Despite Tuesday’s wobble, the narrative that has been fueling the sharp recovery in US equities since April remains supportive as the drivers of the rally are still intact.

The pullback on the Nasdaq was largely due to profit taking on Nvidia Corp. and Palantir Technologies Inc., two of the hottest stocks this year. Investors rotated into defensive names to diversify beyond the most crowded trades, while staying invested in a fundamentally solid market.

Equities have managed to shake off moments of weakness due to the strength in the core drivers of this year’s rally: strong profits from big tech and large caps in general, as well as the integration of artificial intelligence.

Even as the S&P 500 retreated further from the record high it set last week, more than 350 index members traded higher on Tuesday. Themes like shares in companies with pricing power, the stagflation trade and low volatility stocks bucked the downward force and gained on Tuesday.

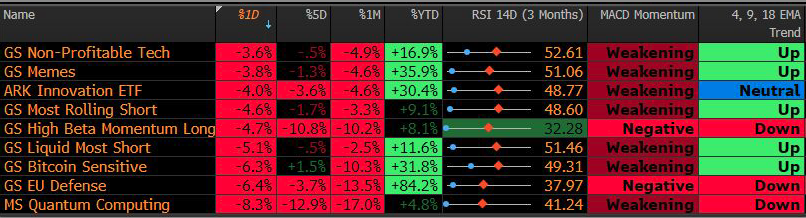

On the other hand, favorite trades were sold, with significant declines in thematics like meme stocks, most-shorted stocks, Bitcoin-sensitive names and the European defense trade.

Some parts of the market are overbought, the Nasdaq 100’s breadth remains unusually narrow and the S&P 500 bullish streak above its 50-day moving average is also an outlier. But putting the technical issues aside, the backdrop remains supportive for now.

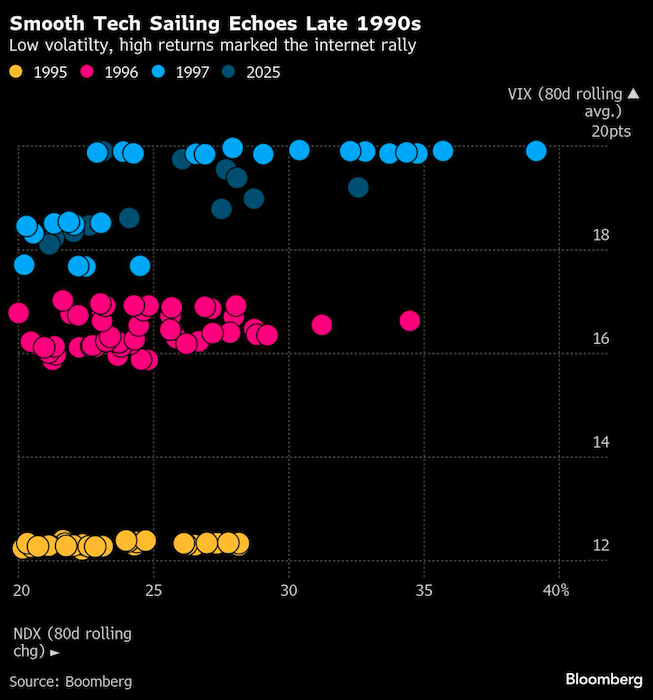

The current market set up is prompting veteran market commentators to reach for the history books.

“In a few different ways, this reminds me of those riveting summers from the very end of the 1990s,” Goldman Sachs Group Inc. partner Tony Pasquariello wrote in a note to clients. There are parallels with the period referenced by Pasquariello: markets are heading for a trifecta of all-time highs, super low volatility and a Federal Reserve that’s most likely about to cut interest rates to prevent recent cracks detected in the macro economic picture from expanding into a recession.

And while trading volumes for stocks are likely to dwindle to their seasonal low over the next two to three weeks, making the market a touch more vulnerable to sudden shifts in positioning, there is little to suggest that the majority of investor flows will be exiting stocks.

Read more: Underweighting AI Stocks Cost Mutual Funds, Goldman Says

Institutional positioning, even in some of the hottest trades, does not seem to be overly extended. Trading in equity futures is far short of its peak, suggesting that many portfolios haven’t built major short-term exposure.

Flows among momentum-driven commodity trading advisers, or CTAs, are heavily skewed to the downside, although their positioning does allow for some further buying. More importantly, CTAs need the trigger of a consistent decline before their selling power can play out.

Corporate buybacks are helpful to the market too, with more than 90% of companies emerging from blackout periods that prevented repurchases, as the earnings season wraps up.

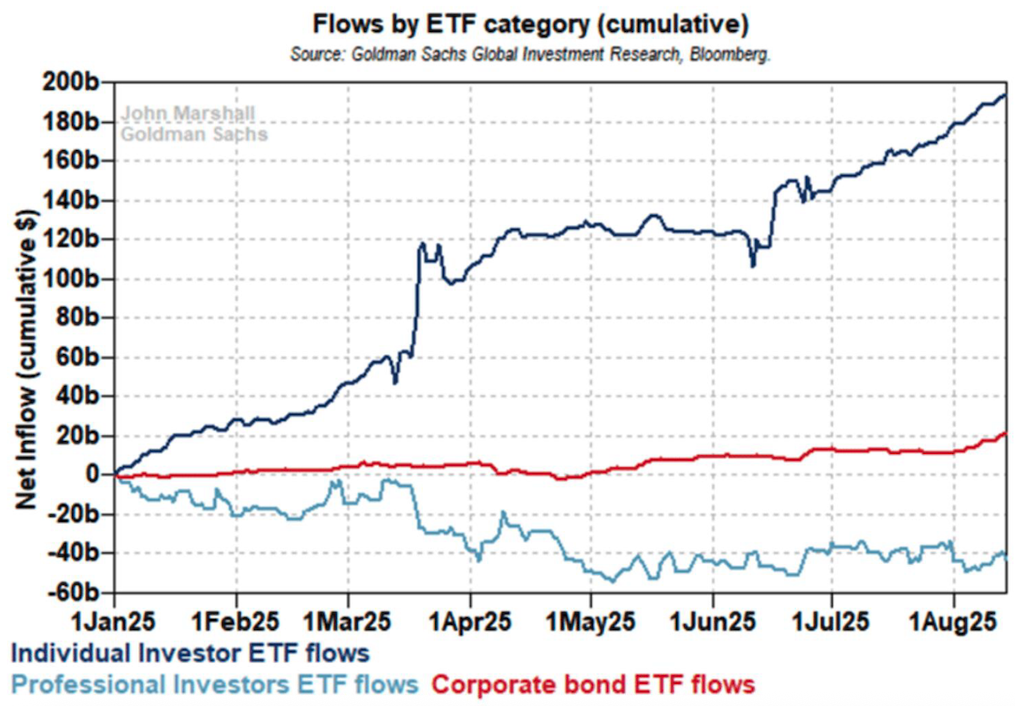

Retail flows are steady for now, providing broad support. Options flows from dealers, meanwhile, are unlikely to be a drag on the S&P 500. They are at a cyclical low this week following the latest expiry, with dealer gamma exposure in a trough in the space between the roll-off and before September contract deltas become more reactive.

“This reduces the influence of options market flow and allows SPX to move more on organic supply and demand rather than positioning-related mechanics,” note the option flow specialists at Tier 1 Alpha. “While not always the case, the week after expiration often marks the beginning of new market trends. With dealer positioning at its lightest, volatility tends to be slightly higher and less predictable based on the market structure alone.”

Equity benchmarks have also shown evidence of a broadening out in gains over the past week. Some year-to-date underperformers are doing well, most notably US small-cap stocks.

There has been evidence of this further afield too. The Shanghai Composite Index climbed to the highest in 10 years, overcoming tariff and domestic China issues. What’s more, these gains have been accompanied by significant trading activity, suggesting another risk-on market that’s being carried higher by broader investor flows.

Prepare your bond portfolio for changing market conditions. Register today for the Fixed Income Symposium on Sept. 18, 2025, 11AM ET / 8AM PT.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.