Why Ken Rogoff is Bearish on Inflation & the Dollar

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe views presented here do not necessarily represent those of Advisor Perspectives.

“Nothing about currencies is simple.”

–Mark Kritzman, winner of the 2025 James L. Vertin Award

Why is the U.S. dollar, which has lost more than 97% of its value since 1913, the dominant currency in the world? Is that status endangered, and what happens if the dollar loses its global reserve currency status? How bad is it for the U.S. government to have so much debt? Should we worry about inflation? How should we act if substantial further inflation is a threat?

Source

Kenneth Rogoff, perhaps the ultimate insider in the currency game, capably answers questions like these — and many more — in his memoir, “Our Dollar, Your Problem.” (The title refers to an insult lobbed by then-Treasury Secretary John Connally at a group of European central bankers in the 1960s.)

As a Harvard professor and chief economist of the International Monetary Fund, Rogoff was party to most of the important discussions and decisions regarding the global financial system during a period when that system was in flux due to the emergence of the euro, the collapse of Russia, the 2008 crash, the COVID crisis, and many other events. A better source of inside knowledge about currencies and global economic governance could scarcely be imagined.

Yet the book has flaws. Perhaps the biggest is that there’s little discussion of economic theory, a better treatment of which would benefit investors confused by the contradictions between monetarism, Keynesianism, the Fiscal Theory of the Price Level, and other concepts. Rogoff is a political centrist who is well-positioned to treat these topics fairly. Readers would have benefited had he included more economics in the book.

This time is different?

Rogoff is best known to investors as the co-author, with Carmen Reinhart, of “This Time Is Different,” his 2012 volume relating the level of government debt in a country to its potential for economic growth. (It’s bad news for countries with a debt-to-GDP ratio above 90%, he wrote at the time; he later softened his position a bit.) “This Time Is

Different” was criticized for relying on a paper that contained a math error, although that critique does not alter its conclusions.

While the U.S. has exceeded the 90% benchmark by quite a bit, and we’re still the world’s richest large country, one would be foolish to deny that the U.S. government is potentially in fiscal trouble. We ignore Rogoff and Reinhart’s debt warnings at our peril.

This review follows my usual plan: a roadmap through the book along with my assessment of its quality and readability; next, a more detailed discussion of a few of the issues it raises. I then close with a more personal contribution, in this case, a focus on the Fiscal Theory of the Price Level and its power for explaining inflation and the value of currencies.

How to read this book

Surprisingly, given the book’s topic and Mark Kritzman’s aphorism that nothing about currencies is simple, “Our Dollar, Your Problem” is eminently readable — even fun. The reason is that it’s a memoir, with Rogoff adopting a highly personal tone as he recalls his wanderings through the halls of every major central bank in the world, the International Monetary Fund, and the classrooms of Princeton and Harvard. The personal connection to policies and policymakers makes his arguments come alive in a way that is rare in economics literature.

Rogoff’s occasional waggishness helps enliven the book. He recalls that “This Time Is Different” “improbably reached number 4 on Amazon, just behind the three books of The Girl with the Dragon Tattoo series; then again, those books have sex and violence.”

Given the breadth of Rogoff’s knowledge and experience, it’s not surprising that the book contains detailed analyses of many of today’s major issues in international economics. These include Japan’s rise and relative decline, the end of high growth in China, and the risk of the country falling into a classic middle-income trap, the weirdness of Lebanon and Argentina, and the lure of crypto and other alternatives to traditional currencies. A discerning reader who wants to pick and choose topics can thus learn much from the book without reading the whole thing.

Readers seeking the “royal road to geometry” should instead listen to the excellent podcaster Dwarkesh Patel’s roughly hour-long interview with Rogoff The interview is specifically focused on this book.

The dollar as dominant reserve currency

The central theme of “Our Dollar, Your Problem” is the global dominance of the U.S. dollar and what might dethrone it in the future.

What is a reserve currency?

A reserve currency is one that is held by governments, central banks, and major financial institutions to facilitate investments, settle transactions, and pay international debts, or to stabilize their own domestic currency. In addition, because important commodities such as gold and oil are priced in the reserve currency, other countries must hold this currency to pay for these goods.

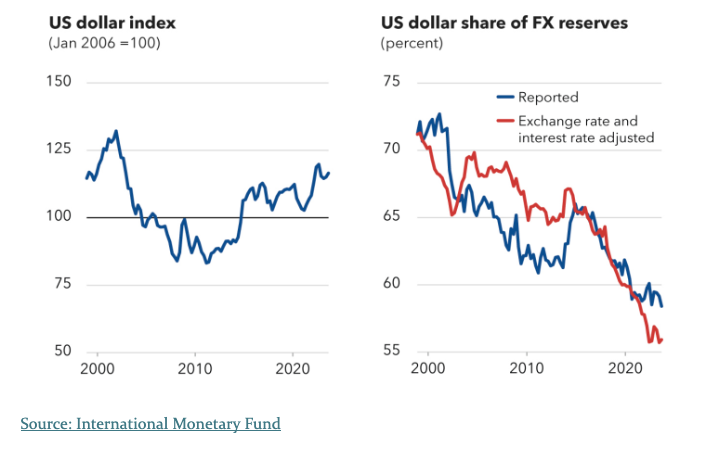

As of late 2024, dollars represented 57% of all foreign exchange reserves. The euro was second, with about 20%, and all other countries had small shares. Exhibit 1 shows, in the left panel, change over time in the foreign exchange value of the dollar and, in the right panel, the evolution of various currencies’ share of foreign exchange reserves. While the dollar’s share has been trending consistently downward, 57% is still a big number, and the post-World War II dominance of the dollar was unsustainable, so the downtrend up to this point is not a problem.

Exhibit 1

Foreign exchange value of U.S. dollar and its share of foreign exchange reserves

Why should we care whether the dollar is a reserve currency?

It’s generally good for a country to be the issuer of a reserve currency. Reserve status creates relatively stable demand for that currency, over and above the ordinary domestic demand for a currency as a store of value, medium of exchange, and unit of account. (Remember that catechism from your first economics class?)

This extra demand means that the U.S. can borrow in dollars almost to its heart’s content. Occasionally, the news media say that a Treasury bond auction has gone poorly, but all that means is interest rates had to rise a bit for the bonds to be sold. No U.S. Treasury bond auction has ever failed in modern times (in the sense of not enough buyers at any price for the volume of bonds offered).1

That’s a strong record, supportive of the dollar being an effective reserve currency — despite the grinding erosion of the dollar’s value, due to inflation, in terms of goods and services. As noted in the introduction, the dollar has lost 97% of its purchasing power since the Fed was established in 1913. That, ironically, means that the dollar has been a success. Almost every other currency has performed worse, with some of them extinguished entirely.2

Based on bond prices, it looks like the future of the dollar is also relatively benign. We can read the long-term inflation expectation (currency depreciation) for the dollar by comparing the Treasury and TIPS yield curves; as of July 25, 2025, expected inflation is 2.44% over 10 years, and 2.54% over 20 years.3 This is a good thing if the market is forecasting inflation correctly.

The relative stability of the dollar is part of the reason it has become the dominant reserve currency in the world. The other reasons are depth and liquidity. Depth simply means there are enough dollars to go around. (The Swiss franc is more stable, but an international financial system based on Swiss francs would face a perpetual shortage of them.) In terms of liquidity, the market for dollars is the busiest market of any kind in the world, with annual trading volume near $2 quadrillion. Need I say more?

So the dollar looks like a good bet to remain the world’s favored reserve currency for quite some time.

Except that Ken Rogoff says it might not be:

If rapidly rising debt is left unchecked, and there seems to be little political appetite to rein in massive deficits, the United States and the entire world is in for a sustained period of...higher average real interest rates and inflation and more frequent bouts of debt and financial crises. (p. 290)

We’ll soon see why it’s “Our Dollar” but “Your (other countries’) Problem.” But first, let’s examine one reason why it’s also our problem: Interest payments on it are very, very large.

Good news and bad news

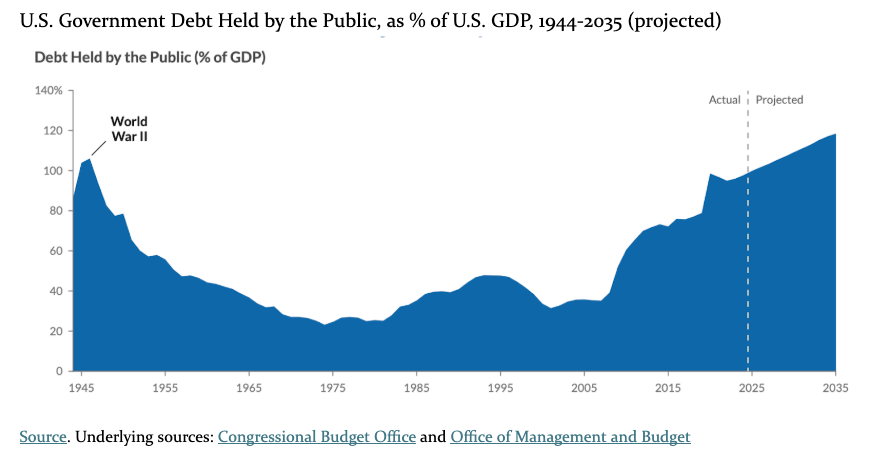

Taken by itself, the fact that the U.S. can easily borrow money is a good thing, especially in case of a war or national emergency. But, like all good things, ease of borrowing and other aspects of having the world’s most in-demand currency has a downside: There has been no market restraint on our government’s profligate ways, with no end in sight to further borrowing and no particular plan to pay the debt back. So the debt grows and grows, from the postwar low of 23% of GDP in 1974 to 98% today. Exhibit 2 shows this evolution.4

Exhibit 2

As of 2025, the interest on this debt is nearly $1 trillion a year, more than we spend on defense — and that number could double in a decade. According to thehill.com, “In 2035, interest payments will double to $1.9 trillion and 17-20 percent of outlays, up from today’s $950 billion interest payments that are 14 percent of outlays.” That forecast presumes the dollar is still the world’s principal reserve currency. If that situation changes, interest rates — and thus interest payments on the debt — could be even higher.

A threat to the dollar

The threat to the dollar’s global reserve currency status, then, is not China or Europe or crypto, but the fiscal policies of our very own United States. You can’t get something for nothing, yet our fiscal policies that depend on ever-growing debt pretend that you can. The more indebted the U.S. becomes, the drawing power of the dollar versus other currencies is less.

We won’t wake up one day and find our dollars persona non grata in the central banks and Treasuries of other countries — major changes in financial arrangements don’t change that fast. It will, instead, be a gradual erosion of one of the most valuable parts of America’s vaunted soft power. Like the proverbial boiling frog, we won’t notice it for a long time, and when we do, we’ll think it all happened at once and wonder, “Who did this to us?”

The answer, of course, will be “we did.”

Will the renminbi be the next ‘dollar’?

No, says Rogoff. Despite the incredible rise of the Chinese economy since the 1970s — to the point where it rivals that of the United States (and exceeds Europe) in sheer output, although not in the standard of living — the renminbi is not ready for prime time for several reasons.

First, China’s economy is slowing. We don’t know by how much, because its data is suspect. Second, the country is awash in debt, not just the central government — which has a debt-to-GDP ratio of 88%, lower than the U.S. — but local authorities, including local government financing vehicles (LGFVs). These contributors push the country’s overall government debt to an astonishing 312% of GDP.5 If that isn’t an impediment to growth and a threat to the international renminbi, I don’t know what is.

Finally, China’s government is enamored of capital controls, which throw sand in the gears of trade, foreign direct investment, and foreign portfolio investment. These considerations greatly weaken the case for the renminbi competing with the dollar in its role as a reserve currency. However, China is taking steps to reduce the controls’ impact and internationalize the renminbi. Bastian von Beschwitz, a senior economist at the Fed, gives this effort a mixed review:6

Prasad (2021) argues that without a full liberalization of the Chinese capital account, the renminbi will not be able to become a global reserve currency. By contrast, Eichengreen et al. (2022) argue that a fully open capital account is not needed for the renminbi to take on a large international role [because invoicing in renminbi requires foreigners to hold them so they can pay Chinese suppliers].

And there is a great deal of foreign investment in China, despite the controls. Bottom line: Despite what you may have heard elsewhere, the risk of the renminbi supplanting the dollar as the dominant reserve currency is pretty remote.

Are the Chinese saving too much?

I was surprised that Rogoff buys into the idea that one of China’s ills is too much saving and too little spending. (Chinese households save about 40% of their income, probably a world record.) Having explained that there is no comprehensive Social Security-like system in China,7 , meaning citizens are responsible for their own retirements, you’d think Rogoff would favor high savings rates. Having many children can ameliorate the problem, but China’s birth rate is very low.

Some years ago, Stephen Sexauer and I published an article showing that Americans of modest means can enjoy a high (70%) income replacement ratio in retirement if they save enough — but, even with Social Security benefits, they had to save up to 27% of income in some periods if investment returns were low. So 40% seems reasonable to me in a country with no government retirement plan at all.

The putative reason that the Chinese “should” spend more is to help the economy. But should you really try to help the economy by hurting yourself? It’s odd that a sensible centrist like Rogoff, who name-checks Milton Friedman as one of the greatest economists of all time, is seduced by this ridiculous Keynesian logic.

The Fiscal Theory of the Price Level and the future of the dollar

The issues discussed in “Our Dollar, Your Problem” are similar to those raised in the “fiscal theory” discourse to which Tom Coleman, Bryan Oliver, and I contributed in a 2021 CFA Institute Research Foundation brief. The Fiscal Theory, developed by Eric Leeper and John Cochrane since the 1990s, arose as an alternative to the classic Quantity Theory of Money espoused by Milton Friedman and also the New Keynesian theory used by almost all central bankers and a large proportion of academic economists.

Friedman, studying monetary policy 60 to 80 years ago,8 had tied the price level (inflation) to the rate of growth of what was then a relevant measure of the money supply, M2 – “currency and various sorts of bank and money market mutual fund deposits that are relatively liquid.”9

Decades later, it became evident that an alternative was needed: Today, all kinds of assets, not just M2, serve as money. These include, or will include, “electronic bank or brokerage transfers..., bond mutual fund[s]..., digital money..., and cryptocurrencies,” Coleman et al. wrote in 2021.10

Although all of these assets have become interchangeable and represent purchasing power, only M2 and government bonds are direct liabilities of the government. As a result, only those two items count in the Fiscal Theory for setting the price level.

How the Fiscal Theory operates

The Fiscal Theory starts by noting that the price level is just the reciprocal of the real value of government liabilities. These liabilities include both currency and government bonds, and can be evaluated like any other asset — by observing the value of whatever backs it.

In the case of government-issued securities, the backing is the present value of expected future tax receipts, minus the cost of generating those receipts (government spending other than interest on the securities themselves). The surplus calculated without including interest on the debt as an expense is called the primary surplus.

Performing this subtraction, a unit of government liability is worth the present value of all expected future primary government budget surpluses, scaled by the size of the liability. Coleman et al. wrote, “The present value relationship closely resembles the dividend discount, or discounted cash flow, equation for stocks or any other security.”

The dollar, comprising these liabilities — whether in the form of currency or bonds — is thus priced by this mechanism.

Wait, what future surpluses? The U.S. government, as Rogoff reminds us, faces deficits out as far as the eye can see. But only primary surpluses matter for this equation, and the U.S. ran primary surpluses of 0.3% of GDP on average from 1947 to 2007, a period over which we faced many economic crises and periods of deficit spending. The years starting in 2008 are another story, with primary deficits the whole time.11

However, if the Fiscal Theory is correct, the fact that the dollar has any value at all (much less dominates the global currency market) means that market participants believe there will be primary surpluses in the future, in large enough amounts to pay the interest on all the securities the government has issued.

The Fiscal Theory and the prospects for the dollar

How does this digression on the latest monetary theory tie back to Rogoff’s book? Since about 2020, the U.S. has embarked on a risky experiment in deficit financing by maintaining large deficits all the time. The national debt is simply the cumulative deficit. Thus, if the balance between government debt plus currency, on one hand, and the backing for these securities (future primary surpluses), on the other hand, is what really explains inflation, then we should prepare for significant inflation — far more than the 2%-3% average rate that has prevailed over most of this century. And a lot of inflation means a major decline in the dollar.

Moreover, U.S. inflation hits non-U.S. holders of dollar-denominated debt twice. The dollar declines relative to the holder’s home currency, and bond prices decline due to rising interest rates, which are the almost inevitable consequence of accelerating inflation.

That’s why Rogoff — addressing governments, banks, and investors in other countries — says “our dollar” is “your problem.”

Conclusion & advice for investors

Ken Rogoff’s professional life is such a rich vein of material for a memoir that it’s impossible to summarize “Our Dollar, Your Problem” in an essay of manageable length — so I didn’t try. I’ve omitted at least a dozen major topics and focused on the one promised in the book’s title — why the U.S. dollar, while appearing strong, is vulnerable and could cause trouble for holders of dollars and dollar-denominated securities in the future.

Rogoff’s concern about U.S. government debt and its possible effect on the value of the dollar is warranted. Investors should be on guard against unexpectedly high levels of inflation. Even a supposedly moderate inflation rate of 3% causes prices to double every 23 years and rise nineteenfold in a century. Following Rogoff’s logic, 3% long-term inflation would be a great outcome. It could get much worse.

I’m not quite that bearish on the dollar, because the U.S. has confronted highly inflationary conditions many times — during World War I, during and after World War II, in the 1970s and early 1980s, and in the early 2020s — and we made the sacrifices necessary to stabilize prices after each episode. In addition, the real economy came out stronger each time. But Rogoff is legitimately concerned that, this time, we don’t have the political will needed to restrain spending and/or increase tax revenues enough to guarantee a happy outcome.

Investors who agree with Rogoff about the risk of prolonged and severe inflation should hold equities (which are an inflation hedge if held long enough), TIPS bonds, and real assets. If they hold conventional bonds, the maturities should be short.

Those who are more confident in the ability of the U.S. to get through this period of yawning government budget deficits should adopt a more conventional allocation, but overweight inflation-resistant assets at least a little.

Ken Rogoff is not given to panic or hyperbole. When he’s concerned about an economic trend, you should be too.

Endnotes

1 I added “in modern times” because I don’t have data before the Great Depression —not because I know of a bond auction failure prior to that.

2 The ideal currency for global reserve purposes is, of course, one that is not expected to lose value at all. While no such currency has ever existed, one operating on the classical gold standard is a good bet for retaining its value on average over the long term (with lots of interim volatility). That’s exactly what the British pound did from 1870 to 1914, and U.K. inflation averaged a minuscule 0.1% per year during that period. (The Bretton Woods gold standard was not a classical gold standard, and there was plenty of inflation under that standard.)

3 I subtracted the 10- and 20-year TIPS yields obtained at https://fred.stlouisfed.org/series/DFII10 and https://fred.stlouisfed.org/series/DFII20 from the 10- and 20-year conventional Treasury bond yields obtained at https://fred.stlouisfed.org/series/DGS10 and https://fred.stlouisfed.org/series/DGS20. The resulting inflation rates are called breakeven rates, meaning the inflation rate at which the TIPS bond and conventional Treasury bond would have the same return. This is the market’s estimate of the inflation rate over the life of the bond.

4 Source: https://www.pgpf.org/article/how-much-is-the-national-debt-what-are-the-different-measures-used/. This is debt held by the public, that is, excluding debt owed by one government agency (the Treasury) to another (e.g., Social Security). Total U.S. Treasury debt is about 120% of GDP. In addition, there is a lot of state and local government debt that the taxpayers must service.

We should not be particularly proud of the low 1974 debt-to-GDP number. The U.S. “paid off” much of its post-World War II debt through inflation; that is, it borrowed in expensive dollars and paid the debt off in much cheaper dollars, causing losses in real terms for bondholders while avoiding default in the sense of not making scheduled payments (“financial repression”).

5 A UC San Diego 21st Century China Center study (Shih and Elkobi 2023) reports that one-third of China’s provinces have debt service expenses that exceed the province’s revenue.

State and local debt in the U.S. are also large and is omitted from most calculations of U.S. government indebtedness.

7 A quick check of websites describing China’s social insurance systems suggests that Rogoff’s statement is too sweeping. See the Council on Foreign Relations report at https://www.cfr.org/blog/what-chinese-pension-system-and-why-are-its-problems-hard-fix. However, this report describes benefits as “minimal” and notes that “about 350 million people [are] uncovered. It thus makes sense for households to save large amounts.

8 Friedman’s seminal work on monetarism is “A Monetary History of the United States,” with Anna Schwartz (1963).

9 https://www.stlouisfed.org/on-the-economy/2023/may/the-rise-and-fall-of-m2

10 While stock mutual funds fluctuate widely in value and don’t meet any traditional definition of money, you can pay your bills (denominated in money) with them.

11 We came pretty close to running a primary surplus in 2015.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Laurence B. Siegel is the Gary P. Brinson Director of Research at the CFA Institute Research Foundation, economist and futurist at Vintage Quants LLC, the author of Fewer, Richer, Greener: Prospects for Humanity in an Age of Abundance, and an independent consultant and speaker. His latest book, On Progress and Prosperity: Essays 2019-2024, contains many articles previously published in Advisor Perspectives. He may be reached at [email protected]. His website is http://www.larrysiegel.org.

The author thanks Thomas S. Coleman, senior lecturer and Executive Director, Center for Economic Policy at University of Chicago Harris School of Public Policy, for his generous assistance.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All