The Federal Reserve is aiming to lessen the costly fluctuations in bank capital demands created by its annual stress tests. But big lenders are pushing for more relief while the central bank is politically weakened and some board members seem keen to please the White House. The Fed must be careful not to give away too much bit by bit by tackling several different regulatory changes in a piecemeal way. A gathering of industry leaders and regulators next month to discuss an integrated review of large banks’ capital requirements, which was announced by the Fed on Thursday, is the place to start.

Financial safety is vulnerable right now. President Donald Trump favors looser regulation in the hopes of promoting growth and squashing what Republicans see as a political focus on climate risks and diversity efforts. At the same time, Trump is trying to undermine Fed independence by hounding Chair Jerome Powell to lower interest rates. Key board members have recently backed early cuts.

Powell himself has also had to eat humble pie over perceived overreach by bank supervisors to influence industry lending decisions through the prism of reputational risk – he has now ordered that be removed from bank assessments. The central bank also stumbled badly in its attempt to update US capital rules and bring them into line with the international Basel standards, which led to a humiliating climbdown by American regulators last year.

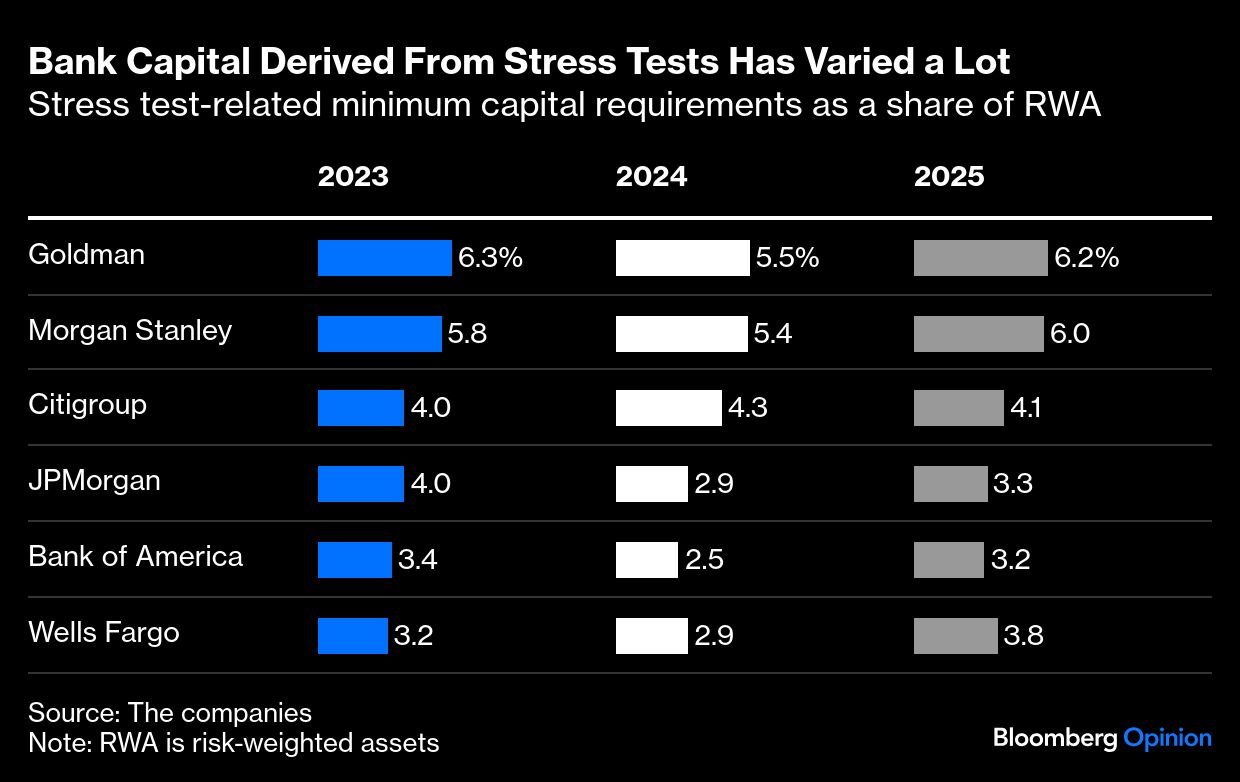

This year’s stress test results are due out today and the Fed might also update markets on plans for the first change to how the outcomes apply to banks. Since 2020, the results of this test are used to calculate between a quarter and a half of big banks’ minimum capital requirements, but because the tests are different each year the amounts involved have varied wildly. JPMorgan Chase & Co., Goldman Sachs Group Inc. and the rest have seen their capital needs fluctuate by billions of dollars.

Rulemakers at the Fed, sympathetic to complaints about the costs and uncertainty, are planning to start using an average of two years’ results to limit the variation. Normally, banks must meet their new requirement three months after it is set: by October after results are released each June. The industry wants a phase-in period to the end of the year. This sensible smoothing could aid banks’ planning without undermining the safety of the system.

However, lobby groups such as the Financial Services Forum, which represents the eight biggest lenders, and the Bank Policy Institute want more. First, they’ve asked that banks be allowed to take the full benefit of any cut in requirements, while using averaging to limit any increase. The argument is that the cost of adding capital is asymmetric and so there’s a justification in making the averaging asymmetric too.

Obviously, this is self-serving. It will tend to favor moves toward less capital over time. It’s also only one side of the argument: There is asymmetry to releasing equity that the Fed should worry about, which poses an additional risk to the stability of the system. The less capital is required, the greater the chance that some bank is unable to cover all its losses and fails. Averaging should apply both ways if it is being used at all.

The cost of extra demands is somewhat academic right now as well because all the biggest banks have significant excess equity over requirements, and this year’s test was less onerous than last year’s, so is widely expected to mean a cut in demands for most banks.

The industry also has more substantial, longer-term changes on its wish list. First, is more transparency in how the stress tests feed into the Fed’s calculations of capital needs. The process has grown more opaque and less predictable in recent years, which hurts the banks. But the argument against too much transparency is that lenders could game the outcome. Worse than that, though, is that banks want to use this to challenge the Fed’s decisions. “It would enable firms to meaningfully seek reconsideration of their [capital] requirement,” the FSF wrote in a letter to policymakers on Monday.

This would be a mess. There are problems with opacity, but regulators must have some power and discretion. Their job is to serve taxpayers and the financial system, not to be tied up in costly appeals and arguments every year.

Another industry complaint is the double counting of some risks between the capital requirements set by the stress test and the base minimum that flows from the wider US capital rules. This is a fair complaint and was a big problem with the Fed’s proposal launched in 2023 to update US rules in line with international standards. That proposal, nicknamed the “Basel III Endgame” in the US, is being rewritten after it was pulled last year.

The answer, however, is not to weaken the capital derived from stress testing – especially before America’s “Endgame” is complete. The best solution is to reexamine these elements together as a single piece of work and ensure an outcome that sets steady and safe capital levels in a way that is efficient and understandable (as far as possible) to all parties.

My view is that the vast majority of banks’ capital requirements should be set under the main capital rules (the Basel Endgame), more like other countries. Regulators should also have discretion to impose extra requirements if individual banks are squeezing much more risk out of their models than peers, or falling down on risk management or governance in ways that endanger their survival. Stress testing should be a warning system for extreme or unusual risks – a sense check on what the main capital rules tell us about the safety of banks. If this were the case, debates around averaging or transparency would be irrelevant.

Michelle Bowman, the Fed board member now in charge of bank rules — and a recent convert to interest rate cuts — has promoted the idea of a holistic review of how capital rules work together, as have industry executives. That would be better than piecemeal bargaining that could cause the death of financial safety by a thousand cuts.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul J. Davies