Treasuries rose as traders latched onto fresh signs that the US labor market is softening, bolstering their outlook for how much the Federal Reserve might cut interest rates in the coming months.

The 10-year note’s yield fell below 4% for the first time since early April, while the five-year note’s came within a basis point of its lowest level this year after the weekly tally of new claims for unemployment insurance unexpectedly jumped to the highest level in almost four years. Yields ended the session between one and five basis points lower.

Demand for the monthly auction of 30-year bonds, though less robust than for this week’s two other Treasury debt sales, was strong enough to keep the gains mostly intact.

The latest sign of weakening labor conditions was viewed as likely to quell Fed policymakers’ concerns about inflation that still exceeds their target, leading them to cut interest rates for the first time this year when they meet next week. Briefly, traders fully priced in quarter-point cuts at each of this year’s three remaining meetings of its rate-setting committee. The market-implied odds of a larger, half-point cut next week remained minimal.

The jobless claims data overshadowed a report on August consumer prices that was mostly in line with economist estimates. The annual growth rate increased to 2.9%, approaching this year’s high. A different inflation gauge that the Fed aims to have average 2% over time was 2.6% in July, and August data won’t be published until the end of this month.

“The more concerning news from the data this morning is jump in claims,” Tiffany Wilding, economist at Pacific Investment Management Co., said on Bloomberg Television. “The data confirms the 25 basis points cut. There is probably going to be discussions around 50 basis points,” she said, referring to next week’s meeting.

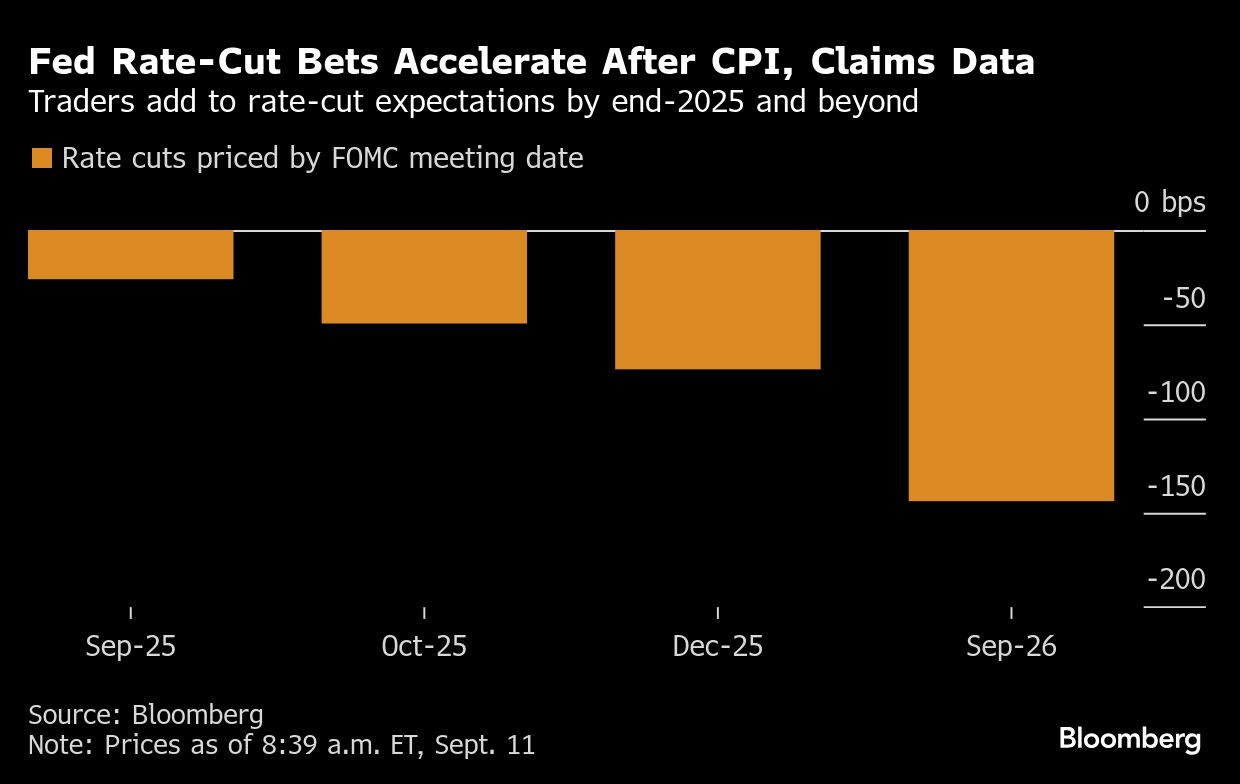

While the economic data had little impact on market-implied expectations for next week’s Fed decision, traders priced in a steeper downward path for the federal funds rate in subsequent months. The target band for the overnight lending rate has been 4.25% to 4.5% since December following three cuts totaling 100 basis points late last year.

Thursday’s rally trimmed interest rates for short-term interest rate futures contracts expiring during the first half of next year by about six basis points, fully pricing in four quarter-point cuts by the end of March.

Rate-cut expectations began to soar several days after the Fed’s most recent meeting in July, when employment data for July and revisions to the two previous months painted a more dire picture of hiring than policymakers had been aware of. Until that point, their assessment of risks facing job-seekers were more evenly balanced with predictions of faster inflation arising from tariffs the US administration has been implementing this year.

“The overarching conclusion of the market is that the Fed is going look at the jobs side of the equation,” said Robert Tipp, chief investment strategist and global head of bonds at PGIM Fixed Income. Even a cautious approach to easing “would still seem to be pretty much in line with, say, 100 basis points of cuts in the next year.”

Limiting the market reaction to the jobless claims data was the possibility of distortions caused by the US Labor Day holiday and stability in the total number of claims, said Guneet Dhingra, head of US rates strategy at BNP Paribas.

Still, “anything that these days shows any signs of weakness in the labor market seems to put investors on high alert that it could put the Fed on track for larger easing,” Dhingra said.

The initial drop in yields after the US data also stalled amid weakness in euro-zone government bonds after hawkish signs from the European Central Bank, which met Thursday.

The auction of 30-year Treasury bonds at 1 p.m. New York time drew 4.651%, in line with its yield in pre-auction trading shortly before the bidding deadline, a sign that demand was as expected. Sales of three- and 10-year notes over the past two days drew lower-than-indicated yields, a sign of strong demand despite offering the lowest yields this year. The 30-year auction result was the lowest since March.

Those auctions also produced record-low awards to primary dealers, a sign of strong bidding by investors. For the 30-year, the 10% primary dealer award was lower than last month’s, but short of a record low.

Other risks that attend next week’s Fed meeting include quarterly revisions to policymakers’ economic projections and expectations for the path of rates. In June, the median forecast was for two quarter-point rate cuts in 2025, followed by declines over the next two years.

Bond investors are also interested in whether a decision to cut rates next week is unanimous. In July, two Fed governors — Christopher Waller and Michelle Bowman — dissented the decision to keep rates unchanged in favor of lowering them, and Waller has since has since said he favors “multiple cuts” in the coming months. Assuming a quarter-point cut next week, dissents could be in favor of the September meeting a bigger move or none at all.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Liz Capo McCormick, Ye Xie