Rising Rates Are Good for You: Part 2

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In Part 1 of this two-part series, we deconstructed the (semi-)myth that rising interest rates are bad for bond investors by exposing in detail the prevalent submyth that 40 years of falling interest rates were a “tailwind” from the early 1980s through the early 2020s.

In summary, while that was indeed a 40-year backdrop of strong fixed income returns, the credit (no pun intended) goes to the very high interest rates with which the period began, not to the unremitting decline in rates thereafter. Contrary to the tailwind mythos, had interest rates stayed at their 1981 levels, or even risen further — ignoring the potential rising risk of default! —bond portfolio returns would have been even better.

However, we did notice that the tailwind hypothesis contains a grain of truth on shorter time frames.

A portfolio of longish-term bonds held to a shortish-term horizon did appear to benefit from a drop and suffer harm from a jump in interest rates. This article’s purpose is to sharpen that observation and remove the ambiguity — and to examine as a corollary how bond investors can truly reduce interest rate risk with respect to their individual goals.

A simpler toy

To accomplish this purpose, we will investigate a toy model more rudimentary than the last article’s already-simplified system of separating the immediate and subsequent consequences of annual rate changes. To better isolate the immediate price change and the subsequent yield differential caused by an increase or decrease in interest rates, let’s examine what happens when a rate move happens immediately and then holds at the new level for a sustained period.

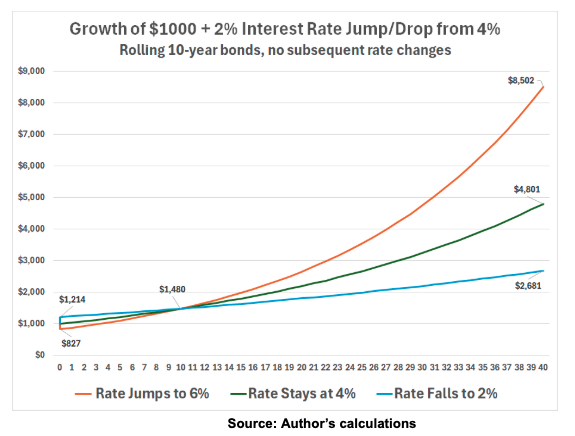

We’ll pursue the same strategy of rolling 10-year zero coupon bonds for 40 years. This time, let’s assume the 10-year rate is 4% initially.1 Then, through some sort of quantum superposition,2 we experience three simultaneous futures:

- Interest rates immediately jump to 6%, and they stay at 6% for 40 years.

- Interest rates hold at 4% for 40 years.

- Interest rates immediately fall to 2%, and they stay at 2% for 40 years.

Here are the results:

If rates fall by half, we experience an immediate 21% gain and feel rich. If rates rise by half, we experience an immediate 17% loss and feel we should have waited a few more seconds to buy, but alas.

As time goes on, however, the gap narrows and then reverses, and ultimately we experience the same results as before: Long before the 40 years elapse, the initial pain from a rate jump has been wildly overcome by the ongoing bonus of higher interest accruals, while the initial joy of a bond price increase has been obliterated by decades of lower yields. How long before? In exactly 10 years, the three series converge to the same 48% total return, with results favoring the higher-rate series thereafter.

The 10-year convergence of a model using 10-year bonds is clearly no coincidence. If a 10-year zero coupon bond with a 4% annual percentage yield has a $1,000 price tag today, then it must have a face value (the value returned to the investor at maturity in 10 years) of $1,480.

When rates jump/drop to 6%/2%, that means the market price today has adjusted to a level such that 6%/2% annual accruals will result in the same $1,480 value in 10 years. With five-year zero coupon bonds, the crossover would occur in five years; with 30-year bonds, it would take 30 years; with one-year bonds, higher rates would start winning after just one year; with short-term “cash” instruments, higher interest rates start winning immediately.

Price risk vs. reinvestment risk

The above example illustrates two countervailing interest-rate-driven risks in fixed income investing: price risk and reinvestment risk. Price risk is the possibility that your bonds will lose value immediately if interest rates rise. Reinvestment risk is the possibility that your bond portfolio will earn less money than initially expected if interest rates fall before you roll your bonds to longer-dated maturities.

Observations of price risk, with its greater immediacy, are what give rise to the notion that rising rates are “bad” for bondholders, but as illustrated above, this notion can be enormously wrong if an investor’s horizon is longer-dated than their bond holdings.

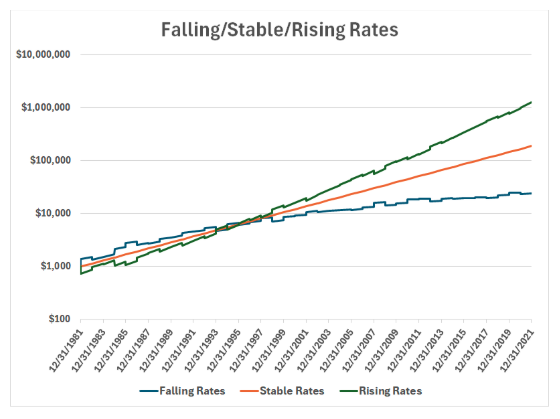

In the prior article, the crossover occurred after significantly more than 10 years. This is because that model rolled annually into a new 10-year bond, thus pushing out the maturity of the bond portfolio every year, even as interest rates (usually) continued to fall. Nonetheless, the tortoise of higher interest rate accruals inevitably beats out the hare of immediate price drops eventually.

Note that I didn’t specify whether this article’s simpler toy model involves rolling out to new 10-year bonds annually, at maturity, or on some other frequency. In the special — and nonsensical — case where interests rates change only once at the beginning, reinvestment risk is the same no matter when or how often you reinvest. In the real world, with ever-changing interest rates, how often you roll into new bonds does matter … but eventually the cumulative effect of reinvestment risk will overwhelm price risk, if interest rates evolve primarily in a single direction.

Portfolio immunization methods

We are ready to revisit the opening paragraph of the Part 1 article, specifically this sentence: “If, as is true of most individual investors, your fixed income portfolio has a shorter duration than does the future spending (of all kinds, even legacy) towards which you are investing, then as a bond investor you are better off with rising than with falling or stable interest rates, short-term losses from rising rates notwithstanding.”

The key word there is “duration”: This is a measure of the number of years required to recover the upfront cost to purchase a bond or bond portfolio, and it is very similar to the weighted-average timing of a bond portfolio’s promised cash flows. In the above example, the duration of a 10-year, zero coupon bond is 10 years.3

Consequently, if investors intend to liquidate the bond portfolio and spend the money in less than 10 years, then they are better off if rates drop; but if they plan to hold the bonds for more than 10 years, a rate increase is better for them, ignoring the aforementioned complexities from rolling the bonds forward early.

Which scenario is more common? Do bond investors tend to have longer-duration liabilities (the set of intended future uses for the money) or longer duration fixed income assets? Let’s consider:

- If you’re 50 years old, if your portfolio is for an age 65 retirement hopefully lasting ~30 years (i.e., an income liability duration in the 20+ year range), and if you’re holding something like the Bloomberg US Aggregate Bond Index (duration ~6 years), then you are far better off if rates rise than if they fall. (As a bond investor, anyway; as mentioned in Part 1, we offer no conclusions here about stocks’ response to interest rate changes.)

- If you panic whenever markets hiccup and go to cash with your retirement nest egg, then you are buying something that offers the warm fuzzies of low price volatility in exchange for taking on enormous reinvestment risk with no risk premium. At least the stocks that so frightened you offered a sizable expected return premium in exchange for their riskiness. Here’s hoping interest rates increase for you!

- But if you’re holding that aggregate bond index — or ETF — thereupon, and you’re on your deathbed, then … guess what? You’re not going to spend your portfolio. Your heirs are, and their spending needs are probably longer-duration than your ETF as well.

As these examples illustrate, the great majority of bond investors are “short duration,” meaning the purchases they will ultimately make with their investments have a much higher-duration profile than do their bond investments. Contrary to the popular fixation with price risk over reinvestment risk, such investors — most investors — are manifestly better off if rates increase.

A reader could be forgiven for wondering, “If it works both ways, why do these articles’ titles say rising rates are good for me? What if I don’t want either risk? I bought bonds to lower my risk.”

Look again at that $1,480 convergence point in the toy model chart. If you had a $1,480 spending need coming up in 10 years, then once you bought that bond, you could ignore the vicissitudes of price and reinvestment risk, because at the 10-year mark, they will precisely offset one another. More generally, duration matching — setting the duration of a bond portfolio equal to the duration of the spending needs for which the portfolio is invested — will “immunize” the portfolio against rate risk. Conversely, the greater the duration mismatch, the greater the interest rate risk. This is true of a mismatch in either direction, but in practice, excess reinvestment risk due to a bond portfolio that is much shorter-term than the investment horizon is far more common than excess price risk from holding overly long-duration bonds.

Rate risk from duration mismatch may rationally be deemed acceptable if, to pick a few examples: a) credit premiums or other considerations create compensated risk in sufficient expected quantity to justify the uncompensated rate risk; or b) the investor is willing to countenance adapting their cash flows in response to portfolio returns — essentially reverse immunization — for example, through dynamic portfolio withdrawal rules.

But for inflexible planned expenditures, immunization is possible by purchasing bonds with either defined, matched maturities (e.g., bond ladders, including TIPS ladders for inflation-protected goals) or matched duration, something I’ve written about previously.

Annuities offer another neat trick: They allow you to immunize a lifetime annual income need, despite not knowing in advance how long your life will be. Given longevity uncertainty, it’s impossible to duration-match a bond portfolio to a lifetime. Conservatively crafting a bond ladder that goes beyond life expectancy (e.g., the age-95 “target death” above) is an option, but: a) you may live even longer; and b) if you don’t live to the ladder’s end, then you overspent to build your ladder. Via “mortality pooling,” an annuity provider can efficiently craft income for life for a whole cohort of retirees (though I still want that inflation-protected income option.4)

Barring those options, though, the next time interest rates jump and your bond portfolio loses value, don’t panic … celebrate!

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Endnotes

1 As in the last article, I am using annually compounded rates for simplicity.

2Don’t most simple toys involve quantum superposition?

3 There are multiple definitions of duration, and this statement is true of Macaulay duration specifically, but that is also the form of duration that allows an investor to immunize rate risk.

4Retirement researcher Wade Pfau gave an excellent description of various dynamic portfolio withdrawal rules, and modeled some of the possible outcomes from using those rules, in the following two 2023 Advisor Perspectives articles:

https://www.advisorperspectives.com/articles/2023/03/06/a-comparison-of-variable-spending-strategies

In his roles as chief investment officer for Round Table Investment Strategies and portfolio manager for Torren Management, Nathan Dutzmann is responsible for applying financial science and investment research to the process of constructing portfolios tailored to the individual needs and goals of clients nationwide. Nathan was previously an investment strategist with Dimensional Fund Advisors and a partner and chief investment officer with Aspen Partners. He is also a member of the investment industry advisory council for The American College of Financial Services. He holds an MBA from Harvard Business School and a master’s degree in international political economy and a bachelor’s degree in mathematical and computer sciences from the Colorado School of Mines.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All