Jack McIntyre’s US global bond fund, aided by a slumping dollar, is posting one of the best performances in its almost two decades of existence. His challenge is convincing investors that it’s more than just a flash in the pan.

His $1.3 billion Brandywine Global Opportunities Bond Fund is up about 12% this year through Aug. 7, a return it’s only beat on a full-year basis twice in the past decade. It’s also trouncing virtually all of its peers, data compiled by Bloomberg show.

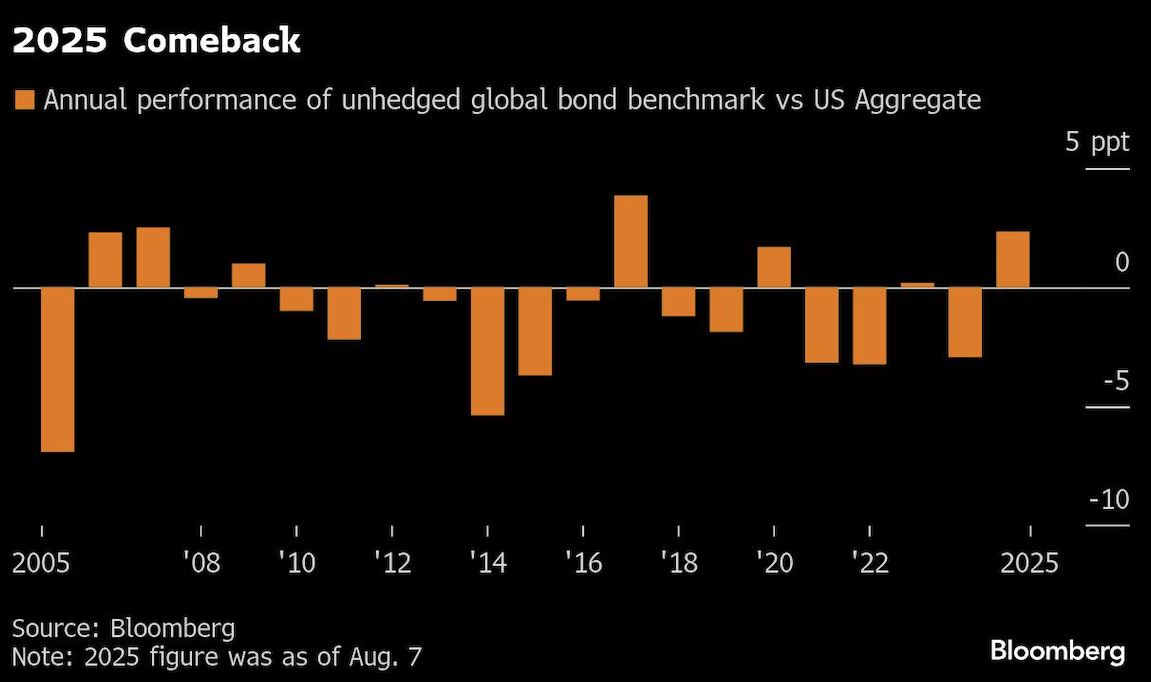

The whole sector, in fact, is outpacing the US fixed-income market by the most since 2017, judging by a dollar-based index of global bonds. And yet hanging over this year’s success is the crucial question of whether the greenback will extend its decline, boosting the value of overseas debt holdings. The currency effect has accounted for roughly 60% of the global bond index’s 7% total return this year.

McIntyre, for one, is positioned for the dollar to slide further, after its steepest first-half loss since 1973. He has less exposure to the greenback than the benchmark he tracks. But he knows he needs more time to lure investors back to an asset class that had been essentially left for dead for most of the past decade.

“It’s more likely that we need to see a couple years of this” to rekindle interest in global bond funds, said McIntyre, whose fund is about a third of its 2015 peak size. “It’s kind of a ‘show-me-the-money’ sort of thing.”

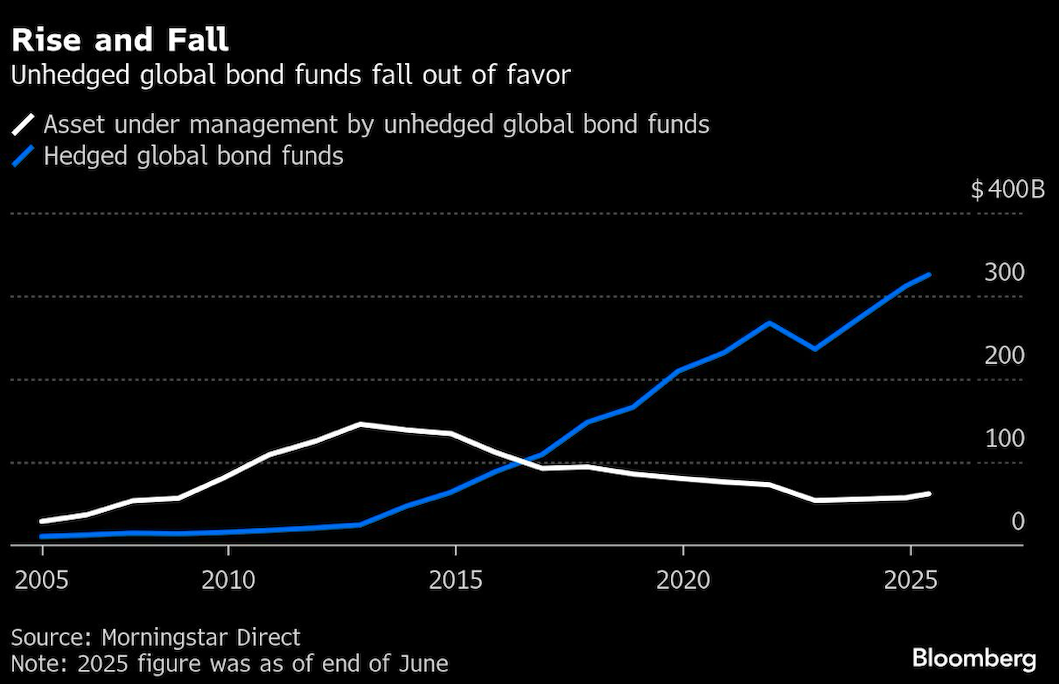

This caution is understandable. The sector saw years of outflows as a strong greenback and attractive US yields penalized bond investors looking to diversify overseas while keeping foreign-exchange exposure. The segment’s assets slumped to $57 billion last year, from a peak of $146 billion in 2012, according to Morningstar Direct.

In a sense, this year’s outperformance leaves US global bond funds, and investors mulling them, at a crossroads.

It could be just the start of a structural shift where investors are finally rewarded for diversifying away from the US as an array of worries fuels a multi-year dollar downturn: from the grim US fiscal outlook, to President Donald Trump’s attempts to strong-arm the Federal Reserve into cutting interest rates, to signs of a cooling US economy. Managers at firms such as DoubleLine Capital and TCW see scope for a much weaker greenback.

“With the dollar likely to continue to weaken, we would anticipate further inflows into unhedged global bond funds, as well as into emerging markets,” said Jamie Patton, co-head of global rates at TCW.

Tracking How Markets Are Reacting to Trump’s Second Term

But just as easily, the strength may prove short-lived if the notion of American exceptionalism in financial markets re-asserts itself and the dollar reverses course. To wit, a Bloomberg dollar gauge has stabilized since setting a low for the year in July.

So far, the money isn’t exactly gushing in. Global bond funds that don’t hedge out currency risk drew in $1.2 billion this year through June, putting them on track for the first back-to-back annual inflows since 2012, according to Morningstar Direct. That still pales in comparison with the record haul of $20 billion in 2010.

Overseas Appeal

US investors have reason to consider parking more cash abroad now, beyond the prospect of a weaker dollar.

At about 1.5%, yields on 10-year Japanese government bonds are near the highest since the global financial crisis amid calls for the Bank of Japan to hike rates to contain inflation. In Germany, 10-year yields at 2.7% are up from an all-time low of minus 0.9% in 2020. Ten-year Treasuries, at around 4.3%, are still higher, but that spread has narrowed.

“For the first time in a while, these jurisdictions look way more interesting,” Andrew Balls, global fixed-income chief investment officer at Pacific Investment Management Co., said of Japan and Europe.

To peel away from the US, though, bond investors have options beyond global funds that use currency exposure to juice returns at the expense of higher volatility.

Strategies that strip out currency risk have been steadily gaining market share, and posting higher cumulative returns over the past decade. Assets of US currency-hedged global bond funds have surged more than ten-fold since 2012, to $325 billion.

Brendan Murphy, head of fixed income for North America at Insight Investment, runs both strategies. His $3.5 billion BNY Mellon Global Fixed Income Fund, which hedges out currency risk, draws far more interest, he said. That’s even though the performance this year of the unhedged counterpart, the $137 million BNY Mellon International Bond Fund, has been superior.

“I’ve been managing the global fixed-income fund for a long time, and I’ve never had so many big institutions asking me about hedged yields and global fixed-income products,” said Murphy, a three-decade Wall Street veteran.

The hedged funds offer another perk: Hedging out dollar fluctuations actually allows US investors to generate higher yields than those available at home. Japanese 30-year bonds, for example, yield about 7% after hedging, compared with roughly 4.8% in the US.

This year, however, that maneuver hasn’t been exactly a winner as steep losses in Japanese debt have offset the yield pickup.

At Ocean Park Asset Management, global bond funds account for about 12% of its $1.3 billion Tactical Core Income Fund, and most of that exposure is in currency-hedged offerings, said James St. Aubin, the CIO.

“International bonds for US investors are kind of a forgotten asset class,” he said. “People are still somewhat skeptical about the longevity of the dollar move.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Ye Xie, Michael Mackenzie