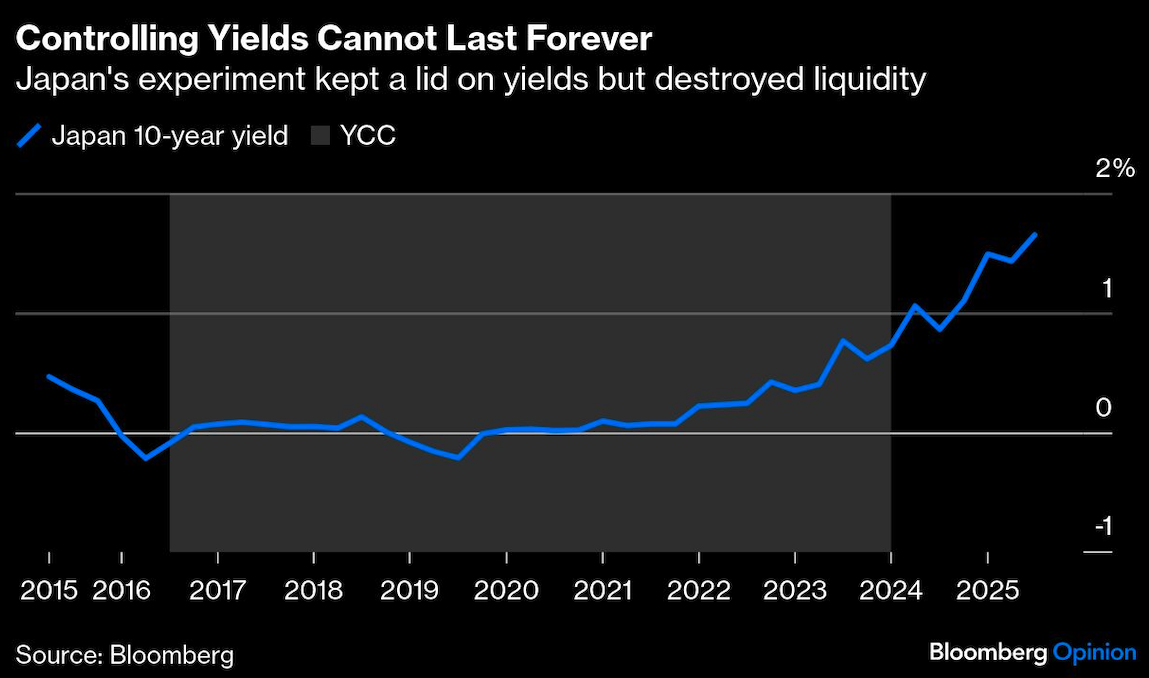

That, though, shouldn’t sanction explicit yield curve control, as trialed by the Bank of Japan between 2016 and 2024. Optically, there was a long period of stability — but at the heavy price of sharply reduced liquidity. Japanese government bond yields are now significantly higher; the experiment has driven buyers out of the market, perhaps for good.

Lorie Logan, president of the Federal Reserve Bank of Dallas, last week proposed replacing the central bank’s benchmark federal funds rate with a more widely used market bellwether. The federal funds market, where banks once lent to each other on an overnight basis, has ceded activity to the market for repurchase agreements, another form of short-term lending. So far, she's a lone voice willing to question the current ossification of monetary policy — and even then is only tinkering with its output mechanism, rather than the guiding inputs.

Shifting to a target range for inflation must make it explicit that consumer price increases can occasionally be allowed to linger below 2%, drifting closer to deflationary levels; otherwise, those bond vigilantes will always suspect policymakers will be more comfortable at the higher end of the spectrum. That 2% shibboleth may have been the answer once — but central bankers should be willing to move with the times and embrace change before change is inflicted on them.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Marcus Ashworth