Unlike Donald Trump, Chinese President Xi Jinping is not known for caring about stock-market returns. As recently as 2021, the government went ahead with harsh regulatory crackdowns on big tech and real estate developers, ignoring global investors’ bitter complaints.

But there are clear signs that Xi is changing his mind. State-owned institutional investors are pouring billions of dollars in this year. In January, the government said large insurers will need to invest 30% of their new policy premiums in onshore equities. In April, Central Huijin Investment Ltd., a domestic unit of the sovereign fund China Investment Corp., formally established its presence in the market. As of the end of June, Huijin owned 1.3 trillion yuan ($180 billion) of index funds.

So it’s worth asking what prompted the change of heart. Investors are expecting a Xi put — a belief that the state will purchase Chinese stocks in the event of a rout. Will the institutional support be here for the long-run?

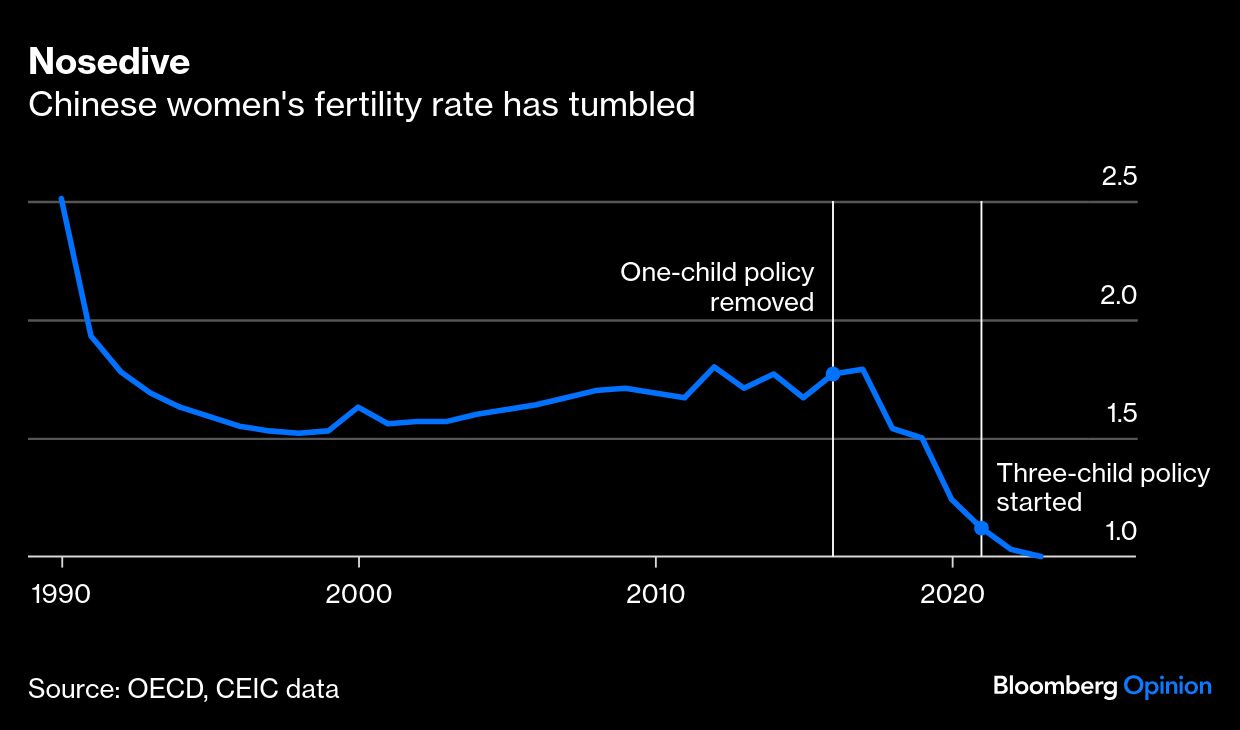

Sharp demographic shifts may be forcing Xi’s hand. It took just five years for China to enter a fertility crisis. Only 9.5 million babies were born in 2024, an alarming decline from about 15 million annually before the pandemic. The total fertility rate, or the estimated average number of children a woman will have in her lifetime, tumbled to just 1 in 2023 from 1.8 in 2019.

As a result, the social safety net is becoming impossible to maintain. In 1990, for every new retiree, China had about 3.6 workers entering the labor force. By 2045, that number will fall to 0.4 — there will be only 9 million job entrants starting to contribute to social security, but 21 million who begin to receive pension benefits, according to estimates from Goldman Sachs Group Inc. The tables have turned.

This perhaps explains a slew of new policies to improve the math. China raised the retirement age late last year for the first time since 1978. A recent court ruling closed the loophole small businesses have been using to opt out of mandatory social insurance payments. And new child subsidies — 3,600 yuan a year per child under the age three — will be handed out to boost birthrates.

But these measures alone are not enough to unburden a stressed pension system. China’s social security has achieved near universal coverage, with more than 1 billion people included. That accomplishment also comes at a great cost, however. The government has been subsidizing state pensions for at least a decade. In 2023, the total reached 1.7 trillion yuan, or 6.4% of fiscal expenditure.

Even with state subsidies, millions of baby boomers don’t have enough to enjoy their golden years. Urban salaried workers are covered under the employee insurance, a defined-benefit plan that pays out a percentage of pre-retirement income. It distributed an average 45,000 yuan per person in 2023. But many others, including those in rural areas or who don’t have full-time jobs, are only enrolled in the so-called resident insurance, which disbursed a dismal 2,671 yuan that year.

This is why the stock market will be increasingly important as Chinese society ages. The US offers an enviable example. Those born between 1946 and 1964, the first generation to be offered 401(k) pension plans when they started work, have more money than anyone else, because of the soaring value of stock portfolios and homes. Many don’t rely on the social security check, which averages $2,000 a month, for a living — and won’t complain if annual retirement payment increases are small.

China is certainly keen to replicate that recipe, especially now that the housing market is in a prolonged downturn. Late last year, the government rolled out its version of an Individual Retirement Account, or IRA, nationwide, which allows people to invest up to 12,000 yuan a year tax-free. But will they bother to enroll if the stock market is perpetually in bear territory? Similarly, the state pension system might become more self-reliant if social security funds can notch better capital gains.

The so-called TACO trade, betting that Trump will eventually chicken out of market-unfriendly policies, is popular this year. This is because the US president has long seen the S&P 500’s performance as a proxy for his approval rating. Xi, serving an unprecedented third term, doesn’t have to worry about that. However, he does have a fiscal book to balance, perhaps for decades to come.

In the future, when one worker has to support three pensioners, equity returns will be very important. Xi has no choice but to love the stock market.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Shuli Ren