The market’s attention usually seesaws between corporate fundamentals and monetary policy. After earnings season effectively ended with an underwhelming report from Nvidia Corp., the Federal Reserve’s next rate decision — along with any signals about the future path of interest rates — is poised to dominate this month. The market’s lofty expectations for policy easing set the stage for what could be a volatile September.

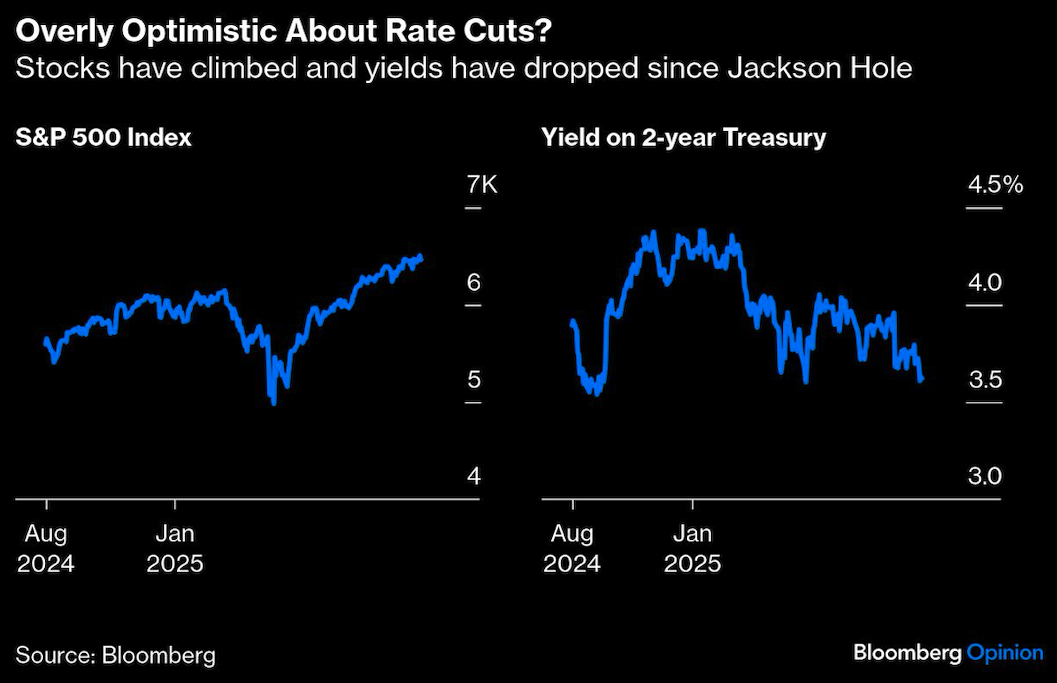

Even with a jump on Tuesday, yields on two-year Treasury notes are down 0.11 percentage point since Fed Chair Jerome Powell spoke at the Jackson Hole central banking symposium on Aug. 22, leaving them about 0.13 percentage point above an almost three-year low. Stocks are near all-time highs, with forward price-earnings multiples close to their richest of the current millennium.

But in reality, markets may have mistaken a nuanced speech about two-sided risks to both the labor market and inflation for a rock-solid signal of imminent rate cuts. While Powell’s speech alluded to possible easing, it left plenty of room for policymakers to put off action depending on the evolution of the data. In the next two weeks, policymakers will get two crucial new pieces of information that could turn the debate on its head: Friday’s payrolls statistics and the Sept. 11 publication of the August consumer price index. The upshot is that the odds of a September rate cut may not be quite as high as the 89% likelihood currently implied by futures trading. And if policymakers end up dashing expectations, the reckoning could be particularly unpleasant.

The most consequential Fed meeting of the year comes during a major dearth of corporate headlines to compete for traders’ attention. If you wanted to feel optimistic in recent years, corporate America (and its pals on Wall Street) have provided the very best medicine during earnings season. Companies have crushed expectations, and Wall Street analysts have generally used the new information to raise their price targets, a virtuous cycle for equities. In fact, over the past five years, the first and second months of reporting season have seen price targets revised up on average by 1.6% and 1.5%, respectively. In the dead month, with virtually no large-cap earnings, price targets rose just 0.4%.

So if companies aren’t reporting and analysts aren’t upgrading, stock traders have little to look forward to aside from the debate over monetary policy — well, that and the volatile policy declarations coming out of the White House. In that regard, deregulation and tax cuts appear to be priced in at this stage, and there are still persistent risks from unpredictable trade policy and attacks on central bank independence.

Our best chance of a “good news” in September might be signs of a swift resolution to the tariff debacle. The US Court of Appeals for the Federal Circuit ruled on Friday that Trump inappropriately used an emergency law to implement tariffs. But the judges left the tariffs in place as the case winds its way through the court system, and markets were in no mood to celebrate the the decision on Tuesday, the first trading day after the decision. The reaction pointed to the highly uncertain final outcome if the case goes to the Supreme Court. Meanwhile, the uncertainty seemed unlikely to do monetary policy doves any favors in the near-term.

If the Fed cuts meaningfully in September and subsequent months, it would be because the economy is cooling, perhaps due to the lagged effects of the aggressive tariff policy rolled out this year. That’s not the most constructive setup for equities, at least over the next month or so, until earnings season comes around again and gives us something else to think about.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin