Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

US Exceptionalism

Over the past 125 years, the US has been an exceptional place to do business, combining solid productivity growth and population growth1 with world-leading innovation and powerful geopolitical advantages. The US emerged from both world wars physically unscathed2 and economically strengthened, allowing it to lead the global economy while much of the world rebuilt. Its development of the atom bomb and projection of both hard and soft power cemented its influence on the world stage.

Domestically, the US has fostered a uniquely business-friendly legal and regulatory environment, encouraging entrepreneurship, protecting property rights, and supporting deep capital markets. The U.S. possesses tremendous natural resources, and intellectual ones too, with roughly half of all Nobel prizes awarded to researchers living in the U.S. This combination of economic dynamism, technological leadership, and institutional strength forms the fundamental backdrop to the prevailing belief in US exceptionalism.

U.S. Stock Market Exceptionalism

The U.S. stock market has delivered tremendous returns to investors: an average annual return of 8.5% above inflation over the past 125 years, the highest among all major global stock markets. It is not surprising that nine out of ten of the world’s largest companies by market capitalization are U.S. companies.

US Stock Market Earnings Un-exceptionalism?

Given the facts laid out above, to what extent was the exceptional U.S. stock market performance due to U.S. companies riding the strong wave of 3.2% per annum U.S. real GDP growth to generate exceptional earnings growth? By “riding the wave,” we mean obtaining corporate earnings growth in line with GDP without requiring any reinvestment.

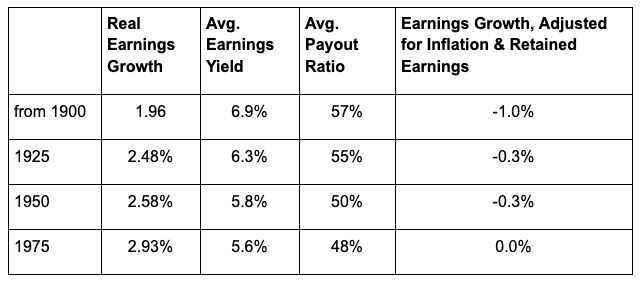

According to data provided by Professor Robert Shiller, real U.S. earnings growth over the past 125 years was 2.0% per annum. That may seem to support the notion that U.S. companies enjoyed some pleasant surfing yet didn’t catch the full wave of the 3.2% GDP growth. But, in fact, it’s telling us there wasn’t any good surfing at all.

We need to consider that U.S. companies, on average, retained 43% of their earnings to invest in plants and equipment or to buy back their stock, both of which are expected to generate earnings growth. Indeed, using either the stock market earnings yield or actual stock market real returns, the 43% of earnings that companies didn’t pay out as dividends should have generated about 3% real earnings growth just by itself, in addition to any GDP surfing. So, had companies caught the full wave of U.S. exceptionalism, they should have seen earnings growth of over 6% — a pretty far cry from the actual 2% they delivered. It looks more like they never made it off the beach!

Another way of seeing the decidedly unexceptional earnings performance is to look at actual market returns compared to expected returns. If companies had paid out all their earnings as dividends, and if they weren’t getting any earnings boost from the exceptional U.S. environment, then we’d expect their earnings to grow in line with inflation, and no more than that.

If you invested in the U.S. stock market in 1900, and you believed that corporate earnings would grow with inflation, then you’d have expected to earn a long-term real return equal to the earnings yield of the U.S. stock market in 1900, which was about 8%. And that’s pretty much what you got — 8.5% to be precise. That extra 0.5% is explained by the nearly doubling of the price-earnings market multiple from 1900 to today.

The conclusion — admittedly from just this one data point — is that while the US has indeed enjoyed a tremendously exceptional economic environment over the past 125 years, this has not translated into earnings growth that US companies could freely tap into. In the table below, we show that the story looks pretty much the same over the past 100, 75 and 50 years, too.

Non-US Corporate Earnings Growth

Unfortunately, we don’t have good data for non-US markets going back more than 50 years, but the picture for non-U.S. real, payout-adjusted earnings growth over the past 50 years is less than 1% worse than that of the U.S. If you incorporated that experience into your view of prospective real returns, you’d want to reduce your estimate based on the earnings yield of non-U.S. stocks by about 1%, a relatively minor adjustment.

Connecting the Dots

The U.S. has been extraordinarily exceptional in so many important dimensions, but corporate earnings growth has not been one of them. The past 125 years of U.S. stock market and corporate earnings experience is supportive of the idea that if companies pay out all their earnings as dividends, they’d be able to keep earnings growing with inflation, but no more than that, even with great economic tailwinds. If this holds in the future too, it implies that the market’s earnings yield serves as a simple and useful estimate of the long-term real return of the stock market.3

U.S. stock returns from 1900-2025 have been truly exceptional but are almost entirely explained by their high starting earnings yield in 1900. By contrast, today’s U.S. stock market earnings yield of 3.5% predicts low long-term real returns, and low relative returns compared to safer assets.4

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Endnotes

1Roughly 2% productivity growth + 1.2% population growth => 3.2% real GDP growth.

2With the exception of the bombing of Pearl Harbor.

3For more information, see our note on P-CAPE and the most important number in investing.

4For more, see our latest Capital Market Assumptions.

This is not an offer or solicitation to invest, nor are we tax experts and nothing herein should be construed as tax advice. Past returns are not indicative of future performance.

Victor Haghani is founder & CIO of Elm Wealth, a Philadelphia-based asset manager. James White is Elm Wealth’s CEO.

Learn more at www.elmwealth.com.

Read more articles by Victor Haghani, James White

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.